Getech has now released its final results for the year ending 2015.

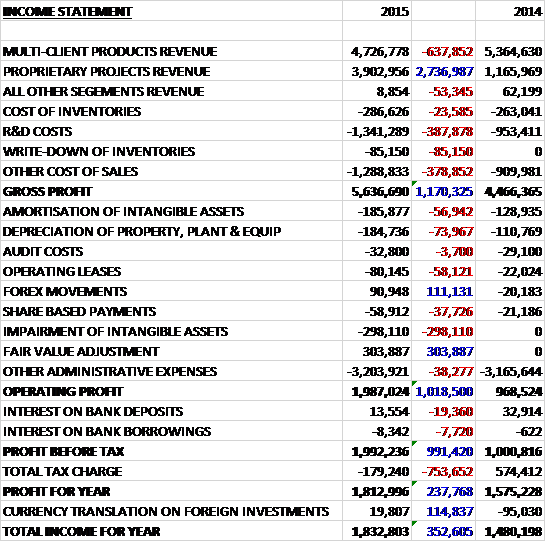

Revenues increased by £2M when compared to last year as a £638K fall in multi-client products sales was more than offset by a £2.7M increase in proprietary projects revenue, and with cost of sales only up £875K, gross profit was some £1.2M ahead. There was an increase in depreciation and amortisation along with a £298K impairment of intangible assets but there was also a £304K fair value adjustment and positive forex movements which meant that, after a £38K increase in other admin expenses, the operating profit was £1M higher year on year. Finance income was a little lower than last time but there was a big swing to a tax charge to give a profit for the year of £1.8M, an increase of £238K year on year.

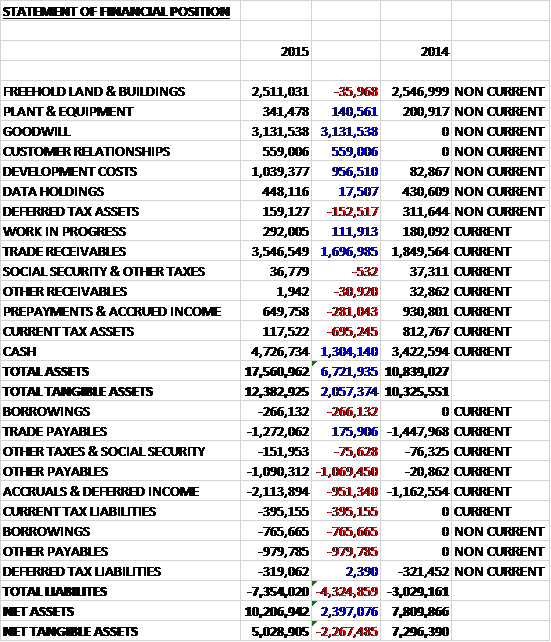

When compared to the end point of last year, total assets increased by £6.7M driven by a £3.1M growth in goodwill, a £1.5M increase in other intangible assets, a £1.7M growth in trade receivables and a £1.3M increase in cash levels, partially offset by a £695K fall in current tax assets. Total liabilities also increased during the year due to a £2M growth in other receivables, presumably relating to deferred consideration on the acquisitions, a 951K increase in accruals & deferred income, and a £1M increase in borrowings. The end result is a net tangible asset level of £5M, a decline of £2.3M year on year.

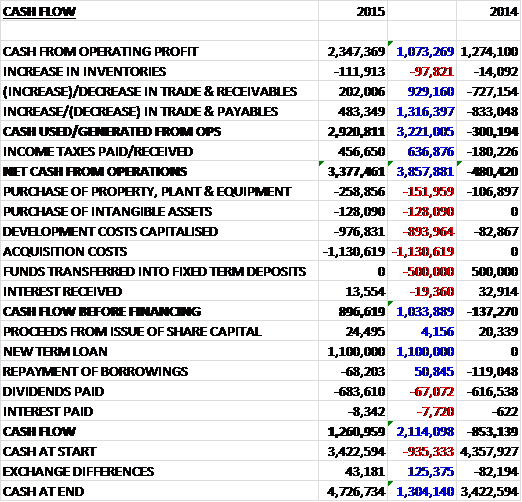

Before movements in working capital, cash profits increased by £1.1M to £2.4M. A good inflow from working capital, especially the increase in payables, plus a £457K tax rebate, meant that the net cash from operations was £3.9M higher at £3.4M. The group then spent £977K on development costs, £259K on fixed tangible assets, £128K on other intangibles and £1.1M on the acquisition to give a free cash flow of £897K. This covered the £684K paid out in dividends but the group took out £1.1M in new loans to give a cash flow for the year of £1.3M and a cash level of £4.7M at the year-end.

For the exploration and production sector, last year proved to be even more challenging than the previous one. The reduction in exploration expenditure the group observed in 2014 has been followed by a very significant drop in the oil price in oil which has led to significant reductions in capital expenditure across the whole sector, and major redundancy rounds in many companies. The reduction in capital expenditure affected exploration spend most dramatically and a wide range of service companies have been severely impacted.

The profit in the multi-client products division was £3.2M, an increase of £402K year on year, the profit in the proprietary projects division was £2.2M, a growth of £1.6M when compared to last year and the profit in other segments was £1K a decline of £60K when compared to 2014.

In September the group announced their largest ever contract, which was $5M of consultancy work for Sonangol, the Angolan national oil company. This involved generating structural and related interpretation for all the Angolan basins. The project has been completed to schedule and the majority of the income was recognised within the past year. In November, a further umbrella contract with a major oil company was announced and in December the first order under this contract was received which amounted to £400K, although nothing much seems to have happened since then. In April it was announced that they had passed through the tender process with another major national oil company, under which they are one of three qualified bidders for a three year programme comprising several basin work packages per year, each of which would be significant – nothing else seems to have happened on this either.

The group have continued the globe investment programme during the year. While they continue to enhance the data content, the globe clients have apparently been particularly pleased by the software that they have developed to improve the user experience. The group continue to build the interpreted data but have also added two significant third party data-sets. One well data-set comprising more than a million North American wells, and a seismic data-set which covers a number of areas of interest across the world. These help to provide the important assurance to Globe clients that their work is controlled by independent data.

Getech has historically been known for gravity and magnetic data, and for geological work at global and regional sales. The acquired ERCL has a particularly strong seismic interpretation team, which has previously been a gap at Getech. ERCL typically operates at a smaller geographical scale and at stages in client workflows which are later than the Getech focus and with some clients they also directly plan the drilling programmes so the group are now able to offer a significantly broader coverage of client workflows. In its first year of trading, ERCL made a pre-tax profit of £1.2M which sounds impressive but is unlikely to be repeated in this environment. The acquisition generated goodwill of £3.1M and was satisfied by £1.75M in cash, £1.2M in shares issued and £1.4M in contingent consideration.

It is expected that the work in the current three year development period of Globe will continue to add to its value as well as increasingly enabling the group to realise value directly through its use at a variety of scales and in a range of product types. In line with the existing strategy, the board aim to increase the level of business with national oil companies. They recently recruited an experienced international business development manager whose role is renewing and establishing relationships with a range of national oil companies and governments, as well as seeking new government data-sets that may become available for use in Globe.

In the short term, there remains considerable uncertainty about the state of the market and its impact on the group’s trading and the board believe the year ahead will be trading substantially below current market expectations. In this context they will seek to mitigate the immediate effects of the lower oil price while at the same time pursuing attractive opportunities as and when they are available, to grow the business in the medium term.

The board believe that they do have a strong foundation for maintaining profitability in the longer term including the globe framework, which entered its second phase in August 2014, which has seen continued support from the larger E&P companies; there has also been continued demand for proprietary projects, where they can leverage the ERCL acquisition to provide a broader range of advice. The acquisition provides capability in seismic interpretation, well planning, field development and asset management, which mitigates to some extent the effect of low oil price on large-scale exploration; the relationships with a number of national oil companies and governments, which are generally less susceptible to oil price fluctuations, provide a degree of robustness and the ongoing relationship with Sonangol demonstrates strength in this area.

There are apparently a number of significant sales proposals awaiting approval. Client budgets are clearly under significant pressure but even where there is little current money, there has still been a willingness to consider proposals for inclusion in 2016 budgets. While there remains significant uncertainty about the short term and the group cannot predict how the market will develop during 2016, they remain convinced that their products and staff are well regarded to satisfy a clear industry need and as such, whilst they expect a slow start to 2016, they remain confident about the long-term prospects for the group.

The group is very reliant on just one client, with 38% of all revenues coming from just one customer which is clearly a major risk for them. At the current share price the shares are trading on a PE ratio of 6.3, increasing to 20.3 on WH Ireland’s next year forecast. The dividend yield currently stands at 6.4%, however, which is forecasted to remain the same in 2016.

Overall then, the last year has actually been a pretty good one for the group. Profits were up, operating cash increased and there was plenty of free cash but net tangible assets did decline. The globe data set seems to be coming on nicely and the ERCL acquisition looks a good fit. There are two major problems here though. The first is that a big portion of their revenues have come from Sonangol and this work has now finished and the second is that the decline in the price of oil has led to many oil companies slashing budgets which leaves Getech in a rather difficult place. The house broker has reduced their forecast so the PE is now at an expensive looking 20.3 for next year. The dividend yield of 6.4% does look tempting but an investment here really depends on when you think the price of oil will increase. The shares are probably worth a punt if you think this will be soon but I am not so sure so have sold out here – an expensive mistake.

Over the past few days it has been announced that director Peter Stephens has purchased 30,000 shares at a value of £10.9K and now owns 1,068,000 shares. This seems nothing more than a token gesture to me.

On the 9th February the group announced that CEO Ray Wolfson was stepping down from his role. Until a replacement is found, he will continue in the role and the Chairman will increase his level of day to day involvement. Ray has been in the role since 2007 and following his resignation he will take on the role of commercial director, which will not be a board position. I suppose at this time of unprecedented turmoil in the market, he felt this was his time to go. Not positive news for the company in my view.