Following the acquisition of Naked Wines, the group has changed its reporting structure. Their operations are now organised into four business units. Majestic Wine Retail is a customer based wine retailer, Majestic Wine Commercial is a B2B wine retailer, Lay & Wheeler is a specialist in the fine wine market and Naked Wines is a customer funded on-line wine retailer. The retail business now includes the retail arms of the UK stores and the Calais stores which were previously reported in a separate business segment. The group has now released its interim results for the year ending 2016.

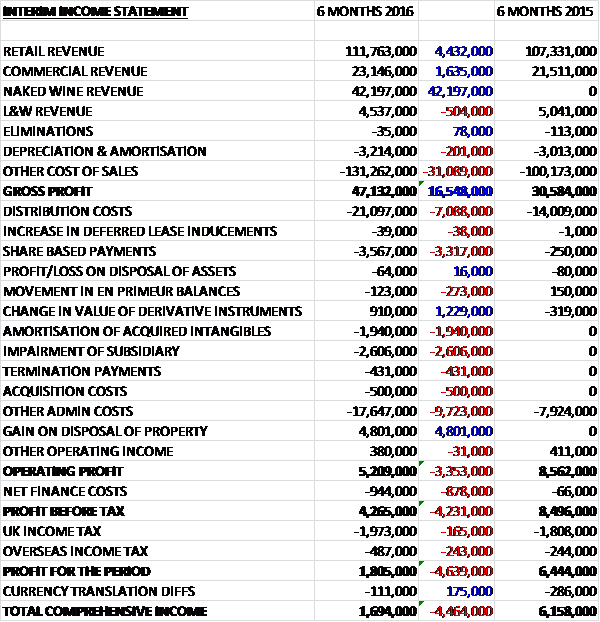

Revenues increased when compared to the first half of last year with a £504K decline in Law & Wheeler revenues being more than offset by a £4.4M growth in retail revenue and a £1.6M increase in commercial revenue. We also see the maiden revenues from the Naked Wines acquisition, with £42.2M being recorded. Cost of sales also increased to give a gross profit some £16.4M above that of last time. There was a £7.1M growth in distribution costs, a £3.3M increase in share based payments relating to the acquisition, a £1.9M amortisation of acquired intangibles, a £2.6M impairment of Law and Wheeler assets, and a £9.7M growth in other admin costs, partially offset by a £1.2M favourable movement in derivative financial instruments and a £4.8M sale of a freehold property which gave an operating profit £3.4M below that of last time. Finance costs then increased, along with a smaller growth in tax so that the profit for the first half of the year came in at £1.8M, a decline of £4.6M year on year.

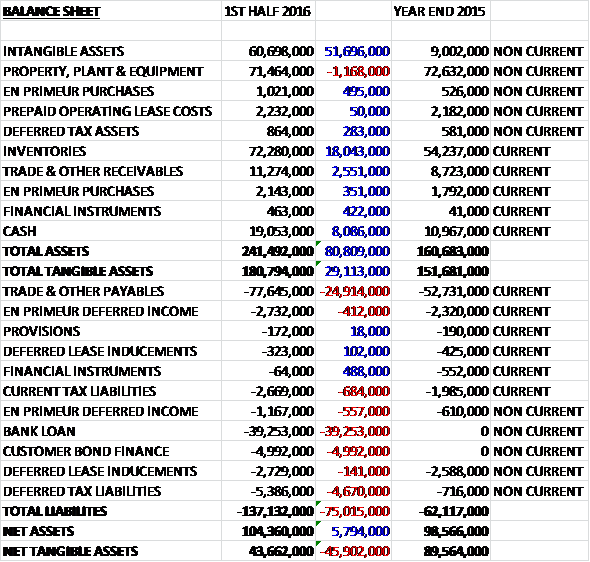

When compared to the end point of last year, total assets increased by £80.8M driven by a £51.7M growth in intangible assets, an £18M increase in inventories, an £8.1M growth in cash and a £2.6M increase in receivables , partially offset by a £1.2M decline in the value of property, plant and equipment due to the asset sale. Total liabilities also increased during the period due to a £39.3M new bank loan, a £24.9M increase in payables, a £5M growth in customer bond finance and a £4.7M increase in deferred tax liabilities. The end result is a net tangible asset level of £43.7M, a decline of £45.9M over the past six months.

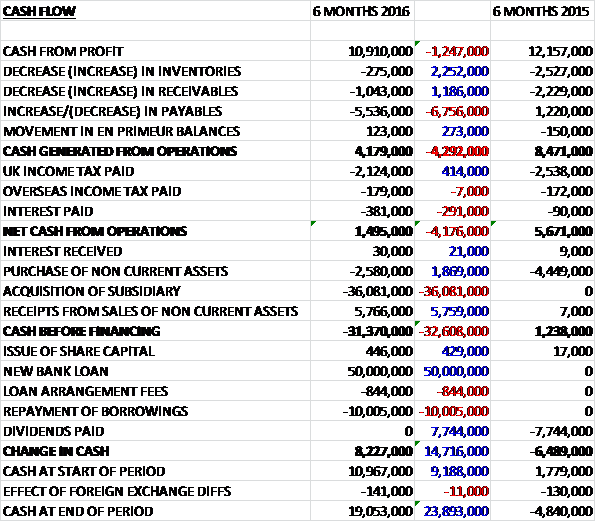

Before movements in working capital, cash profits fell by £1.2M to £10.9M. We then see an outflow of cash from working capital, with a particularly large decrease in payables and after a smaller amount of tax was paid and a higher level of interest, the net cash from operations was £1.5M, a decline of £4.2M year on year. This did not cover the £2.6M spent on capex and the £5.8M receipt from the freehold sale went towards the acquisition so that before financing there was a cash outflow of £31.4M. A net new £40M of bank loans, however, meant that there was a cash inflow of £8.2M during the period and a cash level of £19.1M at the end of the half.

The pre-tax profit in the retail business was £7.5M, an increase of £223K year on year on a 5% growth on sales as costs increased ahead of inflation, a legacy of the store opening programme. The group has seen positive growth even in mature stores which have previously suffered negative like for like sales for some time.

The adjusted pre-tax profit in the commercial business was £2.3M, a growth of £331K year on year which is a lower rate of growth than previous years reflecting a slightly slower build of new accounts during the half. The board are confident that the division can resume historic growth rates and are investing in supply chain, IT and new business development to achieve this and win additional accounts.

The adjusted pre-tax profit in the Naked Wines business was £608K which reflects a better than planned performance from existing customers and the decision to delay spend on customer acquisitions into the second half. This profit was achieved earlier than expected but further expenditure means that profits are expected to fall before they grow again.

The adjusted pre-tax profit in the Lay & Wheeler business was £27K, a decline of £100K year on year and despite growing sales and a stronger en primeur vintage, the business did not achieve targets set at the end of last year which has led to the goodwill associated with the business being impaired with a charge of £2.6M.

The group is targeting over £500M in sales by 2019 but there is a change of emphasis from opening new stores to new customer recruitment to drive higher returns from the current investment spend and the target for UK stores has been reduced from 330 to 230 (the group currently has 211). In addition they intent to review the existing store network for opportunities to unlock value. I don’t like the sound of this, as it seems to me that they are looking to sell and leaseback some stores which is a real bugbear of mine in retail and totally smacks of short-termism. One thing that I do approve of is the removal of the six bottle minimum purchase requirement whilst retaining discounts for those who do buy more, however, as this should improve passing trade.

The group are reducing capex to around £6M per year but this will be lower still in 2016 as they target a reduction in debt as the interest costs are expected to be £2M during the year with exceptional costs of £500K in the second half along with a further £5M of non-cash acquisition expenses. One issue that the board have been battling is the very high turnover of store managers which is currently running at 23% per year and is a particular target for the new KPIs that have been introduced along with customer retention, product availability and wine quality – it is quite nice to see KPIs targeting customer services as opposed to just financial items.

Obviously one of the main events during the period was the acquisition of Naked Wines in April for a consideration of up to £70M payable in a combination of cash and shares. The acquisition generated goodwill of £30.9M and contributed £37K to group profits. In addition to the initial cash payment, a further amount of up to £20M in Majestic shares has been issued to management in the form of contingently returnable shares and share options.

These will vest subject to the achievement of certain performance criteria over a period of four years which actually seems rather excessive to me. In fact, as I mentioned at the time, this is an exciting acquisition but it really is very expensive and over the next two years share based payments and acquired intangible amortisation together is expected to be £11M each year, falling to £7M in 2018.

During the period there has been a bit change in the make-up of the board. John Colley has joined as MD of Majestic Wine, Luke Jecks as MD of Naked Wines and James Crawford joins from Naked Wines as CFO. The profit for the year is likely to be impacted by the increased investment derived from the successful test period and 2016 is likely to be a low point for profit, after which they expect to see sustainable growth as the anticipated returns from the initiatives are realised.

At the current share price the shares trade on a PE ratio of 15.8 but this increases to 17.6 on the full year consensus forecast. No interim dividends were announced so the shares are not currently yielding anything but the intention is to restore dividends progressively by the end of 2018. At the end of the period the group had a net debt position of £25.2M compared to a net cash position of nearly £11M at the end of last year.

Overall then, this has been a period of change for the group. Profits have fallen but this was mostly due to acquisition-related items and the organic profit decline seems very modest. Net tangible assets were down considerably, as would be expected as tangible cash is used to acquire goodwill and intangible assets. Operating cash flow was disappointing and fell year on year with no free cash generated during the period, mainly due to a large payment of payables it must be said, however. The performance of the retail stores seems to be going well, with even older stores posting profit growth and although the commercial profit increase slowed somewhat, the growth in that sector was good.

Naked Wines posted a small profit but this seems to have been as a result of a delay in investment and may reverse in the second half and Lay and Wheeler seems to be struggling, only just breaking even at the moment – there is no indication of what will be done with this business but I would not be surprised to see it closed. The group are targeting debt reduction, very sensibly in my view, and therefore the store opening programme has been slowed. The acquisition of Naked Wines is clearly the transformational event in the period and it seems like a very expensive acquisition to me. With a PE of 17.6 and no dividends on offer, plus the execution risk of a huge acquisition, these shares do not seem to offer much value at these levels in my view.

On the 7th January the group released a Christmas trading update. Total sales growth was 42.6% compared to the same period last year, boosted by the Naked Wines acquisition – on a pro forma basis, sales were up 12.2% on constant currency rates. The retail like for like sales grew 7.3% in the period, supported by the previous investments to reinvigorate sales growth with new and simplified pricing and improved customer service. These investments have obviously resulted in higher costs, however, and a slightly lower percentage gross margin. The commercial business saw sales grow by 10.2%, Naked Wine sales increased by 28.9% but Lay and Wheeler sales declined by 3.5%.

This is clearly a positive performance and progress really does seem to be being made here but as the CEO himself states (refreshingly honestly), this is too early to call it a trend and the shares are looking a bit expensive to me now, especially given the amount of debt.

On the 8th January the group announced that CFO James Crawford and his wife purchased a total of 9,000 shares at a cost of £32K which represents his maiden share purchase. Whilst not a massive amount, I guess this shows some willing from the director.