Avon Rubber has now released its final results for the year ended 2015.

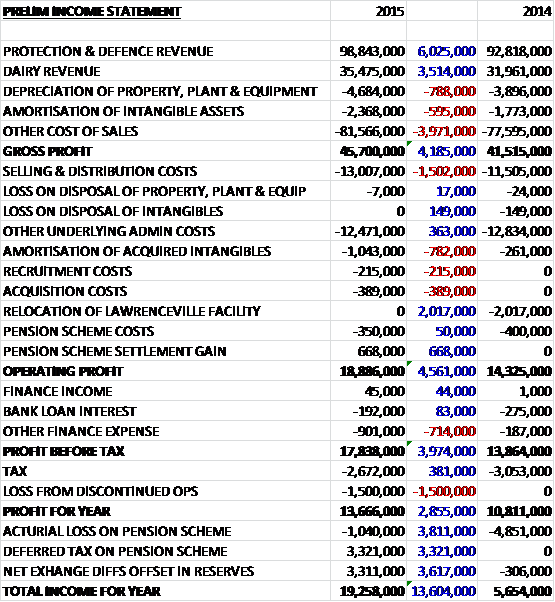

Revenues increased across both business sectors with a £6M growth in protection and defence revenue, along with a £3.5M increase in dairy revenue. Both depreciation and amortisation increased year on year and cost of sales also grew so that gross profit was up £4.2M. Selling and distribution costs increased by £1.5M but underlying admin costs fell. There were also a number “non-underling costs”, not all of which I really agree with. Amortisation of acquired intangibles was up £782K, recruitment costs increased by £215K and acquisition costs were £389K but on the other hand there was no relocation cost, which was £2M last year and there was a £668K pension settlement gain so that operating profits increased by £4.6M. Finance expenses then increased, and there was a £1.5M “loss from discontinued operations” which actually included a rehabilitation provision on a closed business, so that the total profit for the year came in at £13.7M, an increase of £2.9M year on year.

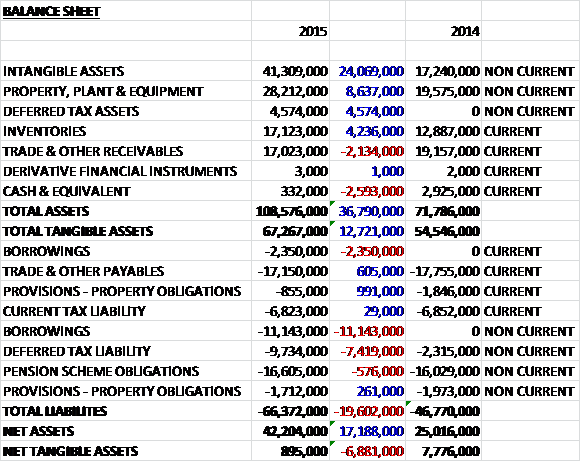

When compared to the end point of last year, total assets increased by £36.8M driven by a £24.1M growth in intangible assets, an £8.6M increase in property, plant and equipment, a £4.6M growth in deferred tax assets and a £4.2M increase in inventories, partially offset by a £2.6M fall in cash and a £2.1M decline in receivables. Total liabilities increased by £19.6M due to a £13.5M growth in borrowings and a £7.4M increase in deferred tax liabilities. The end result is a net tangible asset level of just £895K, a decline of £6.9M year on year.

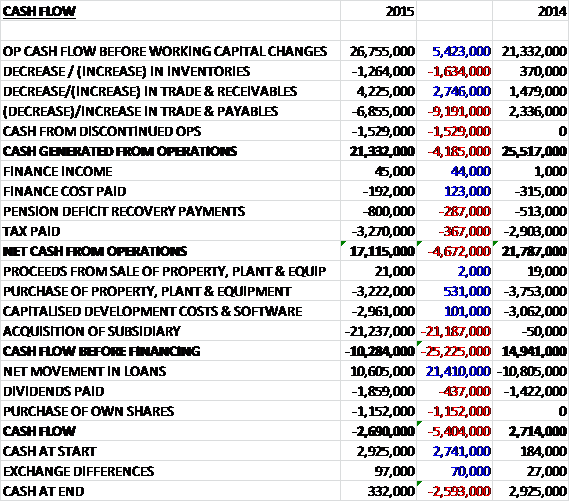

Before movements in working capital, cash profits increased by £5.4M to £26.8M. There was a general outflow of cash from working capital, in particular a big fall in payables which was not helped by a £1.5M cash payment from the discontinued operation so that after a small increase in pension recovery payments and tax paid, the net cash from operations came in at £17.1M, a decline of £4.7M year on year. The group then spent £3.2M on tangible fixed assets and £3M on intangible assets to give a free cash flow of £10.9M before they spent £21.2M on acquisitions. We then see a £1.9M payment on dividends and a £1.2M spent on share purchases but the cash flow was aided by a £10.6M net increase in loans to give a cash outflow of £2.7M for the year and a cash level of just £332K at the year-end.

It is worth noting that the group enjoyed a significant currency tailwind due to the strengthening of the US dollar. The net effect of this is a £1M operating profit gain due to the currency tailwind. The group is also currently enjoying a lower tax rate than normal because it is still using UK tax losses which have now been utilised so this, along with the higher tax rate in Italy where Interpuls is based, means that the tax bill going forward will be higher.

The profit for the protection and defence business was £15.3M an increase of £4M year on year with a £2.3M underlying growth in the year. The DOD, Fire and AEF business have all grown while the non-DOD mask volumes have reduced slightly, as apparently expected given the strong 2014 comparative. Margins have improved due to efficiencies and increased prices under the long-term DOD contract.

Under the DOD long-term M5 mask contract, the group supplied 240,000 mask systems during the year, bringing the total to over 1.4M systems so far under this contract. Having received orders for 172,000 mask systems during the year, the order book stands at only 50,000 systems at the start of 2016 but further DOD M50 orders are expected in the first half of next year as 2016 DOD budgets are released. The filter requirement has less short term visibility, but they expect this consumable item to be a good source of repeat revenue in the long term as more masks enter service. As expected, the DOD qualified a second source to provide filters during the year but in the second half of the year, the group received their first order under this new arrangement for 124,000 filter pairs.

During the year the Joint Service Aircrew Mask programme design, development and testing work progressed well. This will provide respiratory protection to a wide range of operators on the DOD’s fleet of fixed wing aircraft. As previously announced, the DOD has extended its testing phase of this development contract which is now due to conclude at the end of 2016 and should lead to a production contract which could be worth in excess of $70M. Sales to the US law enforcement and non-US military and law enforcement were £27.7M, a decline of £3.3M year on year due to two large orders last year. Despite the decline, there was a good performance from the underlying portfolio and a 10,000 C50 delivery to a customer in the Middle East.

The industrial portfolio launched in 2014 continued to make good progress with particular successes in the oil and gas market and with further product enhancements in the pipeline, there is potential to develop this area of the business. The group saw growth in sales to the North American fire market this year following the release of the new NFPA-approved Deltair SCBA. The product, which is designed to meet the new US regulations and to deliver enhanced operational performance, has been well received by the market and remains one of only four units to receive approval to date. AEF grew strongly in the year, winning hovercraft skirt and fuel and water tank orders as the group have rolled out their non-DOD sales strategy to this area of the business. DOD spares sales have reduced slightly this year, as expected given the volatility of DOD ordering patterns in this area. Long term, as the installed base of masks grows so will the DOD’s requirement to fill its supply chain.

The profit for the dairy business was £5.6M, a decline of £141K during the year but this was only due to the acquisition costs and if the non-underlying costs are discounted, profits increased by £698K. The organic sales growth was achieved despite markets in Europe softening in the second half of the year, reflecting the success of the Cluster Exchange service and growth of the higher margin Milkrite products. Due to the timing of the Interpuls acquisition and the summer holiday season, the acquired business did not contribute to profits this year.

At the start of the year, market conditions improved as global milk prices were at acceptable levels and farmer input costs were favourable meaning there was less pressure on farmer revenues and margins and therefore normal levels of demand for the group’s consumable products. Towards the end of the year, markets softened as these pressures increased due to lower milk prices in some regions. Russian import controls and the removal of quotas have also affected European markets.

The Cluster exchange service was launched in the US and Europe at the end of 2013 and growth rates continue to exceed the initial expectations. By the end of the year it was servicing 430,000 cows on 1,262 farms in the US and Europe. This added-value service enhances the value of each direct liner sale they make and has delivered a more robust business model. Under this programme, farmers outsource their liner change process to Avon, which they deliver through service centres established in their existing facilities. Milkrite sales increased as a proportion of total revenue providing a richer sales mix, rising from 53% to 72% in five years in part due to some OEM outsourcing.

In Europe, Milkrite’s market share has increased as a result of the investment made in the increased sales force, enhanced technical support, and a larger distributor network. The Impulse Air mouthpiece vented liner continues to gain traction with market share increasing from 2.6% to 3.5%. In the US, the air mouthpiece continued to perform well, with market share increasing from 21% to 25%. The group have now commenced work on the next generation of products, the first of which, the Milkrite claw, was launched in Q4 this year.

In China, year on year revenue grew strongly as the industrialisation of the milking process continues apace, creating excellent long-term potential for their consumable products. In South America, where the group opened their sales and distribution facility in the first half of the year, they have started making good progress in establishing a strong dealer network and expect to see growth in this region. In many emerging markets, including India, the number of dairy cows being milked using automated milking processes is growing strongly. This is adding to the market potential for the consumable products the group sells. They plant to harness this potential using the distribution network which InterPuls has already established in these regions.

In June the group completed the acquisition of Hudstar Systems for £3.2M in cash, with deferred contingent consideration of up to £300K and a goodwill generation of £1.1M. In August the group acquired InterPuls for a cash consideration of £18M. This acquisition came with intangible assets of £10.9M and generated goodwill of £1.1M – I have to say that it is quite nice to see properly allocated intangible assets rather than chucking everything in goodwill. After the year-end the group acquired the Argus thermal imaging business from E2V for a consideration of £3.5M. The business is a leading designer and manufacturer of thermal imaging cameras for the first responder and fire markets.

Interpuls provides the farmer with a range of high margin technical solutions including pulsators, milk meters, automatic cluster removers and vacuum pumps, enabling customers throughout the world to configure milking systems. In addition to traditional milking components, the business is expanding into high technology sensors and devices to monitor the life cycle of a cow, analysing milk production, reproduction and health data to provide management information to increase the operational efficiency of the farm. The combination of the largely non-overlapping sales forces of InterPuls with Milkrite should drive higher sales growth than either company could have achieved alone by extending international reach and cross fertilising the product ranges. In combination, the larger business created will increase the group’s profile and the customer awareness in the higher margin areas targeted for expansion.

Hudstar designs and manufactures electronics for breathing apparatus for firefighters and this acquisition both secures the supply chain for some key components of the Deltair products and provides electronics expertise with applications across the rest of the product range.

I must say that after analysing the Easyjet results and how clean they are, it is quite disappointing to see so many “non-underling” items here. We have £215K recruitment costs for board directors which in my view is just a cost of doing business; there is a £389K acquisition cost relating to the purchase of Hudstar and InterPuls which could be considered non-underling; a £350K pension scheme admin cost which occurs every year – this is definitely not “non-underling” and should be included in my view; there was a gain that arose following a trivial commutation exercise which I am happy to discount; and the loss on discontinued operations of £1.5M relating to dilapidation costs of former leased premises of a business which was disposed of in 2006 – I think it is a bit rich calling this a loss from discontinued operations and it is a real cash cost, although not underlying.

Finally, the amortisation of acquired intangibles is removed from the underlying figures. This is not unusual but a real bugbear for me as I think this kind of amortisation is a great way to spread the cost of the acquisitions over a greater period of time and if the company is gaining from the acquisition, it should also be paying the cost in my view. I just wish goodwill was amortised in the same way.

In June the group agreed new bank facilities with Barclays and Comerica Bank. The combined facility comprises a revolving credit facility of $40M and expires at the end of November 2018. This facility is priced on the dollar LIBOR plus a margin of 1.25% which seems pretty good. InterPuls also had a fixed term loan of €2.5M which expired at the end of the 2015 calendar year and is priced at LIBOR plus 0.9%.

At the current share price, the shares are trading on a PE ratio of 24.7 which falls to 20.3 on next year’s consensus forecast so these shares are no longer that cheap. After a 30% increase in the total dividend, the shares are now yielding just 0.7% which increases modestly to 0.9% on next year’s forecast.

Overall then, this has been a good year for the group but probably not quite as good as I was expecting. Profits were up buy net tangible assets were down and the hefty pension deficit and new borrowing means that the balance sheet is actually looking rather weak here in my view. Operating cash flow fell year on year but this was due to a fall in payables and cash profits increased. The protection and defence business performed well with the DOD, Fire and AEF businesses all performing well, although non-DOD masks did decline.

The dairy business performed quite well given the weakness in the market due to the low milk price and the fact that Interpuls is not yet contributing to profits. The forward PE ratio of 20.3 and the dividend yield of 0.9% does not leave much room for error here and I am a little concerned. This year we had a £1M gain from the strengthening dollar and a bit order at the end of the year for DOD masks. When we also add into the mix the fact that all the tax losses have now been used up and the tax bill will be higher next year and there is no longer the backing of the strong net tangible asset level I am very tempted to lock in some profits here.

Avon Rubber has now released its annual report to give a bit more meat to the bones of the final results. We can see that the large increase in finance costs was mainly driven by a £642K increase in the interest paid on the pension scheme and the modest fall in admin costs was as a result of a £1.1M fall in legal and professional fees, partially offset by increases in other underlying admin costs.

The balance sheet gives a lot more detail on the financial position of the company. The £36.8M increase in total assets was driven by a £20.3M growth in intangible assets, a £4.8M increase in the value of freehold property, a £4.6M increase in deferred tax assets, a £4.2M growth in inventories, a £2.5M growth in the value of leasehold property and a £2.3M increase in goodwill, partially offset by a £2.6M fall in cash. The increase in total liabilities was driven by a £13M increase in bank loans and a £7.4M growth in deferred tax liabilities, partially offset by a £2.4M decline in accruals and deferred income.

We can also see just how susceptible the group is to changes in the US dollar/Sterling exchange rate with a 5c movement affecting profits by £609K. The group also indicate an increased potential impact of the loss of a major contract or business to competitors such as price competition in the dairy market and the impact of milk prices and feed costs.

There is also an interesting graph showing the Milkrite market share where it is running at about 50% in the EU and much more in North America but in China, Brazil and Russia the market share is negligible. It is also non-existent in India but most cows are milked by hand in that country so it might be a bit harder to penetrate the market. In conclusion, there it will probably be difficult to gain much more market share in North America but some opportunities exist in the EU. The largest machine milked market available seems to be in Brazil and the largest market as a whole, including hand milking is India.

Overall then, nothing really that material but a few interesting items nonetheless.

On the 14th December the group announced that non-executive director and Chairman of the remuneration committee, Richard Wood will stand down at the AGM following three years in the role.

On the 26th January the group released a Q1 trading update. In Protection and defence, mask systems production has been focused on fulfilling deliveries to the DOD under the ten year sole source contract for the M50 mask. The group continue to see a number of high margin export opportunities but, as usual, timing of these orders remains unpredictable. The board are currently planning for one of these orders to be received sand fulfilled in H1. The integration of the Argus business has progressed well, with the manufacturing operation being moved from Chelmsford to the Melksham facility.

General market conditions for dairy farmers, particularly in Europe, have been weak as milk prices have been low which has reduced demand for the group’s consumable products as farmers extend the life through over using product. The take up by farms of the Cluster Exchange service remains at encouraging levels in both North America and Europe. The board are pleased with the integration of InterPuls. Net debt at the end of the period stood at £10M compared to £13.2M at the year-end.

This is a bit of a messy update in my opinion – there is nothing much of note in the defence business and sales of consumable products have been hit in the dairy business but how does this affect profits? Who knows because there is no information regarding the impact of these factors on the business. The progress on net debt seems fairly decent but having been stopped out a few weeks ago, I am not yet rushing back in on the back of this update.

It is also interesting to note that at the AGM, some 23% of shareholders voted against the resolution to approve the remuneration policy. This is perhaps something to do with the CEO earning over £1.4M last year with an annual bonus of more than 100% of the base salary and some £604K worth of shares from the long-term plan. This seems very excessive for a company of this size so the shareholder response is not that surprising.

On the 1st February the group announced that new CEO Robert Rennie purchased 10,000 shares at a value of £77.8K which represents his maiden share purchase.

On the 26th February the group announced that Chloe Ponsonby will be appointed as a Non-executive director in March. She is a partner at the Lazarus Partnership, an independent research and advisory firm and has spent the last ten years advising companies as a corporate broker and independent advisor.

On the 3rd March the group announced the receipt of an order for 166,623 M50 mask systems worth $42M under the ten year sole source contract with the US DOD. This secures the expected volume of mask system sales for 2016.