International Greetings has now released its interim results for the year ending 2016.

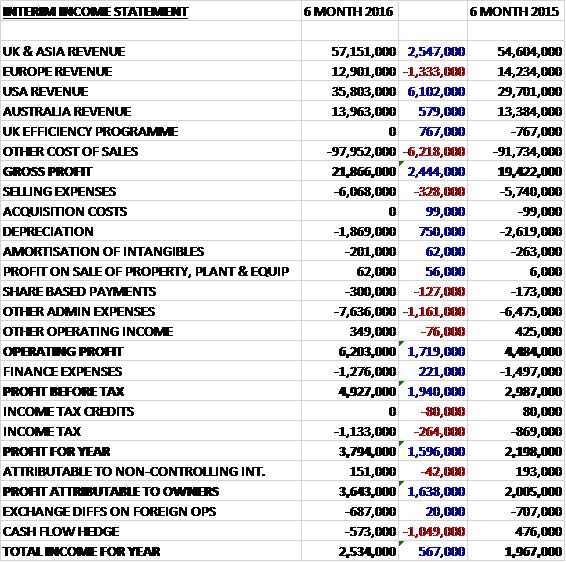

Revenues increased when compared to the first half of last year as adverse movements in exchange rates were mitigated by favourable timing of sales with a £1.3M decline in European revenue being more than offset by a £6.1M growth in US revenues, a £2.5M increase in UK revenues and a £579K growth in Australian revenues. Cost of sales also increased but there was no charge for the UK efficiency programme which accounted for £767K last time which meant that gross profit increased by £2.4M. Selling expenses increased by £328K and underlying admin costs grew by £420K as a £750K decline in depreciation was offset by increases in other admin costs, which gave an operating profit £1.7M above that of last time. A lower finance expense was offset by an increase in tax so that the profit for the period came in at £3.6M, an increase of £1.6M year on year.

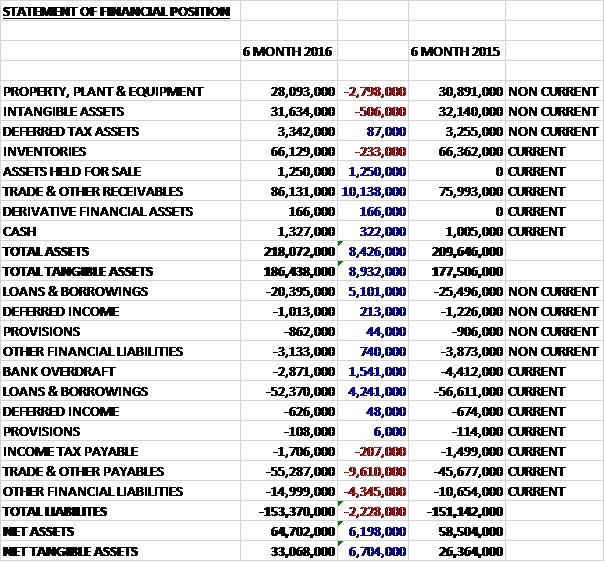

When compared to the same point of last year (due to the highly seasonal nature of sales, this seems to be the most sensible comparison) total assets increased by £8.4M driven by a £10.1M growth in receivables and a £1.3M increase in assets held for sale, which was moved from property, plant and equipment and relates to the printing site in Aberbargoed following the relocation of printing to the Penallta site, driving a £2.8M fall. Total liabilities also increased during the year as a £9.6M growth in payables and a £3.6M increase in other financial liabilities was partially offset by a £9.3M fall in borrowings and a £1.5M decline in the bank overdraft. The end result is a net tangible asset level of £33.1M, a growth of £6.7M year on year.

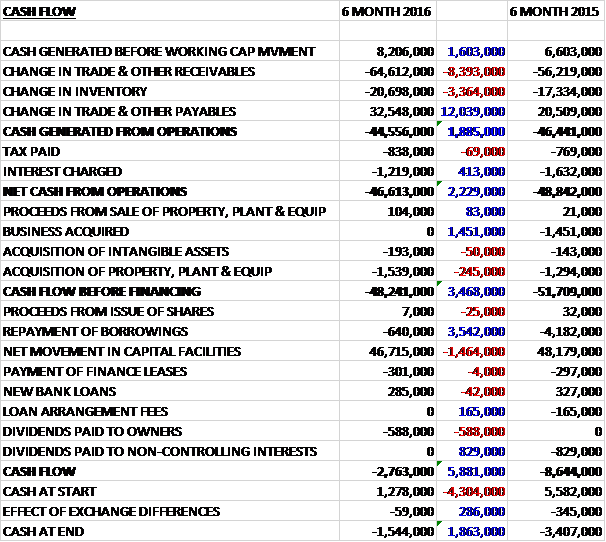

Before movements in working capital, cash profits increased by £1.6M to £8.2M. We can see just how much cash is absorbed by working capital at this time of year (it peaks in October), however, with large increases in receivables and inventory only partially offset by a growth in payables due to the earlier sales profile reflecting the variable phasing of deliveries to customers year to year, which meant that after the interest charge fell by £413K to £1.2M; the net cash outflow from operations came in at £46.6M, an improvement of £2.2M year on year. The group spent £193K on intangibles and £1.5M on fixed assets reflecting the initial costs of the investment in an improved converting capability in the US as well as further investment in efficiency in Europe and China, to give a cash outflow of £48.2M before financing but if there was a neutral working capital position, there would be plenty of free cash available. The group spent a bit on dividends and after the cash income from capital facilities, the cash outflow for the period was £2.8M to give a cash level of -£1.5M at the period-end.

Overall, performance in the first half of the year was in line with expectations. The profit in Europe was £835K, a fall of £87K when compared to the first half of last year as manufacturing efficiencies and customer channel mix was not quite enough to offset the effect of a weaker Euro which impacted margin on products that are predominantly purchased in US dollars. The profit in the UK and Asia was £3.6M, an increase of £115K year on year where strong sales growth was underpinned by a strong portfolio of licensed brands including Star Wars, Minions and Coca-cola, although gross margin fell due to changes in product mix. The business is also on track to deliver expected annual efficiencies resulting from investment in the manufacturing facilities in Wales.

The performance of the China-based Christmas cracker manufacturing operation has exceeded targeted efficiencies and they have delivered in excess of 70M crackers for the 2015 season. They have continued to invest in semi-automation at the facility to mitigate the challenges associated with the increasing cost and reduction of availability of labour in the country. The profit in the USA was £1.8M, a growth of £1.2M when compared to the first half of 2015 on improved sales in a market that remains strong. Gideon Schlessinger started his role as CEO of the US business in April. The profit in Australia was £509K, a decline of £85K year on year despite sales growing during the period. The joint venture is apparently still on track to meet profit expectations though.

It sounds as though the results during the first half of the year have been aided by favourable timing of sales with earlier phasing of deliveries to customers. The benefits of tax losses are starting to unwind and cash tax is increasingly payable in most of the group’s geographic regions as historical tax losses are fully utilised. There are still unrecognised losses with a tax value of $2.3M in the US and £300K in the UK, however.

So far in the second half, trading activities are in line with expectations with a strong order book in place for the balance of the year and already beginning to build for next year. The group are on course to achieve targeted growth in EPS and remain firmly focused on reducing debt through converting profit into cash, which is good to hear.

At the end of the half net debt stood at £78M, still substantial but £6.6M below that of the same point of last year. At the current share price, the shares are yielding 1% in dividends. I have not yet been able to see a forecast for the full year but going by historical forecasts, the yield was predicted to be 1.1% for 2016.

Overall then this has been a fairly decent half year for the group. Profits increased year on year but on closer inspection this was due to a fall in depreciation and the lack of efficiency programme and acquisition costs that occurred last time. Net assets did improve, though, and operating cash flow also improved despite remaining heavily negative due to the timing of Christmas orders and the effect this has on working capital movements. The UK performed fairly well due to increased sales of lower margin licensed brands but it was the US that was the stand-out performer. Things were not quite so good in Australia and Europe, both probably effected by weakness in the respective currencies.

I am a little concerned that the results this year were pumped up a bit by a favourable phasing of orders and without this effect, I can’t see them having been up year on year. Still, the board see the performance this year as being in line with expectations and the real story here is the continued recovery and pay down of the debt which will only really become apparent for the full year. The dividend of 1% is nothing much to get excited about but I will probably hold on here for the long term story.

On the 15th December the group announced the appointment of Mark Tenori as a non-executive director. He is currently CFO of Adelie Foods which manufactures and supplies sandwiches to retailers and is owned by private equity group HIG. I’m not sure what specific experience this brings to the group to be honest, but the board obviously saw something in him.

On the 18th January the group released a trading update covering Q3 which includes Christmas trading. Business continued to be strong during the Christmas period with results in line with expectations and all regions trading profitably. In Wales and Holland the new giftwrap manufacturing facilities have enabled the group to produce high volumes very efficiently with return on investment in line with plans. The operation in China performed well through the year, in the US record sales levels were reached with growth across all channels together with an expansion of export activities to Canada, Mexico and Brazil. There has also been significant growth of their market share in Australia where the “Celebrations” product offering has broadened to include a comprehensive party ware offering, which is an interesting development. Sales performance during the period of the licenced product portfolio featuring big hitters such as Star Wars, Minions and Frozen included sales to new territories and customers.

Overall then, a pretty decent update and things seem to be going as expected.

On the 18th April the group released a trading update covering 2016. The financial performance was ahead of expectations, resulting in a further year of double digit EPS growth. Operational cashflow and debt reduction continued to reduce leverage significantly ahead of expectations and property held available for sale at Aberbargoed in Wales was sold with proceeds of £1.45M being received. The company intends to pay a final dividend of 1.75p which means that the yield is currently standing at 1.4%.

All regions have delivered year on year growth and an overall market outcome ahead of market expectations. In the UK and China, record sales combined with a good manufacturing performance delivered profitability ahead of forecasts. In Continental Europe, sales growth and effective management of mix have mitigated forex transaction headwinds. Trading in the second half of the year in Australia has resulted in in significantly enhanced overall profitability.

In the US, the commercial, operational and financial performance of business has been encouraging. This has included the implementation of phase two of the programme of fast payback investment in manufacturing which will accelerate their capability to profitably grow their share of this market.

This is great stuff, and I am very satisfied with my holding here. If there is any weakness before the results I might even double up on my investment.

On the 24th June the group announced that it had changed its name to IG Design Group, thankfully the ticker remains the same.