Telford Homes has now released its interim results for the year ending 2016.

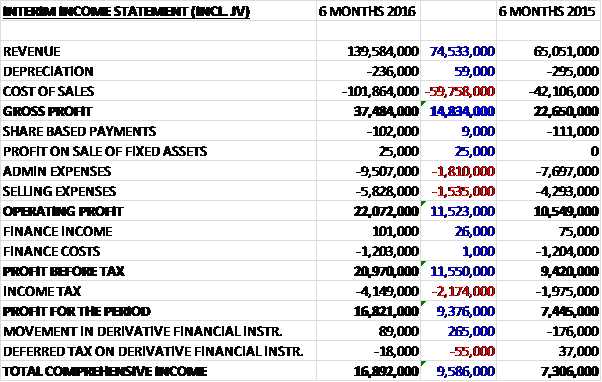

Management believe that the joint ventures are an integral part of the business so they have included them in the income statement – I agree with them! (This year they generated profits of £444K and in the first half of last year, £10.8M) Revenues increased by £74.5M when compared to the first half of last year and after a £59.8M growth in cost of sales, the gross profit increased by £14.8M. We then see a £1.8M growth in admin expenses due to higher employee costs along with legal and professional fees associated with the acquisition and a £1.5M growth in selling expenses as a result of the successful sales launches in the first half of the year along with an increase in the number of completions to give an operating profit some £11.5M above that of last time. Finance costs were broadly flat and mainly relate to non-utilisation fees on the bank facility but tax costs more than doubled which meant that the profit for the half year came in at £16.8M, a growth of £9.4M year on year.

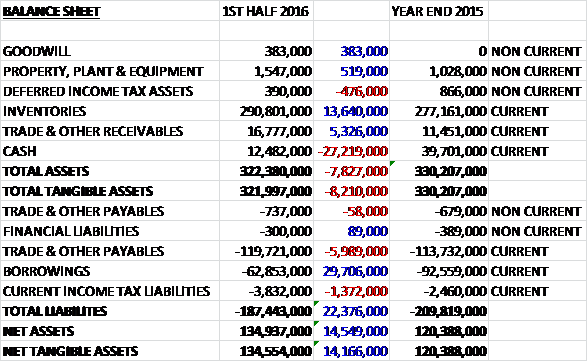

When compared to the end point of last year, total assets declined by £7.8M driven by a £27.2M fall in cash partially offset by a £13.6M growth in inventories and a £5.3M increase in receivables. Total liabilities also decreased over the period as a £29.7M fall in borrowings was partially offset by a £6M increase in payables and a £1.4M growth in current tax liabilities. The end result was a net tangible asset level of £134.6M, a growth of £14.2M over the past six months.

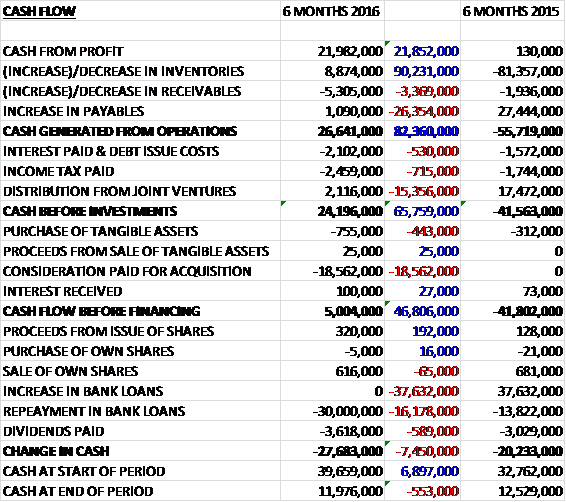

Before movements in working capital, cash profits increased by £21.9M to £22M. A fall in inventories meant that there was a cash inflow from working capital and after an increase in interest and tax, a much lower contribution from the joint ventures meant that net cash from operations came in at £24.2M, a positive movement of £65.8M year on year. The group then spent £18.6M on acquisitions and £755K on intangible assets to give a free cash flow of £5M, of which £3.6M was spent on dividends and some £30M was spent in paying back bank loans so that there was a cash outflow of £27.7M over the past six months to give a cash level of £12M at the period-end.

As expected, the double digit sales price inflation seen in London in 2013 and early 2014 has stopped and affordability constraints have ensured a more sustainable market over the past year with increased of about 4% to 5% per annum. Build cost inflation is still evident across the industry but this has also moderated to a similar rate of increase and is in line with board expectations. At the group’s price point they are seeing consistently strong demand and there is no evidence of that slowing as London still suffers from an acute shortage of homes compared to current need.

Strong demand for the group’s homes has led to continuing sales success across a number of different developments. The launches of both Manhattan Plaza and Bermondsey Works earlier this year exceeded the board’s expectations. In September the group opened a new central sales and marketing suite in Stratford which has already proved its worth through the launch of the remaining 32 homes at Stratosphere with 18 reservations secured on the first day and only eight now remaining for sale. Including the revenue reported for the first half of the current year, the group has secured total forward sales of more than £700M to be recognised from 2016 onwards.

Investor demand continues due to a thriving rental market and, despite recent tax changes, this is expected to remain a significant component of the group’s sales over the next few years. Owner-occupier demand is also prevalent and the board expects to derive more benefit from the new Stratford sales and marketing suite on future schemes across a wide spectrum of buyers.

The group has already indicated that it has been monitoring the emergence of institutional investment in the Private Rented Sector and the board expects this to be a feature of their sales in the future. Strong values can still be achieved based on rental demand and yields in certain locations and, as recipients are paid during construction, cash flow is improved with no need for external debt finance. They have recently been marketing one of its developments for PRS and hope to conclude a sale in the near future. If this is successful further developments could be sold to the same market.

After an initial delay, full planning permission is now in place for 156 homes at Caledonian Road and work is underway on site. In addition permission has been granted in the last few weeks for 471 homes at Chobham Farm, Stratford in partnership with Notting Hill Housing Group, for 192 homes at Redclyffe Road and for an increased scheme of 155 homes at Limeharbour.

The group had drawn debt of £65M at the end of the period from its £180M corporate loan facility leaving headroom of £115M to fund future site acquisitions and construction costs. The facility extends to March 2019 and they expect to utilise it in full over the next few years.

At the end of June the group acquired the regeneration business of United House Developments which consists of a group of companies that have various interests in four significant development opportunities in North and East London. An amount of £23M was paid in September which includes an amount held in escrow relating to one of the four developments, Gallions Quarter, where completion is conditional on UHGHL securing a legal interest in the site. The consideration at the end of June was £18.6M which generated goodwill of £304K.

After the period-end the group issued 13,888,889 shares at 360p per share as a result of a share placing which raised £50M. The net proceeds of the placing are expected to be committed within one year and fully utilised within two years with an initial focus on driving sustained profit growth and targeting annual pre-tax profit exceeding £45M from 2019 onwards. Beyond this the board expects to maintain controlled growth towards pre-tax profits of £60M whilst also utilising the recycled equity to manage future debt requirements and therefore reduce longer term gearing.

The group has already begun allocating the placing proceeds to new opportunities and towards the end of November they announced that they had exchanged contracts for the purchase of a significant development site on Carmen Street in Poplar for over £20M. The site has full detailed planning consent for a 22 storey development consisting of 206 new homes and a nursery, and represents an improvement on the board’s expectations of committing the new equity on sites requiring a planning consent. Work is expected to commence in 2016 with completions expected in 2019 and 2020.

The board is very confident in the prospects for the group over the next few years with output expected to more than double over the next five years. The results for the 2016 as a whole are expected to be weighted to the first half of the year with a greater number of open market completions occurring in this period. The number of open market completions in the first half of the year was 282, up from 140 last year. The balance between the two half years reflects the timing of completion of the group’s developments with the remaining homes at Cityscape, Parkside Quarter, and the Boatyard handing over in the first half of the year together with over one third of the 198 open market homes at Stratford Plaza. Overall the board is very confident of meeting market expectations for the year as a whole.

At the current share price the shares are yielding 3.2% which increases to 3.5% on the full year consensus forecast.

Overall then, this has been a good half year period for the group. Profits are up, net assets increased and operating cash flow grew to give plenty of free cash. The business is very lumpy though, and this mainly reflects timing of sales with the second half of the year expected to be slower. Property inflation in London has now slowed but it seems that build cost inflation has also slowed to increase at roughly the same rate. Demand for the group’s homes is still strong and the board are expecting investor demand to remain strong despite the new legislation taxing buy to lets. The institutional investment in PRS seems as though it should improve cash flow but I assume this must be at the detriment of margins so this could be a bit of a short-term gain for long term pain situation and as such I am not sure I like it.

There seems to have been some decent planning permissions coming through over the period and at my reckoning with £65M debt at the period-end and a net £30M cash inflow from the placing and the Carmen St development, there should be plenty of headroom on that £115M facility. Despite the first half weighting, the board are very confident of meeting market expectations for the year as a whole which sounds like they might slightly beat expectations and with a forward yield of 3.5% this company is looking interesting. There is still a bit of a profit gap in 2017, however, and the debt levels are not inconsequential. This is all fine if the economy continues to do well but what happens if a recession hits in 2018 when most of the group’s developments are coming on stream and they have leveraged to the hilt (as they intend to do)? It’s not without its risk, this one.

On the 22nd December the group announced that the wife of non-executive director Frank Nelson purchased 12,954 shares at a cost of £50K. This is his first share purchase so I am not reading much into it.

On the 5th February the group announced that Jane Earl had been appointed as a non-executive director and will replace David Holland who is retiring at the AGM. Jane holds a degree in law and is on the board of Sentinel Housing Association. Previously she worked on the board of the Planning Inspectorate and was formally CEO of Wokingham Unitary Council and took positions at a number of local government organisations across the South of England. This looks to be a useful appointment to me.

On the 15th February the group announced that it had exchanged contracts for the sale of The Pavilions, Caledonian Road, to a subsidiary of L&Q, one of the country’s leading housing associations. The transaction is for the sale of all 156 homes within the development, 96 of which will form part of L&Q’s substantial private rented sector portfolio. Under the terms of the planning permission, the remaining 60 homes have been sold to L&Q for affordable housing. The contracted price for the entire development is £66.75M with regular payments to be made by L&Q throughout the construction period. As a result the development will not require any equity or debt to be invested by Telford. Construction is already underway and is expected to be complete by mid-2018.

This contract marks the group’s first significant development sale in the PRS sector. There is increasing institutional demand for developments to be “built for rent” and the group have been encouraged by the overall response to the marketing of the Pavilions. They are already exploring a second development for sale in the sector and the board expects that similar PRS sales will form an important part of their sales mix going forward.

On the 17th February the group announced that Land Director James Furlong purchased 20,000 shares at a value of £66.5K which takes his shareholding up to a hefty 1,334,342 shares. A day earlier they announced that non-executive director David Holland purchased 10,000 shares at a value of £32.5K and David Campbell, group sales and marketing director, purchased 2,000 shares at a value of £6.5K. These transactions meant that Mr. Holland owns 571,444 shares in the company and Mr. Campbell owns 41,796 shares.

On the 22nd March, it was announced that Land Director James Furlong purchased 20,000 shares at a value of £69K which gives him a total holding of 1,254,342 shares. It was also announced that non-executive director Frank Nelson purchased 14,385 shares at a value of £50K to give him a total of 27,339 shares. It seems to me that the director buying here is starting to get interesting.

On the 13th April the group released a trading update covering 2016. The board expects pre-tax profit to be slightly ahead of current market expectations. They are already over 90% forward sold at the start of the year but have improved on original forecasts due to initial profit recognition on the PRS sale.

The market has remained strong for the typical Telford product. The launch of the Liberty Building, E14, has demonstrated that investor demand continues to be healthy. In the last four weeks the group have secured over £40M of future revenue at this development with 68 of the 105 open market homes already sold. A third of these sales were to UK investors and the remainder to international investors in China and Hong Kong. The development is expected to be completed in 2019.

The average price achieved was around £900 per square which is at the upper end of the normal price range and ahead of initial expectations with no abnormal incentives having been required.

The group has seen the effect of recent stamp duty changings having a limited impact on sales of more affordable properties. Apart from the Liberty Building, other sales have also been progressing well with the new central sales centre in Stratford achieving 40 sales with a combined value of £25M since opening in September. The total forward sales to be recognised from the start of this month stands at £579M against £503M at the start of last year. This will increase as further sales are achieved during the year and the group has over 50% of the cumulative revenue expected in the three years to 2019 already secured.

The group are positive on the future benefits which institutional PRS brings. They have secured the sale of the Pavilions in Caledonian Road to L&Q, one of the country’s leading housing associations, for nearly £67M in February and have now agreed terms on a second PRS transaction with another investor. These sales improve cash flow but also bring forward profit recognition on a moderately reduced margin so they basically bring forward profits that would have been made at a later date but for less money. The board expect these sales to become an increasing feature of their sales mix over the next few years.

Assisted by the anticipated PRS sales, the group no longer expects there to be a dip in profit levels in 2017, an issue originally created by planning delays. Instead they expect profit levels to continue to grow so that pre-tax profit is now expected to be over £50M in 2019, ahead of prior expectations.

Following the United House acquisition last year, the development pipeline remains over £1.5BN of future revenue. The group raised £50M of new equity in its placing last year and in addition has headroom in its banking facility of £140M. Immediately after the placing they announced the purchase of a site in Camden Street, Poplar for £20M. Many opportunities continue to be appraised and the board is confident of committing the remainder of the placing funds in the coming year.

The group is focused on relatively affordable locations in London where demand remains strong from owners and investors. The balance of supply and demand in London is significantly in the group’s favour and whilst external political factors such as the Brexit vote is likely to cause a period of uncertainty, it should not change this dynamic. The board are confident that they will be able to deliver a significant increase in profit levels over the next few years.

Overall then, this is a positive update with the group now expecting profits to be slightly higher before. It is a shame that this is offset by a slight reduction in margin and the need for them to have raised equity in the market. There are some short-term headwinds in the industry as a whole and until the uncertainty over Brexit is over, I am reluctant to jump in again here.