Sanderson has now released their final results for the year ended 2015.

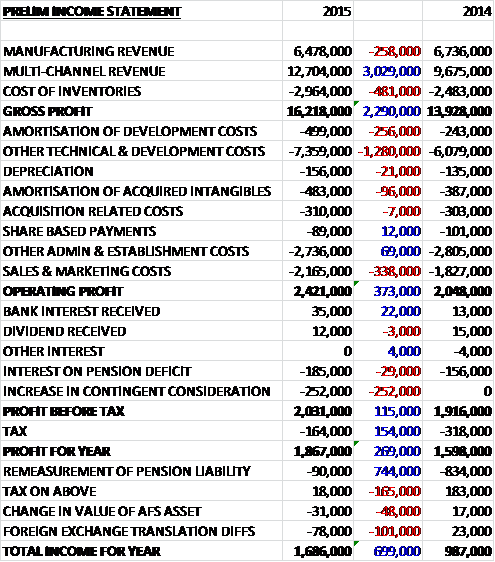

Revenues increased when compared to last year as a £258K fall in manufacturing revenue was more than offset by a £3M growth in multi-channel revenue. Cost of sales increased somewhat to give a gross profit some £2.3M above that of last year. The amortisation of development costs increased by £256K and other technical costs grew by £1.3M and after admin expenses were broadly the same and selling and marketing costs increased by £338K, the operating profit was up by £373K. We then see an increase in contingent consideration offset by a fall in the tax charge relating to the utilisation of tax losses and over provision in previous years so that the profit for the year came in at £1.9M, a growth of £269K year on year.

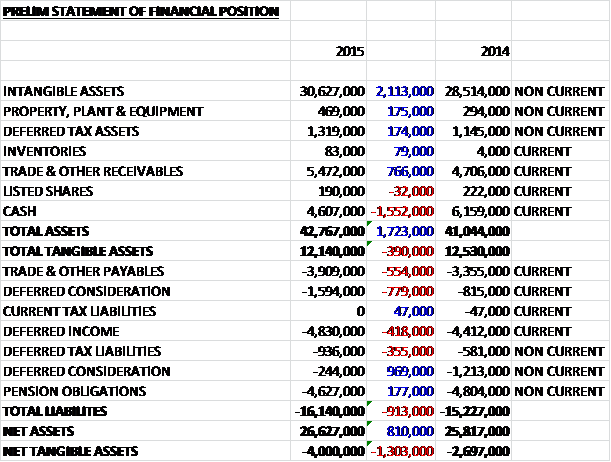

When compared to the end point of last year, total assets increased by £1.7M driven by a £2.1M growth in intangible assets and a £766K increase in receivables, partially offset by a £1.6M fall in cash. Total liabilities also increased during the year due to a £554K growth in payables, a £418K increase in deferred income and a £355K growth in deferred tax liabilities. Overall the net tangible asset level was a negative £4M, a deterioration of £1.3M year on year.

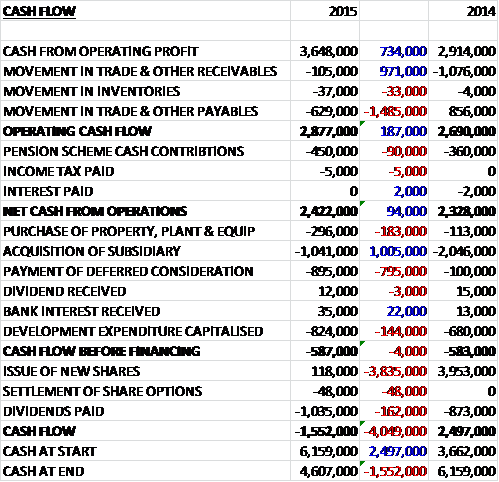

Before movements in working capital, cash profits increased by £734K to £3.6M. There was an outflow of cash through working capital, in particular a decline in payables. The pension scheme cash contribution was slightly higher and the net cash from operations was £2.4M, an increase of £94K year on year. The group spent £824K on development expenditure and £296K on tangible assets and this year there was also £1M spent on an acquisition and £895K on deferred consideration which meant that before financing there was a cash outflow of £587K. The group also spent £1M on dividends to give a cash outflow of £1.6M for the year and a cash level of £4.6M at the year-end.

Overall trading results for the year are in line with market expectations but the order book is somewhat lower than at the end of last year, down by £60K to £2.35M. During the year, pre-contracted revenues accounted for 51% of the total and some 21 new customers were gained.

The operating profit at the multi-channel business was £1.9M, a growth of £748K year on year. Mobile enablement and deployment continues to be a key business driver in this sector with increasing levels of activity. The acquired One Iota business increased revenues by more than 70% during the year but it is not clear how much profit the business contributed. The wholesale distribution and cash and carry market has been a slower area of business during the year but prospects for the coming year have improved, driven by the latest enhanced version of software. Proteus has made a steady start as a subsidiary of the group, contributing £58K of profit.

In the coming year management expects to focus further efforts on delivering growth across the digital retail market, where the One Iota business has a growing presence. Several new customers were gained in the division including Anzac Wines and Spirits, Superdry and Matthew Algie with continued large orders from existing customers who generally invest in the latest technologies to attract new customers and maximise sales. The year-end order book fell by £30K to £1.45M but with good sales prospects, the division is apparently well positioned to achieve its increased trading targets for the current year.

The operating profit at the manufacturing business was £502K, a decline of £375K when compared to last year, although some £109K of this fall was due to restructuring costs. The overall divisional trading performance was lower than expected in contrast to the strong performance last year. The group is focusing their investment in new products on the food and drink business. Traceability of products and ingredients through the food manufacturing and supply chain is a strong feature of the group’s offering but the business operating in this market saw some delay in the receipt of expected sales orders and delivered a lower level of profitability as a result. One large order values in excess of £400K was gained just after the year-end, however, outlook for the current year is much improved.

The business which addresses the general manufacturing market improved its trading performance which is expected to continue into the current year. The introduction of the new Unity Express ERP product aimed at new and emerging manufacturing businesses has proved successful and three new customers were gained in the year, albeit at an average contract value in the region of £35K compared to the average value experienced by the rest of the group of £75K across the new customer contracts signed this year.

Eleven new customers were gained during the year including Simtom Food Products, Summit Chairs, St. Marcus Fine Foods, Wine Bottling Solutions, Purdie Dished Ends and Nutri Fresh. Large projects with existing customers include Food Partners, Cook Trading ad Freddy Hirsch. Recurring revenue represents over 58% of total divisional revenue and covers over ¾ of divisional overheads. A good start to the current year together with a strong sales prospect list should ensure that the manufacturing division achieves a much improved trading result for the year.

On the 5th December the group acquired Proteus Software for a maximum consideration of £1.9M with £1.4M paid in cash on completion and up to £500K will be payable subject to certain performance targets up to December this year. Based on current forecasts, management expect to pay £191K in January. The business provides warehouse management solutions to customers in the areas of third party logistics, warehouse management and supply chain distribution. The acquisition generated goodwill of £1.1M and in the ten months since purchase has contributed £58K to pre-tax profits.

On the 8th June 2015 the group made a small acquisition of Evogenic for a maximum consideration of £445K with £110K paid in cash on completion, deferred consideration of £60K to be paid at six monthly intervals starting this month and further contingent consideration of up to £275K that will be payable subject to certain performance targets in the three years to June 2018. Based on current forecasts, management expect to pay £238K over the three year period. The business has developed an ERP solution to meet the demands of SME manufacturers and distributers and last year it generated pre-tax profit of £5K and contributed £5K to group pre-tax profits since acquisition.

The increase in deferred consideration charge of £252K relates to a change in the calculated value of deferred consideration by discounting expected future cash payments using the company’s cost of capital. The discount is then charged to the income statement over the period of the deferral. As a result of certain payments in respect of One Iota being paid earlier than previously forecast, an accelerated charge of £252K has arisen, which is a non-cash item and rather than reflecting an increased amount, reflects an earlier payment.

During the year Ian Newcombe, who has apparently made a major contribution to the formation of the group’s strategy, driving the development of the multi-channel business, was appointed CEO of the group. They also appointed David Gutteridge as a non-executive director. He has previously been at Financial Objects and Cyan Holdings and was also a non-executive of the group from 2004 to 2012. Until May 2014 he was Chairman of Tinglobal who were sold to the Singapore business, Declout.

Revenues derived from the digital retail market have grown from £4.53M last year to £5.87M this year and going forward the board intends to report its breakdown of divisional results in terms of a digital retail business division and an Enterprise software division which consists of a manufacturing business and a warehouse and logistics business. The board will continue to invest in the ERP software businesses in order to ensure that the product offering continues to attract new customers. The combination of more rapid growth available via a digital retail division and the steadier growth from the Enterprise software business is expected to enable the group to meet its strategic targets over the next three years.

The board are confident that they will make further progress and deliver trading results that are at least in line with market expectations for 2016.

At the current share price the shares trade on a PE ratio of 20.1 which falls to 13.2 on next year’s consensus forecast which is not exactly that cheap. After a 20% increase in the final dividend, the shares currently yield 3.1% which increases to 3.4% on next year’s forecast which is a useful pay out in my view.

Overall then, this has been a fairly slow but decent year for the group. Profits did increase, as did operating cash flows but there is very little free cash generated, and certainly none after the regular acquisitions are paid for. The balance sheet doesn’t look great either (not uncommon for a software company) with a negative tangible book value which has got worse over the past year. Operationally, the multi-channel division performed well driven by digital retail demand but the order book looked rather flat at the year-end. Conversely the manufacturing division performed poorly due to the delay in some orders from the food manufacturers but the order book is looking much better after the receipt of a big order after the year-end.

I like the comment about current trading being at least in line with expectations but overall things are moving slowly here and the negative net asset value is not ideal in my view. Although I will continue to monitor the company, I think this will be my last update until something major changes.