Character has now released its final results for the year ended 2015.

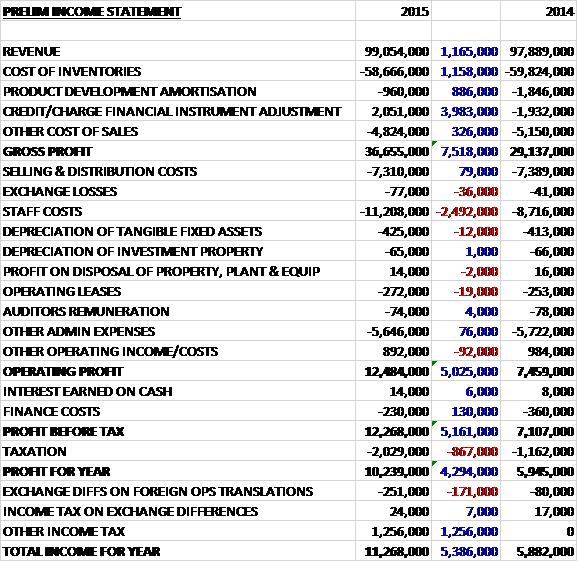

Revenue increased by £1.2M when compared to last year and cost of sales fell by £1.5M. We then see an £886K reduction in the product development cost amortisation and a £4M positive swing with regards the credit from the foreign exchange hedge market value change which gave a gross profit some £7.5M above that of 2014. Selling and distribution costs were broadly flat but staff costs increased by £2.5M so that the operating profit was £5M ahead. Finance costs reduced somewhat but this was offset by an increase in taxation to give a profit for the year of £10.2M, an increase of £4.3M year on year.

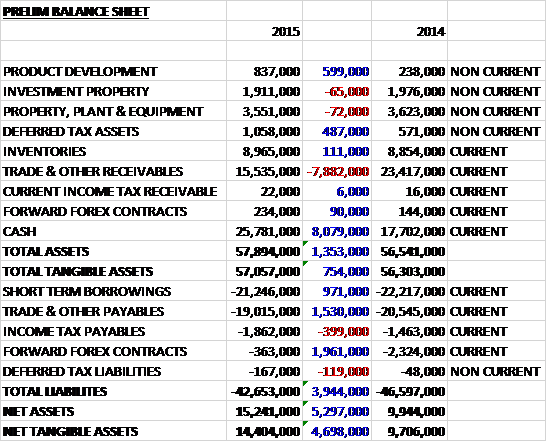

When compared to the end point of last year, total assets increased by £1.4M driven by an £8.1M growth in cash partially offset by a £7.9M fall in receivables. Total liabilities declined during the year due to a £2M decrease in forward forex contracts, a £1.5M fall in payables and a £971K decline in short term borrowings. The end result is a net tangible asset level of £14.4M, a growth of £4.7M year on year.

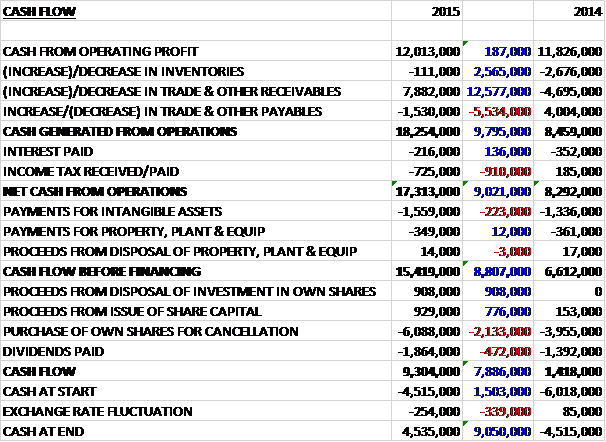

Before movements in working capital, cash profits increased by £187K to £12M. A large fall in receivables was only partially offset by an increase in tax payments and the net cash from operations came in at £17.3M, an increase of £9M year on year. The group then spent £1.6M on development costs and £349K on property, plant and equipment to give a stonking free cash flow of £15.4M. The group paid £1.9M in dividends and purchased £6.1M worth of their own shares which meant the cash flow for the year was £9.3M to give a cash level of £4.5M at the year-end.

The domestic market has trading ahead of expectations but international sales were hampered by adverse exchange movements and a generally difficult economic climate. Going forward, the board expect their international trade to return to normal. The most important brands during the year included Peppa Pig, Minecraft, Fireman Sam, Teksta, Little Live Pets, Scooby Doo, Doctor Who and their activity ranges. The UK subsidiary has been appointed the global master toy partner for Teletubbies and the new line of these characters will be launched in early 2016.

The company continues to win awards for its toys with Character Options being awarded Toy Supplier of the Year at the Toy Industry Awards last January. Product awards were also received for best gaming toy (Minecraft), best interactive toy (Little Live Pets) and joint winner in the Craze of the Year (Cra-Z-loom bracelet maker). The group also received supplier awards from both Argos and Tesco.

A significant portion of the group’s purchases are made in US dollars so they are exposed to foreign currency fluctuations and they manage the risk through the purchase of forward exchange contracts and derivative financial instruments. The group is required to make an adjustment to its financial statements to incorporate a mark to market valuation of these instruments. This has resulted in a credit to the income statement of £2.05M compared to a charge of £1.93M last year. It is unclear to me whether this should be taken out of the results or whether this corresponds to a similar increase in costs due to the appreciation of the dollar and should therefore be included. It is very difficult to make a judgement on this company without knowing this as the bulk of the profit increase is explained by the revaluation.

During the year the group spent over £6M buying back 2,336,330 shares in the company. It remains part of the group’s overall strategy to continue to repurchase shares where appropriate but this will now be limited to a maximum 15% of the issued share capital during the year.

The pre-tax profit figure for the year is apparently ahead of results anticipated and current trading remains encouraging and in line with management expectations. At this stage, the board believe that their underlying performance should be able to deliver another year of solid progress.

At the current share price the shares trade on a PE ratio of 10.5 which is expected to remain the same next year – so no growth is forecast in 2016 then. After a 52% increase in the total dividend this year, at the current share price the shares yield 2.3% which increases to 2.5% on next year’s consensus forecast.

Overall then, this set of results has left me a bit confused. Profits were up but this was due to the credit regarding the mark to market of the forex hedge and lower product development amortisation. Net assets did increase as did operating cash flow, although the latter was mostly due to a large fall in receivables which gave a stonking free cash generation. Operationally it is very difficult to see what is going on, there is almost no detail at all. The only thing I can deduce is that the domestic market has done well whilst the international market has struggled. The PE ratio of 10.5 makes the shares look cheap and the 2.5% dividend is OK. The fact the PE is not forecast to fall next year is a bit of a concern, however, given the likelihood of more share buybacks.

Overall as I say I am a little confused about this. The crux of the performance is really down to the forex valuation. Is the mark to market credit offset by higher purchase costs or not?

On the 7th December it was announced that non-executive director David Harris purchased 2,603 shares at a value of £12.5K to give him a total of 46,700 shares overall. Whilst nice to see directors buying, this is not exactly a huge amount.

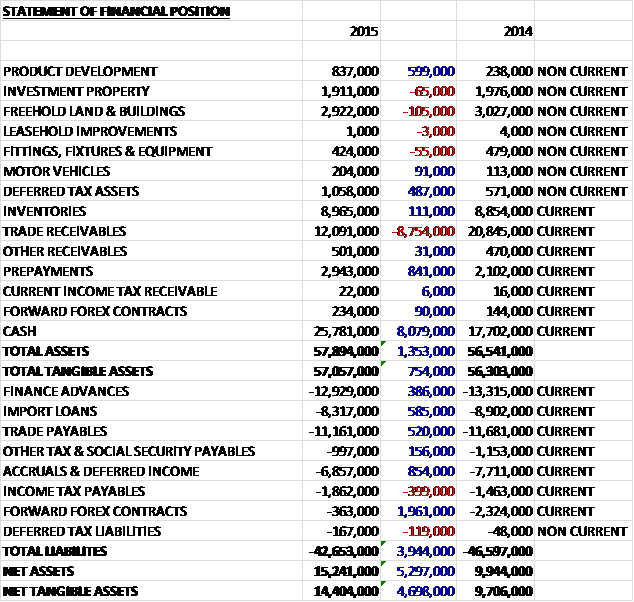

Character has now released their annual report and there is a bit more detail in this update, but not all that much! The more detailed balance sheet is below:

Within the modest increase in assets we can see that the £8.1M growth in cash was offset by an £8.8M decline in trade receivables. Within the decline in liabilities, the main change was the £2M decline in forward forex contract liabilities along with a few other smaller decreases.

I suppose the most useful bit of information is the adjusted operating profit split by region. In the UK the operating profit stood at £4.5M, a growth of £2.3M year on year; in the Far East, the operating profit was £7.4M, a decline of £1.4M when compared to last year; and in the rest of the EU, the operating profit was just £6K, a fall of £97K year on year.

On the 24th December the group announced that non-executive director David Harris purchased 1,703 shares at a cost of £8K. He now owns 48,403 shares in the company.

On the 22nd January the group released a trading update from their AGM. The group continues to perform well, with sold Christmas period sales across all major lines. To date, sales in the current year are up about 6% over the same period of last year and the board fully expect their underlying performance to deliver another year of solid progress and they remain on track to meet current market expectations.

The ongoing performance of the established cornerstone brands including Peppa Pig, Minecraft and Fireman Sam continue to be very encouraging and a number of new introductions will be coming to market over the coming year, including the new ranges based on the Teletubbies characters which was launched this month. Overall, early reaction to the new ranges has been enthusiastic and the board are confident that the offering will deliver in terms of demand and sales across both the UK and international.

Overall then, a decent, steady update. I continue to hold.

On the same date the group announced a number of director changes. One of the founders and exec chairman, Richard King intends to relinquish is executive role and will remain as non-executive chairman. Kiran Shah and Jon Diver who currently share the MD role along with their other roles of Finance Director and Marketing Director respectively are relinquishing their secondary roles and remaining as joint MDs. Therefore, Mark Dowding, current CFO is promoted to the position of group Finance Director and current Marketing Director of Character Options ltd will be promoted to Group Marketing Director.

Following the passing of non-exec Lord Birdwood last year, the group have appointed Clive Crouch as a non-executive director. He was a member of the senior team that launched GMTV and held the role of COO before establishing his own media consultancy business. These changes sound sensible to me and should help the group to be a bit more professional as a public company.