Photo-Me has now released its interim results for the year ending 2016.

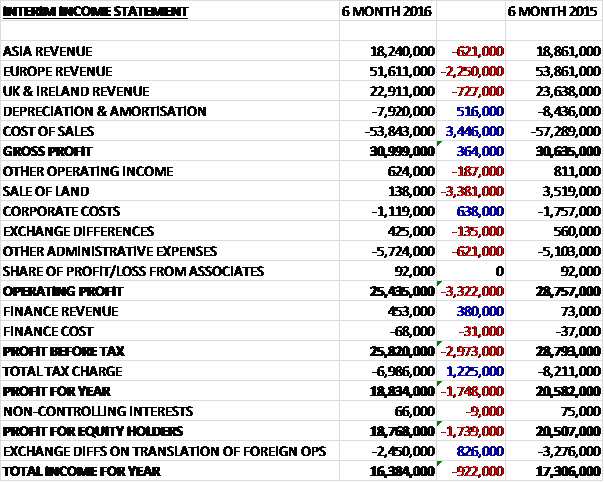

Revenues fell when compared to the first half of last year due to adverse currency movements (they showed modest growth on a constant currency basis) with a £2.3M decline in European revenue, a £727K decrease in UK and Ireland revenue and a £621K decline in Asia revenue. Depreciation and amortisation also fell by £516K and other cost of sales declined by £3.4M so that gross profit increased by £364K. Other operating income fell by £187K, and there was a £135K decline in gains from exchange differences with a decrease in corporate costs broadly offset by an increase in other admin expenses but the lack of the £3.4M gain on the sale of vacant land at Bookham meant that operating profit was down by £3.3M. Finance revenue increased by £380K and the total tax charge fell by £1.2M which meant that the profit for the year came in at £18.8M, a decline of £1.7M year on year.

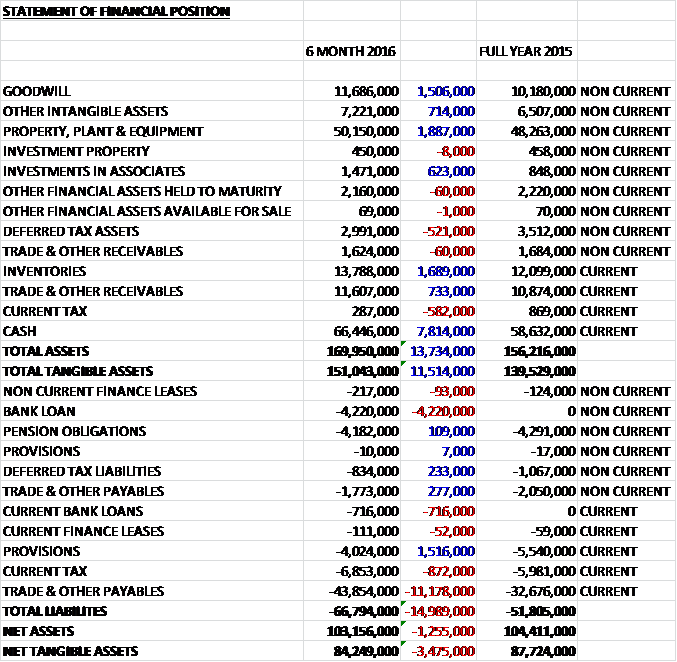

When compared to the end point of last year, total assets increased by £13.7M driven by a £7.8M growth in cash, a £1.9M increase in property, plant & equipment, a £1.7M growth in inventories and a £1.5M increase in goodwill. Total liabilities also increased during the period as an £11M growth in payables and a £4.9M increase in bank loans were partially offset by a £1.5M fall in provisions – I am a little uneasy about the large increase in payables and the new bank debt given the large cash pile – what is that for? The end result is a net tangible asset level of £84.2M, a decline of £3.5M over the past six months.

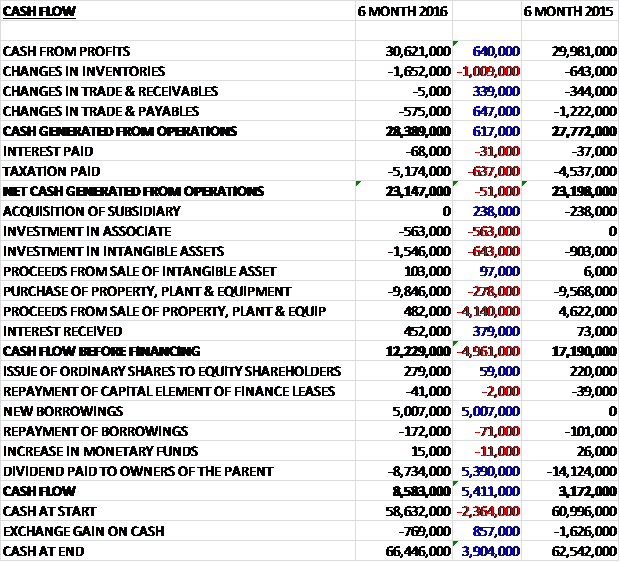

Before movements in working capital, cash profits increased by £640K to £30.6M. There was a modest outflow of cash through working capital, in particular an increase in inventories and taxation was £637K higher to give a net cash from operations of £23.1M, broadly flat year on year with a £51K decline. The group spent £9.8K on property, plant & equipment, mainly relating to photo booths and vending machines, £1.5M on intangible assets relating to R&D, and £563K on investments in an associate to give a free cash flow of £12.2M, of which £8.7M was spent on dividends and inexplicably the group took out £5M of new borrowings which meant that the cash flow for the period was £8.6M and the cash level was £66.4M at the period-end.

The operating profit in the Asian business was £3.5M, an increase of just £26K year on year. The largest territory by far is Japan where performance was strong in the first half. Revenues were up by 2.8% at constant currency with profits up 10% on the same basis. The medium term outlook for Japan is good with the government introducing new ID cards for every resident in the country from 2016 to be used primarily for tax and social security purposes. Asia is seen as a promising market for the laundry product in the medium term and the group is intending to start trials in Japan and China. Gradual progress continues to be made in China and Korea where turnover rose by 23% and 123% respectively, albeit from a low base.

The operating profit in the European business was £17.6M, a decline of £846K when compared to the first half of last year. On a constant currency basis, photo booth turnover grew by 2.7% with the takings of the laundry machines operated by the group more than doubling. On a constant currency basis, operating profits rose by 3.8%. The European photo booth estate increased by 1.4% year on year with the main areas of growth being France, Germany and Switzerland where in spite of the challenging conditions of the mature ID photo market, the performance benefited from the continued rollout of higher margin Starck booths. Across Europe, 3,263 Starck booth have now been deployed.

The rollout of the laundry product continues to progress well. At the end of the period, the group had sold 497 of these units and operated 1,200. The results from the units in operation in France, Ireland and Portugal remain encouraging with monthly takings averaging €1,400 during the period across the more established machines in the operating estate. In the six month period, the turnover of the laundry business increased by 90% to £5.5M.

The most recent laundry launch has been in Spain, a new territory for the group, where there are now a handful of units with supermarkets and petrol stations being the initially targeted sites. They are also considering additional country launches. The gradual planned expansion of capacity in the manufacturing facilities for the laundry business is proceeding according to plan with a current capacity of about 80 units per month. The group has recently finalised the design of “Revolution 2”, expected to be launched in 2016, which again comprises three machines but with a footprint of only 5sqm compared with 10sqm for the current model. This is expected to increase the potential market for the product overall and is likely to be more attractive in Far Eastern markets.

The group continues to operate over 4,700 digital printing kiosks, primarily in France and Switzerland, which are being progressively upgraded to accept all models of memory cards and other media. The new Starck design kiosk has also recently been introduced into a number of locations in France. The new kiosks are fully integrated to major social media networks and enable easy photo printing from smartphones. The initial results of that new product range are promising and trialling will continue in France in coming months. Aside from the new printing kiosk and new versions of the Starck photo booth, work continues on the 3D technology, a compact version of the automated laundry product as well as the optimisation of the energy consumption in photolights.

The operating profit in the UK and Irish business was £5.5M, an increase of £379K when compared to the first half of 2015, driven by operational cost optimisation despite a contraction in turnover. Growth in photo booth numbers was 1.6% year on year while there was a 20% reduction in amusement machines which perform below the group profitability standards due to increasing maintenance costs.

During the period the group signed a five year agreement with Moneygram which would see them roll out money transfer services at Photo-Me’s photo printing kiosks worldwide. They are developing a specific version of its kiosks enabling the new service to be launched on a trial basis in France in 2016. The group have agreed with Karcher, a three year exclusivity in the French car wash retail market in order to support possible larger scale expansion after the trial period. The focus is now on rolling out their laundry product line aggressively with an increasing focus on developing new markets for the photo printing lines and the photobooths, through 3D and extensive technological enhancements to anticipate the new standards in 3D face recognition.

I am a little confused as to why the group has taken out loans of £4.9M when it has cash of £66.4M. I am also a little concerned that in their net cash calculation they are not including the non-current bank loan of £4.2M – why not? Are they trying to hide it?

In October the group acquired Fowler UK.com, a business that supplies and installs laundry and catering equipment. The total consideration paid was £2.3M consisting of “accrual for investment” (whatever that is) of £1.9M and contingent consideration of £400K. The group expects the distribution of the group laundry equipment to be facilitated by using Fowler, which also has an established network of service engineers. The business also has good expansion opportunities in the wider laundry business under the group’s ownership.

Historically the first half of the year is seasonally the stronger for the group and this is expected to be the case again for this year but overall the board remain confident of the outlook for the business over the rest of the year. After a 10% increase in the interim dividend, at the current share price the shares have a dividend yield of 3.3% which increases to 7.4% on the full year forecast.

Overall then, this has been a bit of a mixed six month period for the group. Profits fell year on year but this was entirely due to last year’s sale of the vacant land at Bookham and underlying operating profits were broadly flat. The net assets did fall, though, as the group took out a loan and the payables increased considerably. The operating cash flow was broadly flat due to an increased tax payments but the cash profits increased and the group generated a decent amount of free cash. Operationally, both Asia and Europe suffered from forex movements which meant that operating profits were flat and declining respectively (both increased on a constant currency basis). In the UK, profits did increase due to lower costs.

As usual there are a number of schemes that are being considered with the car wash concept undergoing trials and the money transfer service a new one on me (with not much information given either). The second half of the year is usually not quite as strong and this is expected to remain the same this time and with a lot of cash and a yield north of 3.3% the shares look decent value but I am a little uneasy about some of the items this time – I would have liked some explanation on the large increase in payables and the new debt – is it a hedge against further Euro weakness or are they stepping up for a large acquisition? So, in conclusion I am still invested here but am thinking about realising some profits to be on the safe side.

On the 8th January the group gave an update of trading in Japan where they are benefiting from the introduction of new ID cards for every resident in the country. Trading in Japan in both November and December showed a very significant uplift over the same period of the prior year, with takings about 90% higher which is well ahead of board expectations. Whilst to date, they have only seen an impact on trading in these two months, if a similar level of sales were to continue in the remaining four months of the year, then the group would expect to report results materially ahead of current market expectations. This is a good update but I note they leave wiggle room in case the rest of the year doesn’t match up.

On the 26th February the group released a trading update. They confirmed that trading in Japan during January remained strong, supported by the strong start of the “My Number” programme. For the group as a whole, Q3 turnover was 11% higher with profits up by 90% at constant rates. The much better than expected performance in Japan coupled with the year to date performance in the rest of the business where laundry continues to produce strong results leads the board to conclude that pre-tax profits for the year will be more than £40M. If the Japanese business continues its strong performance in Q4, the eventual outturn for the year is likely to be in excess of this.

Also, the group announced that they have a number of initiatives underway to introduce the next generation of secure ID technology into its booths and is announcing the start of a major initiative in France. They have obtained the first agreement with ANTS to allow the delivery of a digitised e-photo and signature, fully compliant with the new requirements. This document is sent from the photobooths via a secure server.

All of their French photobooths will be upgraded and capable of delivering this service and the new connected secure system is being deployed nationally, beginning in Paris. About 2,000 machines should be upgraded by the end of June and the balance converted progressively in the coming months, with the intention to complete the rollout before the end of 2016.

This approach provides a higher level of security to the French authorities and requires no investment by them. In addition, for the public it simplifies the license application process and is expected to be beneficial to photobooth usage and revenue. The group will provide further details of its other initiatives undertaken in the field, including its work in Germany, Switzerland and China at a later date.

On the 27th April the group announced that they are in discussions with Asda Stores to acquire their UK Photo Product division assets with a view to operating the business from Asda Stores. No further information is given at this stage.