Solid State has now released its interim results for the year ending 2016.

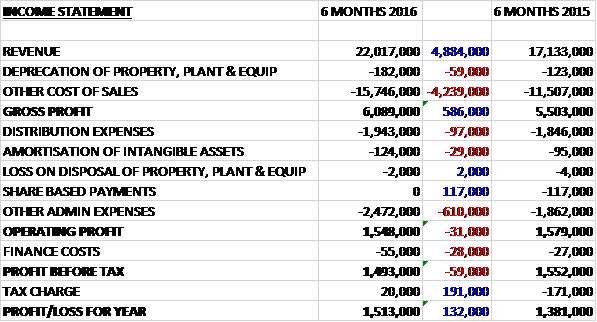

Revenues increased by £4.9M when compared to the first half of last year due to the first contributions from the MoJ contract and Ginsbury Electronics –like for like revenues were flat, but after a growth in cost of sales, the gross profit was just £586K higher. Distribution expenses grew by £97K but there was no share based payment this time which accounted for £117K in the first half of last year. Other admin expenses increased by £610K though which meant that the operating profit fell by £31K. A doubling of finance costs was more than offset by a £191K positive swing in taxation with a rebate this time to give a profit for the six month period of £1.5M, an increase of £132K year on year.

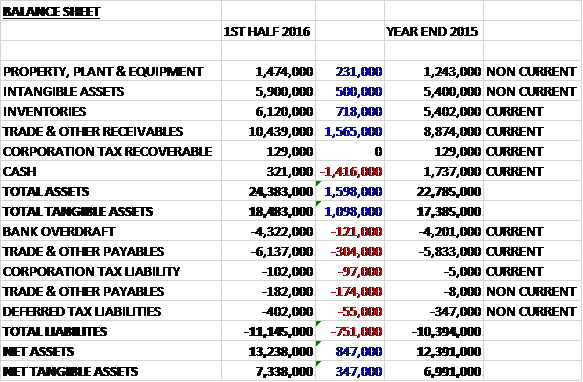

When compared to the end point of last year, total assets increased by £1.6M to £24.4M driven by a £1.6M growth in receivables, a £718K increase in inventories and a £500K growth in intangible assets, partially offset by a £1.4M decline in cash. Total liabilities also increased due to a £478K growth in payables and a £121K increase in the overdraft. The end result is a net tangible asset level of £7.3M, an increase of £347K over the half year period.

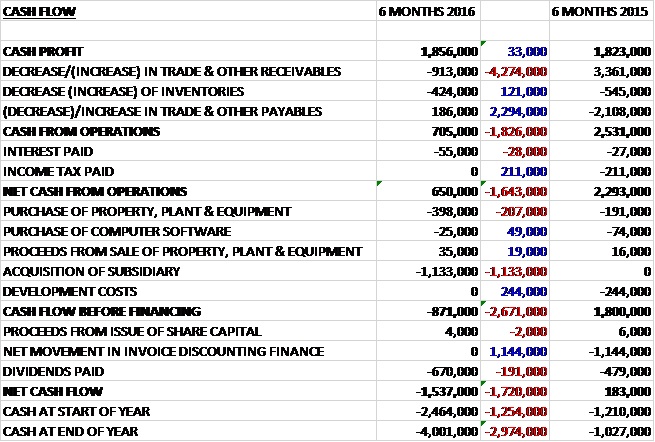

Before movements in working capital, cash profits were broadly flat, increasing by just £33K. A cash outflow from working capital, in particular an increase in receivables was partially offset by no tax being paid so that the net cash from operations was £650K, a decline of £1.6M year on year. The group then spent £398K on tangible fixes assets and £25K on computer software before the £1.1M spent on the acquisition meant that before financing, there was a cash outflow of £871K. The group then spent £670K on dividends that it couldn’t really afford to give a cash outflow of £1.5M over the six month period and a cash level of just £321K at the end of the half year.

The Steatite business faced a challenging first six months of the year due to a softening of the UK’s manufacturing sector and delays to two major programmes, one being the MoJ contract and the other being a programme to supply antennas, which is now underway and will make a contribution in the second half of the year. Due to these delays, however, the gross margins in the division were below that of last year. There have been some contract awards at a higher system integration level which will have a positive impact in the ensuing months along with the completion of a new design for ticketing machines for the rail industry with orders expected to start in the second half.

Construction is now underway on a new leasehold facility for the Q-Par antenna and subsystems operation close to the existing facility in Leominster. It is expected to open in Q1 2017 and will more than double capacity and incorporate a new group pre-compliance test centre which will increase in their in-house test capabilities and save outsourcing costs. The Steatite business has a healthy pipeline of prospects in the second half which include programmes in the government and transport sectors and its secure communications product range. As a result both the Steatite and Q-Par parts of the division are on course for a stronger second half.

During the period the group recognised £3.5M of revenue as part of the mobilisation element of the MoJ contract. This part of the contract is at low margins compared to the actual delivery part of the contract. Additional mobilisation revenue will be recognised in the second half of the year but will be less than in the first half. Unfortunately the delivery schedule to the contract has encountered delays. Steatite has to date fulfilled its contractual requirements but the overall project is made up of a consortium of suppliers and therefore there is a dependence on other parties for the project to roll out in unison as a fully operating upgrade to the existing offender tagging estate. The group expect to be updated on the revised roll out to this client in the new year but no significant deliveries are now expected in the current financial year.

The supplies division has experienced a softening in its markets in the first half. Like for like margins were down but the overall gross margin was up as the division benefited from Ginsbury’s higher margin products. Client order patterns show that the industry as a whole has moved from committing to long term scheduled orders to placing shorter term orders which is consistent with previous periods of market softening. The effect of this is a reduction in the order backlog, but billings are holding which demonstrates that the overall demand has largely remained constant despite the reduced revenue visibility.

The business negotiated two important new franchise contracts with Luminus and Silicon Labs. Luminus brings new high value products to the LED lighting sector of the business and is expected to start contributing to revenue in Q4 this year whilst Silicon Labs is a supplier of low energy microprocessors and radio devices with additional revenues expected in 2017. Commission income on overseas or indirect sales has improved during the period and is now 50% above forecast, in line with the growing recognition from suppliers of the design work carried out by the company in the UK.

At Ginsbury, turnover is currently running behind plan but concerted efforts to increase margin have seen the gross profit margin up 2% thus reducing the impact of the lower sales on net profit. Efforts to generate new sales through cross selling with Solid State Supplies are progressing well and cross training has been completed with some early sales successes already recorded. Furthermore, the single board computer platform developed as an own brand product range by Ginsbury has been well received with several potential customers now evaluating it. Recognising the softening in its market, however, the division has taken steps to reduce its cost base and as a result expects to see a stronger performance in the second half.

At the beginning of the year, the group completed the acquisition of Ginsbury Electronics for an initial cash consideration of £1.6M and a further £525K payable in three equal six month tranches. The business specialises in the supply of high quality display components, monitors, panels, signage and power components to the commercial, retail, industrial and military markets throughout the UK and Europe. It is expected to make a positive contribution to the performance of the group in the current financial year. The board remains active in pursuing acquisition opportunities, particularly in the battery and added value services sectors.

The group have announced they will be appointing Mark Nutter as finance director and he will start in January. At the period-end, the order backlog stood at £18.1M and as in previous years, the order intake and sales performance is expected to be second half weighted. The announcement of delays to the MoJ contract has caused expectations for the group to be revised for the current year and at present the board do not have visibility on how the contract will impact the next financial year. While they are pressing for clarity on the issue, it remains largely out of their control. The project is high priority for the MoJ and the directors are confident that the contract will be fulfilled.

A softening in the group’s markets have resulted in a slower start to the year than the directors would have liked. Nevertheless they remain confident about the prospects across the group and expect an improved performance in the second half. In response to the current state of the market the board has implemented a cost reduction programme which will deliver savings of approximately £500K in the full year of 2017. After the interim dividend remained the same, at the current share price the shares yield 2% which is expected to remain the same on the full year consensus forecast.

Overall then this has been a fairly difficult half year period for the group. Profits did increase but this was only due to a tax rebate and pre-tax profits were down. Net assets did improve but the operating cash flow fell due to an increase in receivables with cash profits broadly flat. The Steatite and Q Par businesses saw softening in their markets which was exacerbated by delays to an antenna supply contract, which has now started, and the MoJ contract which is still clouded by uncertainty over the timings. The supplies business has also seen softening markets, although it did benefit from the Ginsbury acquisition.

The group’s markets seem to be worsening and the delay to the MoJ contract is an unwelcome concern. With a dividend yield of 2% and a forward PE ratio of 18 these shares do not seem to be factoring in these risks in my view and look too expensive.

On the 25th February the group announced that it had been informed by the MoJ that it was terminating the contract for Electronic Monitoring Hardware. The group is to enter discussions with the MoJ regarding the terms on which the relationship will end. This is very disappointing since in the past the board had stressed there was a delay only and the contract was still going ahead. This was supposed to be very material for the group so is a major set-back. The silver lining is any compensation they may be due from the MoJ regarding the termination and the reduction in the share price has actually brought this down to an area that I am much more interested in.

On the 27th April the group released a trading update covering the year ended 2016 in which they stated that trading in their core businesses is expected to be in line with market expectations. The overall final result for the year will be dependent on the completion of negotiations in relation to the settlement of the terminated contract with the MOJ which are now at an advanced stage. The group has entered the new financial year with healthy order books although on a like for like basis the backlog of £13.94M was below the £14.41M at the end of the prior year. Including Ginsbury, which was acquired during the year, however, the backlog was £15.34M.

On the 1st June the group announced the acquisition of Creasefield for a maximum consideration of £1.54M. A cash consideration of £1.4M will be paid on completion from the group’s existing bank facilities with a further £140K payable once completion accounts are agreed. The business specialises in the design and manufacture of custom battery packs to a diverse range of industry sectors such as commercial aerospace, oil & gas, medical, subsea, safety, water, rail, military, security and government. Their operations are complementary to the existing battery operations at Solid State and will allow for wider use of IP, design and engineering capability, cross-selling of existing products and development of sales into new markets.

Last year the business generated an EBITDA loss of £60K and the acquisition generated goodwill of about £71K. The board believe that Creasefield will make a limited but positive contribution to the group performance for the rest of the year and a more significant contribution in 2018. Overall, this looks to be a decent, albeit small, acquisition.