Goodwin has now released its interim results for the year ending 2016.

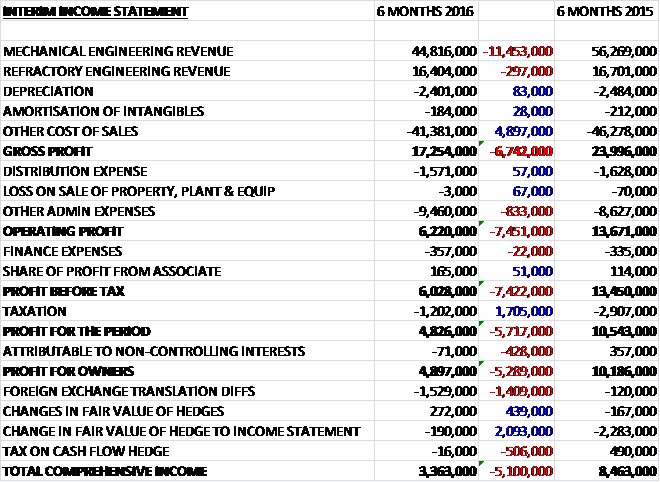

Revenues declined when compared to the first half of last year with an £11.5M fall in mechanical engineering revenue and a £297K decrease in refractory engineering revenue. Cost of sales also decreased which meant that gross profit fell by £6.7M. Admin costs increased, however, so that the operating profit declined by £7.5M before a decrease in taxation gave a profit for the half year of £4.9M, a decline of £5.3M year on year.

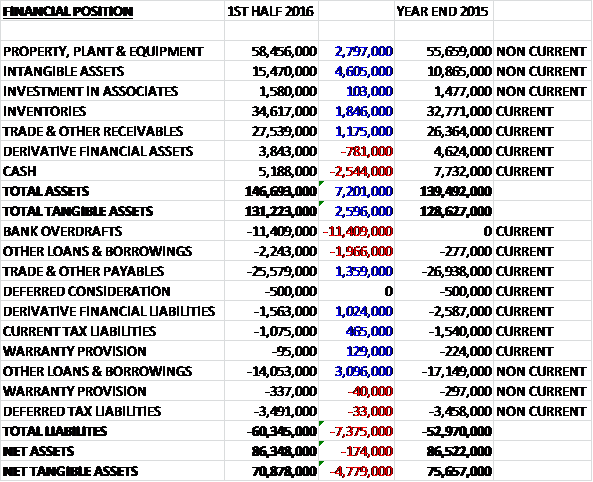

When compared to the end point of last year, total assets increased by £7.2M driven by a £4.6M growth in intangible assets, a £3M increase in property, plant & equipment, a £1.8M growth in inventories and a £1.2M increase in receivables, partially offset by a £2.5M decline in cash. Liabilities also increased during the period as an £11.4M increase in bank overdrafts was partially offset by a £1.1M fall in other loans and borrowings, a £1.4M decrease in payables and a £1M decline in derivative financial liabilities. The end result is a net tangible asset level of £70.9M, a decline of £4.8M over the past six months.

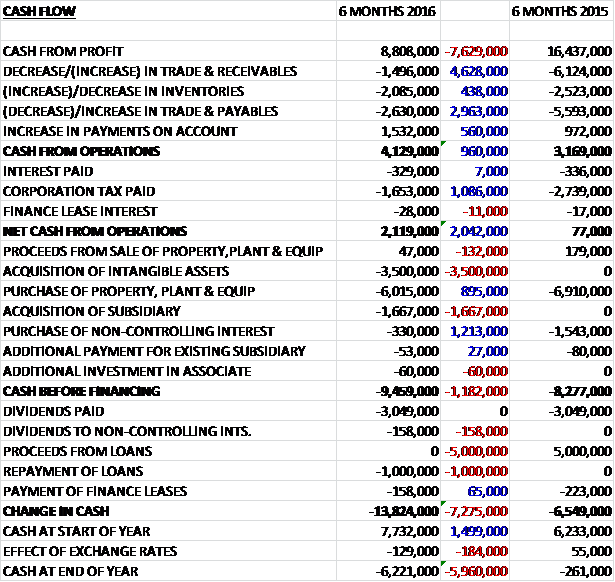

Before movements in working capital, cash profits declined by £7.6M to £8.8M. There was then a cash outflow from working capital, although this was much lower than last year, in particular a smaller increase in receivables which is expected to reverse in the second half of the year. After a £1.1M decline in tax paid the net cash from operations came in at £2.1M, a growth of £2M year on year. This did not come close to covering the £6M spent on tangible fixed assets relating to investment in new machinery for Goodwin International, the £3.5M spent on intangibles and the £1.7M paid for the acquisition so that before financing, there was a cash outflow of £9.5M. The group then paid out £3M in dividends which it couldn’t really afford and repaid £1M of loans to give a cash outflow of £13.8M for the half year and a cash level of -£6.2M at the period-end.

As previously indicated, the group started the year with a work load 22% lower than the year before and this coupled with tighter pricing in the difficult market has led to the reduction in profits. The sales order input during the period was 16% higher than in the same period last year but this increased level of order input was only achieved by quoting tenders with tighter margins.

Good progress was made in expanding the activity of the refractory engineering division. Towards the end of last year, Goodwin Refractory Services purchased the assets of a casting powder company and now supplies a significant amount of tyre tread moulding powder both in Europe and Asia pacific. In October 2015, Dupre Minerals and Hoben International purchased assets at a cost of £4.8M which enable both businesses to expand their manufacturing facilities to produce more vermiculite and perlite. It is hoped that this will start to generate significant benefits during the second half of the year.

In addition, the bulk of the rest of the £5.8M of capital expenditure related to investment in new machinery for Goodwin International to enhance and increase its machining capability to allow the business to further expand its specialist large five axis CNC machining capability. The board expect an increase of £8M in order input for this type of worth this year. Easat Antennas was awarded an R&D grant which over the next two years will enhance its radar supply capability and it is hoped that these activities will, in part, mitigate the effects of the downturn in the oil and gas and mining industries.

The profit in the Mechanical Engineering business was £5.4M, a decline of £6M year on year and the profit in the Refractory Engineering division was £1.6M, a fall of 802K when compared to the first half of last year.

A small electronics company was acquired during the period for a consideration of £1.6M which represented a provision intangible asset and goodwill value of £1.4M. In order for the group to take on larger contracts, an extra £10M line of five year committed bank facility (so far unutilised) has been arranged as payment cycles are less certain in current economic conditions.

Going forward, time will tell whether the group will find satisfactory levels of work to fill the gap temporarily caused by the slowdown in the oil, gas and mining industries which the board seem being quieter for a couple of years.

There was no interim dividend announced (just as last year) so the shares continue to yield 2.5% on an annual basis.

Overall then, this has undoubtedly been a difficult period for the group. Profits have declined with falls in both mechanical and refractory engineering, and net asset levels have increased over the six month period. The operating cash flow did improve but this was only due to a lower cash outflow from working capital than last time and cash profits declined with no free cash generated. The workload at the start of the year was poor but this has improved somewhat as the period progressed, although margins are now lower due to increased competition following the collapse in the oil and gas and mining industries. The group is trying to diversify away from these sectors nut it seems unlikely this will be enough to plug the gap left in profits and this company does not look a good investment until this uncertainty improves.

On the 17th March the group announced its Q3 management statement. In the first nine months of the year, revenues declined by £21M to £87.5M and pre-tax profit fell by £8.3M to £9M. There have been no significant adverse events and whilst many of the engineering customers in the oil, gas, mining and power generation businesses are having a difficult time, overall the order input for the nine month period has increased by 15% when compared to the same period of the prior year. This increase has in part been helped by the refractory engineering division continuing to grow and by the antenna systems business now having a record order book for primary and secondary radar. They are also obtaining significant valve orders for LNG terminals and for the Middle East.

For these reasons, the board do not expect next year to be as difficult as they had previously thought. During Q3 they purchased a casting powder company in China which is complementary to the slightly larger existing two Chinese casting powder companies which should help enhance critical mass and market share.

Overall, this is a better update than expected and I have taken a small position in what I consider to be a high quality company experiencing difficult markets.

On the 12th May the group announced that director Simon Goodwin purchased 1,874 shares at a value of £39K which gives him a holding of 97,307 shares.