Trifast has now released its interim results for the year ending 2016.

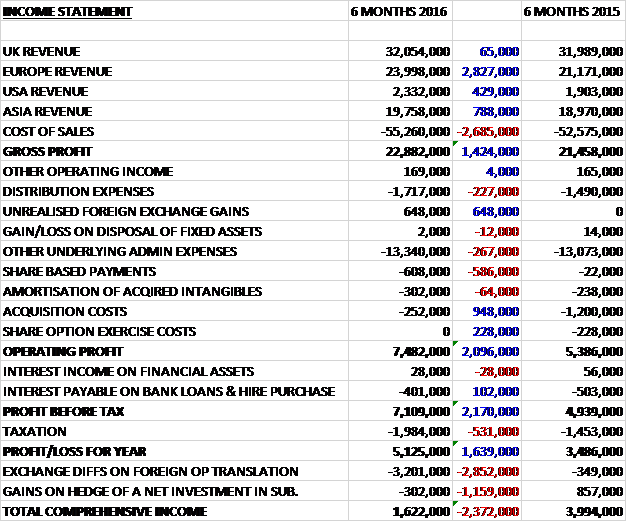

Revenues increased when compared to the first half of last year due to a £2.8M growth in Europe revenues, a £788K increase in Asia revenues and a £429K increase in USA revenue. After a growth in cost of sales, gross profit increased by £1.4M. Distribution costs increased by £227K but there was a £648K income from unrealised forex gains which more than offset the increase in other underlying admin expenses. We then see a £586K increase in share based payments offset by a £948K reduction in acquisition costs and a £228K fall in the share option exercise costs which meant that the operating profit increased by £2.1M. There was a reduction in the interest payable but this was more than offset by a growth in tax so that the profit for the first half of the year was £5.1M, an increase of £1.6M year on year.

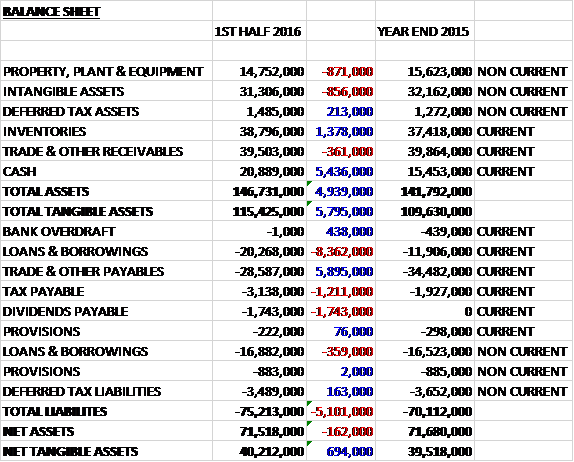

When compared to the end point of last year, total assets increased by £4.9M driven by a £5.4M growth in cash and a £1.4M increase in inventory, partially offset by an £871K fall in property, plant & equipment, and an £856K decline in intangible assets. Total liabilities also increased during the period as a £5.9M decline in payables was more than offset by an £8.8M growth in borrowings, a £1.7M dividend payable and a £1.2M growth in taxes payable. The end result is a net tangible asset level of £40.2M, an increase of £694K over the past six months.

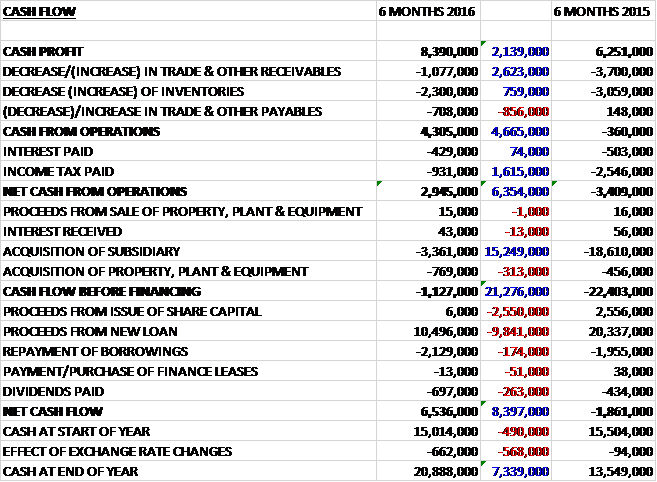

Before movements in working capital, cash profits increased by £2.1M to £8.4M. We then see a cash outflow from working capital (expected to reverse in the second half of the year), although this was less than last year and the tax payment was also below that of last time which meant that the net cash from operations came in at £2.9M, a positive movement of £6.4M year on year. The group then spent £769K on fixed tangible assets and £3.4M on the VIC deferred consideration so that before financing, the cash outflow stood at £1.1M. We then see £697K paid out in dividends and a net £8.4M taken out in new loans to give a cash flow for the period of £6.5M and a cash level of £20.9M at the end of the half.

Overall, the underlying operating profit at actual exchange rates increased by 22% to £8.6M with the organic growth in profits being £800K. The underlying operating profit in the UK business was £3.2M, an increase of £319K year on year; the underlying operating profit in the European business was £2.9M, a growth of just £44K when compared to the first half of last year; and the underlying operating profit in the US business was £247K, an increase of £54K when compared to the first half of 2015.

The underlying operating profit in the Asian business was £3.8M, a growth of £1.1M year on year. The Singapore location continued to perform very well with revenue growth of 19.5% but in contrast, the PSEP business in Malaysia reported a 9.6% decline in revenue. Both of these changes have arisen largely out of changes in product/sales quantities to specific key accounts in the region. The overall growth reflects increased business with certain key customers.

Sales in the UK and China were broadly flat, they fell in Hungary and Malaysia, whereas sales in the US, Sweden, the Netherlands and Singapore were substantially higher and the key customer order pipeline into 2016 apparently remains encouraging. The Italian operation continues to yield strong results and now the earn-out has been has been delivered, the integration of sales and marketing activities is gaining rapid momentum. Interestingly the group have stated that the cost gap between Italy and Taiwan is closing…

The factory extension at SFE in Taiwan has been completed and an additional section of new cold forging machines installed, increasing their total capacity in Taiwan by 15%. Before the end of the year, a six stage parts former, costing £1M, will be ready to commence production at PSEP in Malaysia. This will increase their capacity for complex larger components for the automotive, two wheel vehicle and compressor sectors. In the UK, this period has seen the trial and gradual introduction of computer controlled lean-lift stock storage and picking machines which are halving stock picking times and reducing warehouse space consumption so that the need for any new premises through business growth has been removed for the foreseeable future which in turn has led to the consolidation of the Poole warehouse into the Uckfield hub.

The group are looking at a number of new geographical areas, including Spain and Mexico for new business opportunities but there is no further information on this as of yet.

Just after the period end, the group acquired Kuhlmann for a total consideration of £6.2M. The initial amount of £4.9M was paid on completion in cash and £30K was satisfied by the allotment of 29,350 shares in the company. There is also a consideration of £1.2M deferred for a year and is to serve as a retention against which any potential warranty and indemnity claims will be offset. The group will be investing into Kuhlmann to further develop the opportunities in the German market and expect the acquisition to be earnings enhancing in the first full year of ownership.

Kuhlmann is a distributor of industrial fastenings within the domestic German market with a customer base in the principle sectors of machinery and plant engineering, sheet metal processing and industrial. The management team and previous owners will continue to run the business and last year it made a pre-tax profit of £1.4M, so a nice little business then which comes with goodwill of £2.2M and incurred costs of £300K. This buy should help the company in a large European market (the 4th largest industrial fastener market in the world) where they have apparently been constrained by the lack of a German speaking team.

The group have once again suffered from detrimental movements in exchange rates. The continued weakness of the Euro has reduced revenue growth from the European businesses by £2.1M and the recent depreciation of the Chinese Yuan and its wider impact on currencies across the Asian region has led to a decrease in the revenue from the Asian operations of £300K.

From the 1st October, Mark Belton took over as CEO after the retirement of Jim Barker who stays on as a consultant for the time being. Mark’s role of CFO has been taken on by Clare Foster who moves up from the position of financial controller.

Current global events have influenced the industrial sector’s confidence during the period but the group’s trading to date has not been unduly affected. Taking into account the current business climate the group are operating within, the board are optimistic about the group’s prospects and continue to expect its trading for the whole year to be in line with their expectations. As well as organic growth, the board have stated that they will continue to look for further acquisitions – I think I would rather they concentrated on bedding in the recently acquired businesses.

Looking forward, the order pipeline across the key locations remains healthy with continued sales growth expected primarily from Europe and the US but this is being tempered by a slight softening in demand in the UK where the group are starting to see some signs of hesitation and order deferral. In Asia, the substantial growth in the first half due to increased business with certain key customers has begun to slow down in the second half and at PSEP, slower order levels in the automotive sector are expected to continue in the short term. More positively, following the recent £1M capital investment programme, it is anticipated that the increased capacity in Malaysia will start to counteract any possible slowdown in 2017.

In Europe, the board expect organic sales to continue to grow on a constant currency basis and more generally the cost control and supply chain management is positively impacting margins, which will continue going forward, particularly with the ongoing investment into efficiency drivers such as the lean-lifts the group is rolling out across the UK business.

At the end of the period, the net debt stood at £16.3M compared to £17.5M at the same point of last time and £13.4M at the end of last year, although we should also note that just after the end of the half, the group spent £4.9M on the acquisition. After a 33% increase in the interim dividend, the shares are yielding 2% which increases to 2.1% on the full year forecast.

Overall then this has been a fairly good half year period for the group. Profits increased, net assets grew and operating cash flow improved, although this was not enough to cover the deferred consideration paid out. Profits improved in all regions with particularly strong growth in the UK, the US and Asia where an improved performance in Singapore more than offset weakness in Malaysia. European profits were broadly flat, not helped once again by Euro weakness, where a strong performance in Sweden and the Netherlands offset weakness in Hungary.

The capital expenditure seems to be doing fairly well, although a 15% capacity increase in Malaysia is fairly modest. The new picking machines in the UK sound very promising, however, with impressive efficiency savings and lower space requirements in the warehouse. The Kuhlamm acquisition does look good but I think I would rather the group concentrates on organic growth and brought the net debt down a bit which stood at £21.2M at the acquisition. The board have stated that full year expectations remain the same but the market in the UK is softening and the slowdown in Malaysia is continuing so this will have to be watched. In addition, the change of CEO suggest another potential risk. With a forward PE of 15.4 and yield of 2.1% the shares are decent value and I am tempted to buy in but there are nonetheless some potential banana skins in the near future which is holding me back a bit.

On the 16th February the group released a trading update for the last four and a half months. Whilst the UK industrial market has shown signs of some softening, the markets in both mainland Europe and Asia remain strong. Both Kuhlmann, acquired in Q3 and VIC, acquired in May 2014 are trading well and a combined investment programme of more than £1M is underway in both businesses to further develop the opportunities they have in their respective markets.

Sales enquiries remain brisk through the TR portal and this gives the board confidence in the continuing growth of the business. The order pipeline remains encouraging and they are in negotiations with a number of multinational OEMs to extend the plants they service and to widen the product ranges they currently supply so their long term expansion plans remain on track.

Although global sentiment and the Brexit debate might be influencing the current climate, from the group’s perspective, trading has not been unduly affected and they remain confident of meeting their full year expectations for 2016. Overall then, this is quite a nice update and I am tempted to take a position here.

On the 19th April the group released a trading update for the year. They had a strong finish to the year, benefiting from the ongoing focus on driving operational efficiencies, continued organic growth and a positive contribution from acquisitions. The board therefore expects the results for the year to be towards the upper end of market expectations.

Despite some slowness in the UK, the group’s markets in Asia and mainland Europe have remained strong and the order pipeline is encouraging, especially within automotive. The group have extended their relationship with a number of their multinational OEM customers by serving more plants and widening the product ranges they supply.

Following their investment programme in automation in Asia, Europe and the UK last year, the group are seeing an improvement in UK productivity whilst their operations in Italy, Malaysia and Taiwan have also benefited from this programme, giving them the opportunity to further extend sales and marketing initiatives on a domestic and global basis.

The German business acquired in October has performed slightly ahead of management expectations and the Italian business has had a solid year and contributed strongly, on a constant currency basis, to group performance.

Overall this all sounds good, probably already reflected in the share price but I might look to take a position on weakness.