National Grid is a company that I have been invested in for a while. They were perceived lower risk and something I used to diversify my portfolio somewhat. I am now going to attempted to decipher the rambling 200 page annual report and provide some meaningful analysis.

National Grid was listed on the London Stock Exchange in 1995 having been originally part of the British Gas group. The group is split into three main segments. The UK transmission business includes high voltage electricity transmission networks, the gas transmission network, LNG storage activities and the French electricity interconnector. The UK Gas Distribution business includes four of the eight regional networks of the UK’s gas distribution system. The US Regulated business includes gas distribution networks, electricity distribution networks and high voltage electricity transmission networks in New York and New England, and electricity generation facilities in New York.

Activities not included in the above business are a UK gas and electricity metering business, UK property management, a UK LNG import terminal and other LNG operations, US unregulated transmission pipelines, US gas fields and some corporate activities.

In the UK electricity industry, National Grid own some of the interconnectors with France and Netherlands which allows electricity produced in each country to be used to meet demand in the other countries and capacity on these interconnectors is sold through auctions. National Grid also owns and operates the transmission systems in England and Wales (power lines and the like) and are paid by generators, distribution network operators and suppliers to connect their assets to this system and to transport electricity on their behalf – these charges are reviews annually. These companies also pay the group to balance the system and to ensure demand is met.

As far as the US electricity business is concerned, National Grid owns 57 oil and gas power stations on Long Island and 4.6 MW of Solar energy units in Massachusetts. The group use this and also buy energy made available in the New York ISO market for their own requirements and to sell on. They also own and operate electricity transmission facilities in New York, Massachusetts, Rhode Island and Vermont. In addition they also own a transmission connector between New England and Canada and operate the transmission system on Long Island until the end of 2013, when that will be taken over by another company. They are permitted to recover the cost of electricity transmission from their customers as a transmission charge.

Distribution facilities actually transport the electricity from the substations to the end user. National Grid maintain and operate the distribution system in Long Island until the end of 2013 and own distribution facilities in New York, Massachusetts, Rhode Island and New Hampshire. Customer bills include the commodity rate, and a delivery rate. All the states National Grid operate in are deregulated and customers have the option of buying their electricity from other companies. If they do this, they are only charged by National Grid for distribution.

In the UK gas industry, National Grid owns and operates an LNG importation terminal at the Isle of Grain in Kent and the group charge importers to land LNG at this terminal. National grid are the sole owner and operator of the gas transmission infrastructure in the UK and all gas produced or imported must travel through their pipes. Shippers are charged for the use of this grid at both entry and exit of the system. There is also a commodity charge based on the actual gas flows through the system. When the gas leaves the transmission system it is odourised and enters the distribution system, where it can also be stored. National Grid own four out of eight UK regional distribution networks. The gas is still owned by the shippers and they pay for their gas to travel and be stored in the distribution network. These charges reflect the costs of building, maintaining and operating the network in addition to operating an emergency telephone helpline. It is unclear what kind of profit margin is built into the charges.

In the US, National Grid own and operate LNG storage facilities both for their own use and storage for third parties (for a fee). They purchase gas directly from the producers and importers for resale to customers. The group then pay to the owners of the national pipeline network to transport the gas to the local distribution networks owned by National Grid. This local network is used both for the gas that National Grid sell to customers and that belonging to third parties. Customers then have the choice of buying the gas through Nation Grid or other suppliers using the network (much like the deregulated US electricity market).

National Grid also have a joint venture with TenneT that built a subsea electricity link between the UK and the Netherlands, they have a metering service to install and maintain meters for energy suppliers in regulated market in the UK, they have a property company that manages their properties in the UK. They also have an interest in LNG storage and road transportation in the US.

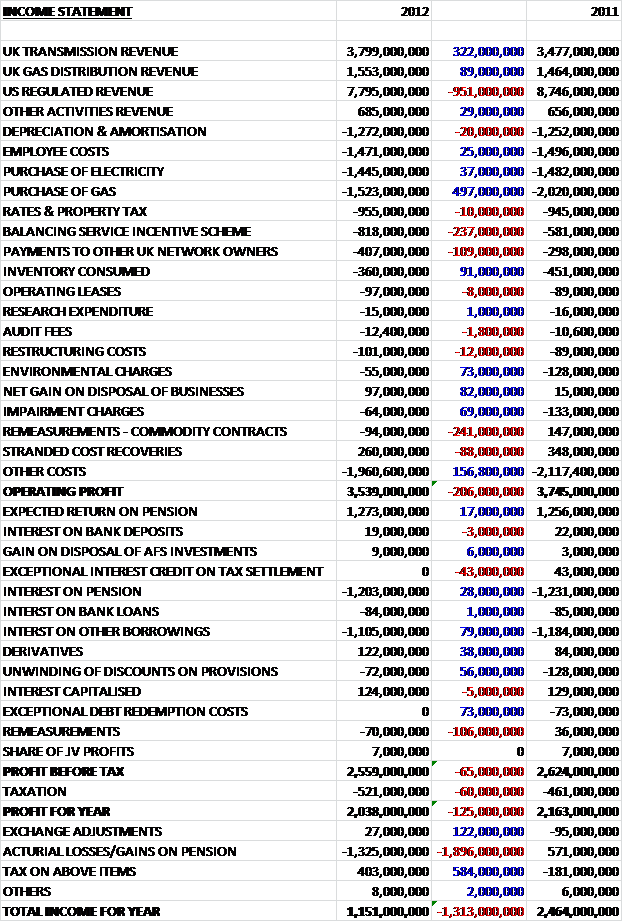

The income statement:

Starting from the top then, revenues were up across most business units, with the exception of the US business which fell by nearly £1B to £7.8B. The one thing I will say is that National Grid has a huge amount of assets – just look at that depreciation/amortisation charge – £1.3B! It was relatively unchanged from last year, however, as were the employee costs and electricity purchase costs (all of which were over £1B). The cost of the purchase of gas was down considerably (nearly £500M to £1.5B), whereas the balancing service incentive scheme was £237M higher to £818M – I am not too sure what that is, but it is a lot. Another large cost increase was the £109M increase to £407M for payments to other UK network owners. Again, I’m not too sure what has caused that but it is a big increase. The two other big swings to the negative when compared to last year were the remeasurements on commodity contracts (£241M swing to the negative to £94M) and the stranded cost recoveries, which were £88M lower at £260M. All this leaves the operating profit £206M lower at £3.54B.

As far as financial income/costs are concerned, the main driver is the interest on borrowings. This was a massive £1.1B in interest alone! This amount was lower by £80M, however, which was the main reason profit after tax was down by just £125M to £2.038B. Unfortunately a huge actuarial loss on the pension made the total income for the year £1.3B lower at £1.151B. Next year the group is expecting to pay £353M to the UK pension fund and £248M to the US pension fund. Restructuring Costs included £58M for severance provision & pension curtailment loss for restructuring the US operations; transformation related initiatives of £54M (£103M in 2011) and a credit of £11M for the release of restructuring provisions in the UK recognised in prior years. Environmental charges include £55M related to specific exposures in the US and are recoverable from customers (last year UK costs of £70M not recoverable).

Gains on disposal of £56M were for Seneca-Upshur, an oil and gas exploration business in the US; £16M for OnStream, a metering business in the UK and £25M for disposals in previous years, representing the release of unutilised provisions. The £64M impairment of intangibles due to the fact the LIPA management services contract will not be renewed. Stranded cost recoveries include recovery of some historical investments in generating plants that were divested as part of the power deregulation process in New England and New York in the 1990s – this was £279M in 2012 and it is thought to now be finished with no future recoveries. There was also a £242M tax credit relating to the change in UK corporation tax rate.

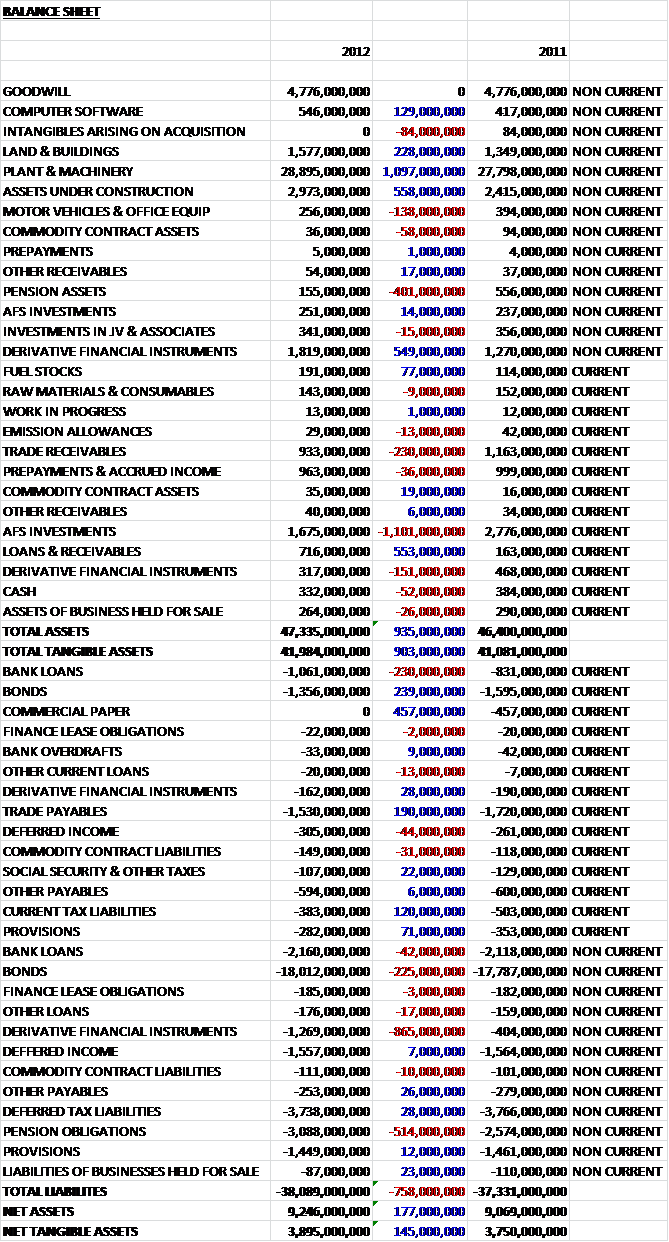

The Balance Sheet:

This year, total assets increased by nearly £1B to £47.335B. Of that, goodwill accounted for £4.776B and an investment in IT systems caused computer software to increase by £129M to £546M. The rest of the assets are tangible. Of these, by far the biggest, accounting for more than half of all assets was plant & machinery – presumably the equipment National Grid uses to transport gas and electricity – this increased by another £1.097B to £28.895B as the group extended their regulated networks (somewhat offset by depreciation and the offloading of the Onstream business). Assets under construction also increased considerably, as did the value of land and buildings. Other large increase included derivative financial instruments, up £549M and loans and receivables, which were up £553M. The loans and receivables are restricted cash balances and relate to collateral placed with counterparties which whom the group entered into a credit support annex to the ISDA Master agreement and pension scheme deficit contributions – if you understand that, you are doing better than me but I guess these are assets not readily usable. Not all assets were up, however, with the largest fall seen in Available for Sale investments, which were down by more than a billion to £1.675B. Other large falls were seen in Pension Assets and Trade Receivables, which were down due to warm weather experienced in the US. The assets and liabilities held for sale relate to the Energy North gas business and the Granite State electricity business in New Hampshire. Commodity contract assets fell in the US due to a fall in electricity prices. The group is still trying to gain regulatory approval for the disposals.

Total liabilities also increased, up £758M to £38.1B. The biggest increased here involved derivative financial instruments, whose liabilities increased faster than assets, up £865M to £1.3B and pension obligations, which increased by £514M to £3.088B due to changes in the discount rate following a fall in corporate bond interest rates – pensions seem to be a bit of a thorn in the side of many companies at the moment and this is quite a hefty obligation (albeit backed by a lot of tangible assets). Also I think worthy of note are the bonds. National Grid has a massive £18.012B debt in the form of bonds, which seems to be its preferred method of raising cash. This is an absolutely huge amount of debt which realistically is probably never going to get paid back (well, the individual bonds will, but as a whole I mean). During the year National Grid also launched its first RPI linked retail bond which attracted a big demand and raised £283M. It will also be noticed that there are over £1B of provisions, which mainly relate to environmental provisions that represent the estimated restoration and remediation costs for a number of sites. This is a lot of potential cash outflow…

The Cash Flow Statement:

After slight changes in working capital, cash from operations stood at an impressive £4.487B, down £367M from last year. After tax was paid, this was £630M worse than last year, at £4.228B because the group did not benefit from a one-off tax refund. So, where does all that cash go? Most of it goes on capital expenditure, and £3.147B went on the purchase of property, plant and equipment. We can also see that £203M was spent on computer software as the group overhauls its creaking IT system; £749M was paid in interest on the loans (down by £216M, but it still seems like a lot to be paying out) and just over £1B was paid to the shareholders in dividends. There were also a few inflows – the largest of which was the net movement in financial investments – this lead to a £553M inflow of cash compared to a £1.577B outflow last year – not too sure what is going on there but it is having a big effect. National Grid also benefited this year from £365M received by selling a subsidiary.

All this leaves a negligible cash outflow of £43M for the year, £303M better than last year. However, when you consider that this was only achieved with the help of £553M movement in financial investment and £365M from the sale of a subsidiary, plus another £100M or so in new loans, this does not look quite so healthy under scrutiny. I find it hard to see going forward how this level of capital expenditure is sustainable in the long term. Cash flows are generally stable but in the US, timings of customer payments and changes in gas and electricity prices have an effect on the short term cashflow

Profitwise the split is £1.354B UK Transmission, £763M UK Gas Distribution, £1.19B US Regulated and £188M others. There is still twice as much profit generated from the UK operations than the US business. Profits were down on last year due to timing differences that benefited last year and two major storms in the US. National Grid generates value by investing in mainly regulated infrastructure. It plans to invest over £40B in their regulated networks before 2021. This investment is key to securing future profits as a lot of their rates are dependent on the amount of capital expenditure they invest. Ofgem published final proposals for the 2012/13 transmission price control and included real increases in revenues for electricity and gas transmission, reflecting the capital investment made over the period. This year, the capital investment program was largely driven by improvements to the UK electricity and gas networks.

In the US, cost savings of $200M were achieved through reorganisation and approval was granted to recover a portion of the recent storm costs in their Niagara Mohawk electricity business. It was announced that National Grid was not selected to continue to manage and operate Long Island’s electricity system beyond the end of 2013. New rate filings were also submitted for the network. In the UK, during the severe winter of 2010/11 some gas escapes occurred which resulted in a fine of £4.3M from Ofgem.

UK regulated revenues are linked to inflation so income is up but the group also have inflation linked debt so it is hedged. National Grid is not really affected by UK economic conditions otherwise. In the US it is different, as they supply to the end user so are exposed to risk relating to economic conditions and unemployment in particular.

In the UK, energy networks are regulated by Ofgem and they set the amount of revenue that can be earned from the regulated part of the business. This price includes enough revenue for the group to meet their licence obligations and earn a reasonable return on their investment. Within this there are financial incentives to Improve the effectiveness of the service, provide quality customer service and invest in the development in the network so as to ensure long term security of supply. Price controls in the UK exist for their electricity transmission operations (one for transmission ownership and another for system operator), the same for their gas transmission operations, and one for each of the four regional gas distribution networks. Also there are some price controls governing the LNG storage business and a cap imposed on the domestic metering service.

The transmission and gas distribution price controls expire at the end of March 2013. There was an extension for the transmission business that included a return of 4.75%. The prices are determined by taking into account an estimate for operating expenditure, capital expenditure, an allowance for depreciation and an allowed rate of return on capital invested, linked to the value of inflation. For the transmission businesses, the allowed return is 5.05%, for the gas distribution business it is 4.94%. Going forward, the pricing structure will change and is revenue will be calculated based on incentives for safety, reliability and customer service. The other change is that the price controls will cover 8 years as opposed to 5.

In the US, retail rates for energy are regulated by state commissions. Utility companies submit a rate filing to the governing bodies for a rate change in a litigated environment and can take up to a year for a final decision to be made. Companies need to prove that the rate change is reasonable but can implement the change before a final decision is made (customer refunds may be needed if the rate change is unsuccessful) and it is often the case that customer bodies will file objections to the increases. The rates are established based on the cost of providing the energy to the customers and includes operating expenses, depreciation, taxes and a fair return on components of the company’s regulated asset base so that it enables it to attract investors and maintain financial integrity. The final rate is often based on a test year to establish the costs involved.

National Grid have 5 US electricity rates and 7 US gas rates. As well as the above, some of the rates allow the group to keep some of the savings achieved through improving efficiency. If targets relating to service performance are not met, the group could be liable for some fines. National Grid is responsible for billing customers and bills include a commodity charge for the price of the gas, and charges covering the delivery service. A substantial amount of the costs are pass-through costs so they can be passed onto the customer (with no profit).

The generation plants in Long Island sell the electricity based on similar regulated rates which end in 2013 – negotiations are underway to set the rates for these plants after this date, however, National Grid have not been selected to run the island’s electricity system beyond this date.

Not including the effects of the US storms, the group were not involved in any reliability issues but they are being investigated over their response to both hurricane Irene and the US snow storms. The “Smart Grid” is being trialled in Massachusetts that will make capital investment more efficient, improve reliability and assist with storm restoration.

During the period, the group sold Seneca-Upshur, a gas generation and exploration business in the US and OnSteam, a metering business in the UK. They are attempting to sell Granite State Electric and Energy North in New Hampshire. They are thinking of expanding their Isle of Grain LNG storage business; looking for investors to develop carbon capture technology and are continuing with plans to develop an interconnector between the UK and Belgium in a joint venture with a Belgian transmission system – it is thought that it will enter commercial use by 2018.

There are a number of mechanisms that incentivise National Grid to provide a good service: transmission network reliability – if targets are achieved, National Grid gain an extra 1% of revenue. Failure could incur a penalty of up to 1.5%; day ahead gas demand forecast – If targets for the accuracy of the forecast in daily demand on their website, the group will earn and extra £8M. Penalties can be charged for innacurate forecasts; greenhouse gas emissions – Incentives are earned for below target greenhouse gas emissions. US plans don’t feature the same variety of incentives as the UK rates but they can earn or lose $4M depending on the reliability of the generation units.

In US, National Grid has moved to a more localised management structure after criticism in order to provide a local face to the business and to more effectively engage with the regulators and customers. This restructuring also seems to have saved some costs by reducing head count.

One example of how Carbon emissions are being reduced is the Grain Heat pipe. This is a joint venture between National Grid and Eon and is a hot water pipeline that transports surplus heat from the Eon power station to the LNG storage facility. This heat is used to convert the liquid gas to vapour to get it into the system. The cooled water is then returned to the power station where it cools the generators. Other capital expenditure projects include new power cables in London at a cost of about £900M and upgrading the old transmission network in New York state.

Over the year, there was a “small” increase in net debt of £866M! Net debt is expected to continue in line with capital investment. Next year should see inflationary revenue growth in UK and new rates from some US business. I find it interesting that the board should consider almost one billion of new debt to be small, but I guess that shows the kind of numbers we are dealing with here.

There has been a £1B JV with Scottish Power to build first subsea electricity link between England and Scotland announced during the period, I am not sure what material impact this will have other than showing that the group are investing in the network..

The UK transmission business recorded profits of £1.4B, up £61M on last year – this increase due to their new regulatory pricing formula, offset by some under recover timing issues and higher employment costs. The UK Gas Distribution business increased operating profit by £68M to £739M. Again, revenues increased due to the new pricing formula, and were held back slightly by depreciation and increased contractor costs to make sure they hit performance targets. In the US regulated business, profits fell by £550M to £1.154B. The main reasons for this fall were the lack of the over-recovery that occurred last year and the effect of tropical storm Irene and the snow storm, which affected profits by £116M. Other activities increased operating profit by £215M to £292M. There were a number of underlying reasons for this increase, there were environmental charges in the previous year that did not reoccur, there were some profitable property sales, the Grain LNG project benefited from the expansion in previous years and there were a number of new metering customer contracts.

The group achieved $200M in annualised cost savings in 2012 and filed new rate cases for their NY and Rhode Island gas and electricity business. The strategy going forward is to file new rate cases and undergo actions to improve efficiency by integrating new tools such as the new information systems. They are also working on their response to major weather events, which seem to be a major risk to the US business at the moment. Other risks include the outcome of the rate case filings and any findings by the audit being undertaken on behalf of NYPSC. Further environmental regulations may also increase costs in some areas.

So, if you’re still with me, what about National Grid as an investment proposition? UK revenues seem to be fine, but the reduction in US earnings is a worry, even though it is being put down to bad weather and bad timing. The figures we are dealing with here are staggering. There is a net debt of £19.6B, which is a huge amount of money and the interest payments alone would cripple most companies and the gearing here is over 200%! The cash flow is nominally negative, having benefited from a disposal but most of the cash goes on capital expenditure.

I did find the process of writing this rather tedious and the company in general bores me a bit – the LNG storage is an interesting sideline but the fact remains that most of the income generated by National Grid is regulated and the only way to improve profit is to find some efficiency savings or invest more in the network. The P/E ratio for what it’s worth is an undemanding 13.3 and the dividend return is 5.2%, which is better than any bank account that you might find. The one thing that concerns me slightly is the debt. The business model seems to be to increase net debt in line with capital expenditure – this surely isn’t sustainable in the long term, and I can envisage investors being tapped up for cash at some point. Tricky one this. I will continue to hold for the income but may sell if the shares rally through boredom.