There will be some changes to the business split going forward as ViiV Healthcare will be merged into the Global Pharmaceuticals segment, which is a bit of a shame in my view. The results this year include ten months of the vaccines and consumer healthcare joint venture with Novartis (and excluding the oncology assets sold to Novartis) GSK has now released its final/Q4 results for the year ended 2015.

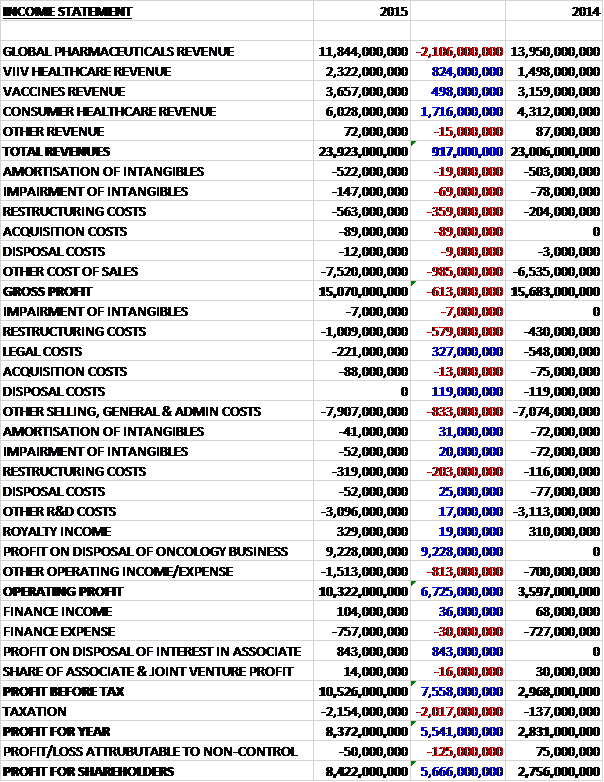

Overall revenues increased by £917M year on year as a £2.1BN decline in global pharmaceuticals revenue was more than offset by a £1.7BN growth in consumer healthcare revenue, an £824M increase in ViiV Healthcare revenue and a £498M growth in vaccines revenue. We then see a £69M increase in impairments, a £359M growth in restructuring costs and an £89M hike in acquisition costs along with a £985M increase in underlying cost of sales to give a gross profit some £613M below that of last year. There was also a £579M increase in admin restructuring costs, partially offset by a £327M decline in legal costs due to the Chinese fine levied last year, and the lack of any disposal costs which accounted for £119M last year.

The underlying increase in selling and admin costs was £833M, however. This was dwarfed by the £9.228BN profit on disposal of the oncology business to give an operating profit £6.725BN ahead of last year. We also see an £843M profit on the disposal of an interest in an associate relating to the disposal of half the investment in Aspen Pharmacare offset by a £2BN increase in tax to give a profit for the year of £8.422BN, an increase of £5.666BN year on year, although obviously without the £9.228BN profit on the disposal, the situation would have been very different.

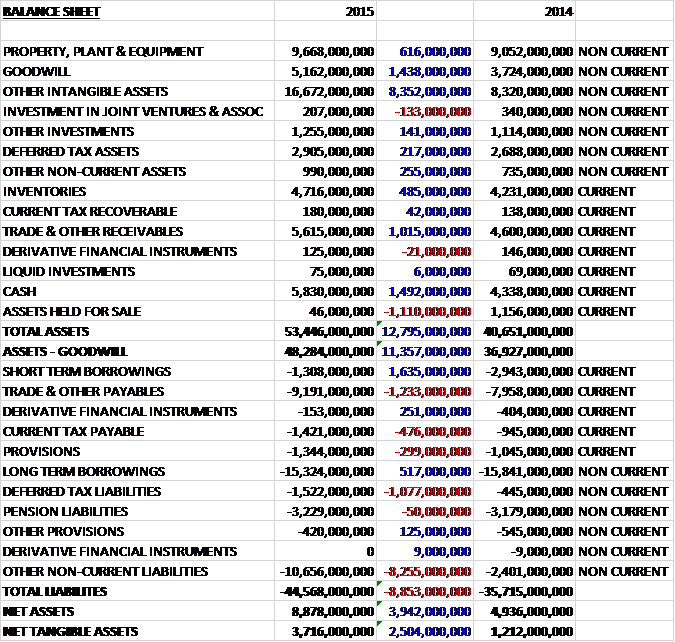

When compared to the end point of last year, total assets increased by £12.795BN driven by an £8.352BN growth in other intangible assets, a £1.438BN increase in goodwill, a £1.492BN growth in cash, a £1BN increase in receivables and a £616M growth in property, plant and equipment, partially offset by a £1.11BN fall in assets held for sale relating to the Oncology assets sold to Novartis. Total liabilities also increased during the year as an £8.255BN growth in other non-current liabilities including £6.287BN relating to the option for GSK to buy the remaining assets in the consumer healthcare joint venture from Novartis with the rest of the increase due to a growth in contingent consideration both to Novartis and Shionogi, a £1.233BN increase in payables and a £1BN growth in deferred tax liabilities due to the tax on consumer healthcare intangibles acquired from Novartis. These increases were partially offset by a £1.635BN decline in short-term borrowings and a £517M fall in long term borrowings. The end result is a net tangible asset level of £3.716BN, a growth of £2.5BN year on year.

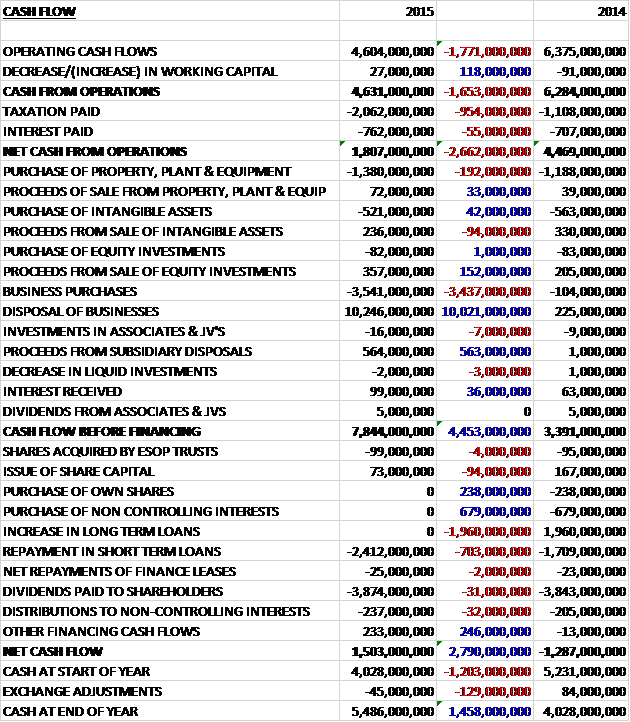

Before movements in working capital, cash profits declined by £1.771BN to £4.6BN. There was a very small decline in working capital but tax was up £954M relating to the tax paid on the Novartis transaction (£1.1BN) with the rest due to be settled in H1 2016, and interest paid grew by £55M to give a net cash from operations of £1.8BN, a decline of £2.66BN year on year. The group spent £1.38Bn on property, plant and equipment along with a net £285M spent on intangible assets but there was a net cash inflow of £275M related to equity investments (the rest of the Aspen Pharmacare investment I think) but the big move is from the net £7.269BN received from the disposal of businesses to give a cash inflow of £7.844BN before financing. The group then spent £2.412BN on repaying short term loans and spent £3.874B on dividends to give a cash flow for the year of £1.5BN and a cash level of £5.486BN at the year-end.

In Q4, pharmaceutical turnover was down 9% on a reported basis, primarily reflecting the disposal of the oncology business to Novartis. Adjusting for the impact of the disposal, turnover was down just 1% and HIV sales grew 51% in the quarter. Respiratory sales declined 3%, primarily reflecting further declines in Seretide in Europe and increased competitive pressures in the ROW region along with the continuing transition of the portfolio to newer products.

Sales of established products declined 20% with lower sales in all regions reflecting a continued decline in Lovaza in the US, intensifying pressure in Europe and the impact of the reshaping of the China business. Sales of new pharmaceutical products increased by £412M which more than offset the decline in Seretide.

The operating profit in Global Pharmaceuticals was £4.733BN, a decline of 24% year on year. In Q4, the operating profit was £1.149BN, a decline of 34% year on year with a 4.9% fall in operating margins on a pro-forma constant currency basis. This decline reflects the impact of lower prices and the cost of investments in manufacturing stability and additional capacity to support the new launches. Respiratory sales in Q4 declined by 3% to £1.594BN. Seretide/Advair sales were down 8% to £1.029BN, Flovent sales decreased 11% to £167M and Ventolin sales declined 16% to £147M. For the year, respiratory sales were down 7% with Seretide down 13%, Flovent decreasing by 12% and Ventolin falling 7%. Relvar/Breo Ellipta recorded sales of £99M and Anoro Ellipta, now launched in the US, Europe and Japan, recorded sales of £30M in Q4. During the year, the combined total of all Ellipta product sales was £353M with £139M of those in Q4.

In the final quarter in the US, respiratory sales increased 3% representing a 7% volume growth offset by a 4% negative impact of price and mix with sales of Advair up 2% although payer rebate adjustments related to prior quarters favourably impacted sales in during the period. Flovent sales were down 13% and Ventolin sales declined 26%, primarily as a result of the net negative effects of adjustments to payer rebates. The net impact of adjustments related to prior quarters for payer rebates across the respiratory portfolio was broadly neutral to reported US sales. The new Ellipta products recorded combined sales of £77M in the quarter.

European respiratory sales were down 11% to £341M with Seretide sales down 22% representing a 5% volume decline and a 7% negative impact of price and mix which reflected pressures of increased competition from generics and the transition of the portfolio to newer products. Relvar Ellipta recorded sales of £25M while Anoro Ellipta recorded sales of £6M. Respiratory sales in the International region declined 7% to £405M with emerging markets down 9% and Japan down 1%. In Emerging Markets, sales of Seretide were down 11% and Ventolin also declined 11%. In Japan, sales of Relvar Ellipta of £20M in the quarter drove overall respiratory performance.

In Q4, cardiovascular sales of £173M represented a decline of 30% year on year with the full year total of £858M representing a 9% fall. In Q4, the Avodart franchise fell 42% to £110M with 50% and 24% declines in sales of Avodart and Duaodart respectively driven by the onset of generic competition in the US and the interruption of third party supply in certain markets. Sales of Prolia were up 27% to £12M. In the year as a whole, immune-inflammation sales of £263M represented a 16% growth while in Q4 they increased 20% to £75M. Benlysta sales were £64M, up 27% and in the US, Benlysta sales were £59M, up 27%.

During the year, sales of other pharmaceuticals were down 4% to £2.199BN and in Q4 they were down 3% to £609M. Dermatology sales declined 11% to £104M, adversely affected by supply constraints, while Augmentin sales increased 1% to £129M. Sales of products for rare diseases declined 9% to £95M, including sales of Volibris which were up 5%.

During the year, sales of established products were down 15% to £2.528BN and in Q4 they were down 20% to £609M with sales in the US down 34% to £156M as Lovaza sales fell 62% to £22M. Europe was down 8% to £125M with Serevent sales down 18% to £9M. International was down 15% to £328M, with lower sales of Zeffix, down 25% to £27M driven by supply constraints in China, and Seroxat down 16% to £33M.

The operating profit in the ViiV Healthcare business was £1.686BN, a growth of 72% when compared to 2014. In Q4, the operating profit was £489M, a growth of 63% when compared to the final quarter of 2014. Sales during the year increased 54% to £2.322BN and sales in Q4 increased 51% to £695M with the US up 66%, Europe up 49%, and ROW markets up 9%. The growth in all regions was driven by Triumeq and Tivicay. The ongoing roll-out of both drugs resulted in sales of £289M in the case of Triumeq and £174M for Tivicay. Epzicom/Kivexa sales declined 19% to £162M and Selzentry sales declined 11% to £30M. There were continued declines in the mature portfolio, mainly driven by generic competition to both Combivir, down 47% to just £8M, and Lexiva, down 43% to £13M.

The operating profit in the Vaccines business was £966M, a fall of 9% year on year. In Q4, the operating profit was £164M, a fall of 23% year on year on margins that declined 8.9% on a constant currency basis, impacted be the inherited cost base of the former Novartis vaccines. Vaccine sales in the year were up 19% to £3.657BN and in Q4 they were up 20% to £963M with the US up 15%, Europe up 30% and ROW markets up 16%. Reported growth was driven by the newly acquired products, primarily Bexsero in Europe and Menveo in the US and Europe. Pro-forma performance was primarily driven by Europe due to strong growth in Bexsero with the US flat, primarily due to the phasing of Menveo and Fluarix sales; and ROW markets down, reflecting higher sales of the acquired vaccines in Q4 2014, and tougher competition for tenders as well as a number of supply constraints.

In the US, sales grew 15% on a reported basis and were flat pro-forma with performance driven by the favourable impact on Rotarix sales in the quarter of CDC stockpile movements in Q4 2014 and by increased Boostrix sales due to market share growth and increased wholesaler orders. These factors were offset by lower wholesale demand for Menveo and Fluarix sales due to the phasing of shipments. The Infanrix portfolio growth also was impacted by a strong comparative performance last year following supply shortages in Q3 2014.

In Europe, sales grew 30% on a reported basis and were up 11% pro-forma. This growth primarily reflected increased sales of the Meningitis portfolio. Bexsero growth came from gains in private market channels in several countries including Italy, Spain and Portugal, and in the UK following its inclusion in the NHS immunisation programme. Menveo growth was driven by tender awards in the UK and Italy and the MMRV portfolio was up 35%. Offsetting this growth, Infanrix was flat, impacted by supply constraints and increased competitor activity, and sales of Hep A vaccines declined reflecting ongoing supply constraints.

In ROW markets, sales grew 16% on a reported basis and were down 8% pro-forma. This performance reflected lower sales of Infanrix and Hep A vaccines due to supply constraints, partly offset by market expansion for Synflorix in Africa, Pakistan and Bangladesh, and the phasing of Boostrix sales in Brazil. Growth was also impacted by lower Cervarix demand and higher sales of the acquired vaccines in Q4 2014.

The operating profit in the Consumer Healthcare business was £680M, an increase of 66% when compared to last year. In Q4, the operating profit was £180M, an increase of 73% when compared to the same quarter of last year on core margins that increased 3.2% on a constant currency basis. Over the year, turnover grew 44% to £6.028BN and in Q4 2015, turnover grew 47% to £1.562BN, benefiting significantly from sales of the newly acquired products. On a pro-forma basis, growth was 5%, reflecting strong growth in the US following the launch of Flonase as well as globally strong growth in Sensodyne. Momentum from first half launches continued to drive innovation contribution with sales from product introductions in the last three years representing about 13% of sales.

US sales grew 50% on a reported basis and 13% on a pro-forma basis, with Flonase being the biggest growth contributor. Thereflu delivered double digit growth, driven by the launch of the warming syrups range earlier in the year, together with some price increases. Distribution gains contributed to the strong performance of Sensodyne Pronamel and the ongoing re-launches of Nicorette lozenge, Nicorette Minis and alli also contributed to the strong quarterly growth. This was partly offset by an adverse comparison on dental care, where re-supply boosted Q4 2014, as well as the continuing impact of supply constraints and increased competition on Tums.

Sales in Europe grew 75% on a reported basis and 2% pro-forma. This performance was driven by Voltaren which recorded market share gains in a number of markets, driven by a new advertising campaign and the Voltaren 12 hour topical innovation which has now launched in 35 markets. In Oral health, Sensodyne continued to report double digit growth due to new advertising in key markets and the rollout of Sensodyne True White in the UK, Sensodyne Repair and Protect Whitening in Germany and Sensodyne mouthwash across a number of markets. Paradontax delivered double digit growth in the period driven by a new condition awareness advertising campaign and consumer sampling. These strong performances were partly offset by denture care which reported an 11% decline due to an adverse comparison with Q4 last year which benefited from supply recovery. Overall, sales declined 6% in Central and Eastern Europe where continued softness in consumer spending was compounded by the low incidence of colds and flu.

ROW sales of £709M grew 32% on a reported basis and 3% pro-forma. This performance was driven by India which continued to perform well with Horlicks reporting growth of 18%, reflecting seasonal marketing campaigns which drove a record market share. Sensodyne delivered broad based growth of 19% across the region with Japan showing the benefits of the launch of Sensodyne Complete earlier in the year. Wellness sales continued to recover from earlier integration activities in many markets but were offset by economic and political uncertainty in Venezuela where sales were down 97%, and the weak consumer environment in Russia where sales were down 10% as a result of customers switching to value offerings as well as the adverse impact of the mild cold and flu season.

There were a number of new pharmaceutical and vaccine products that performed well, with Tivicay and Triumeq sales both up more than 100% in the year to £588M and £730M respectively. In respiratory, Relvar/Breo Ellipta was up over 100% to £257M and Anoro Ellipta also more than doubled to £79M. Incruse Ellipta also made some ground, also more than doubling to £14M with £9M of those sales being made in Q4. Elsewhere Eperzan/Tanzeum more than doubled to £41M in the year and in vaccines Bexsero also more than doubled to £115M although sales of Menveo fell during the year with a 50% collapse in Q4 taking the annual total for that product down to £160M.

During the year, Seretide/Advair remained by far the most important drug with sales falling 13% to £3.681BN but Trimeq became the second largest by sales as they more than doubled to £730M with Tivicay sales also up more than 100% to £588M. Next was Avodart, with sales down 15% to £657M and Flovent/Flixotide with sales down 12% to £623M and Ventolin down 7% to £620M. Other notable drugs were Benlysta, up 25% to £230M and Revlar/Breo Ellipta, more than doubling to £257M. Within vaccines, Infanrix remained the most important, although sales fell by 9% to £733M and Hepatitis vaccines fell 4% to £540M. Better performers were Rotarix, up 14% to £417M; Synflorix, up 5% to £381M; Boostrix, up 12% to £358M; and Fluarix, up 21% to £268M.

On a quarterly basis, again the most important drug remained Seretide, falling 8% to £1.029BN but once again it is pleasing to see Triumeq becoming the second highest by sales, more than doubling to £289M; with Tivicay next, increasing by 58% to £174M offsetting the 19% fall in Epzicom, down to £162M. Flixotide declined 11% to £167M and Ventolin was down 16% to £147M with Avodart collapsing, down 42% to £110M. Relvar/Breo Ellipta is really starting to contribute though, more than doubling to £99M and Benlysta also had a good quarter, up 27% to £64M. Anoro Ellipta is also starting to look promising, more than doubling to £30M. In vaccines, Infanrix was down 19% to £165M and Hepatitis vaccines were down 7% to £134M but there was a 13% growth in Synflorix sales to £136M, a 23% increase in Rotarix sales to £98M and a 61% increase in Boostrix sales to £91M.

There was some progress in the pipeline during the quarter. In HIV and Infectious diseases, the group announced that phase 2n LATTE study of long-acting, injectable formulations of cabotegravir and rilprivirine met its primary endpoint. In respiratory, the group announced FDA and EU approval for Nucala for severe eosinophilic asthma and 3008348 advanced to phase 1. In vaccines, they announced US filing to expand the age indication for FluLaval Quadrivalent, in immune-inflammation they announced positive results from the phase 3 BLISS-SC study of Benlysta administered subcutaneously in patients with systemic lupus erythematosus, positive top line results from the sirukumab phase 3 programme supporting regulatory filings for rheumatoid arthritis, and the initiation of a phase 3 study of sirukumab in Giant Cell Arteritis. In oncology, the announced the initiation of a phase 1 study to evaluate an OX40 agonist and they also announced EU approval for a variation to expand the indication of Volibris to include use in combination treatment of PAG along with the discontinued US Toctino programme.

Major restructuring charges during the year increased considerably, reflecting the acceleration of a number of integration projects following completion of the Novartis transaction, as well as further charges as part of the pharmaceuticals restructuring programme. The programme has delivered about £1Bn of incremental benefits this year, with a net impact on 2015 of £800M after taking into account the £219M structural credit recognised in Q3 2014. Charges for the combined restructuring and integration programme to date are £2.7BN and the total charges of the programme are expected to be about £5BN. By the end of this year, the programme has delivered about £1.6BN of annual savings and remains on track to deliver £3BN of annual savings in total and should be largely complete by the end of 2017.

Under the initial agreement, GSK had the right to withhold its consent to the exercise of either the Shionogi or Pfizer put options for their holdings in ViiV Healthcare so these were not included on the balance sheet. Following the good performance of the business, however, the board has decided that they should be recorded so they have given up their right to withhold consent and by the end of Q1 2016, the estimated present value of £2BN will be included in liabilities. Also, liabilities of £170M will be recognised for the future preferential dividends anticipated to become payable to Pfizer and Shionogi.

In December ViiV Healthcare had reached an agreement with Bristol-Myers Squibb to acquire its preclinical and discovery stage HIV research business. The consideration comprises an upfront payment of $33M followed by milestone payments of up to $587M and further contingent consideration depending on future sales performance. The acquisition is expected to complete during the first half of 2016. In a separate transaction, the group also agreed with Bristol-Myers Squibb to acquire its late stage HIV R&D assets. This consideration comprises an upfront payment of $317M, followed by milestones of up to $518M and tiered royalties on sales. This transaction is also expected to complete during the first half of 2016.

During the year the average sterling exchange rates were stronger against the Euro and the Yen but weaker against the US dollar which is the same situation that occurred in Q4. Due to the continuing political and economic uncertainties in Venezuela, at the year-end the group changed the exchange rate used to translate its subsidiaries in the country. This change had no significant impact on the income statement but gave rise to an exchange loss on translation of the cash held by the subsidiaries of £94M.

Going forward it is expected that the core effective tax rate will increase from 19.5% this year and last year to between 20% and 21% in 2016, mainly due to the higher proportion of sales expected from the US business and further moderate upward pressure on the tax rate is likely over the next several years too.

The group is apparently well positioned to return to core earnings growth in 2016 and the board now expect sales of new products to meet their target of £6BN in annual revenues up to two years earlier than previously stated which should now occur in 2018. In 2016, the board expect core EPS growth to reach double digit percentages on a constant currency basis but they are mindful that the macro-economic and healthcare environment will continue to be challenging. Over the next two years, they are expecting development milestones for Shingrix, sirukumab, ICS/LABA/LAMA, cabotegravir, daprodustat and their Men ABCWY vaccine. They also expect up to twenty Phase 2 starts for assets in Immuno-inflammation, Oncology, Respiratory and Infectious diseases. They also continue to expect to pay a dividend of 80p in 2016 and 2017.

At the end of the year the group had a net debt position of £10.727BN compared to £14.377BN at the end of last year. At the current share price the shares trade on a core PE of 16.7, although it has to be said I don’t really agree with the group not counting legal costs and amortisation as core items and if we add these back on, the PE becomes 19.6 which seems expensive to me. On next year’s consensus forecast, the shares trade on a PE of 16.6, although that probably discounts a load of costs too. After the payment of the 20p special dividend, the shares are currently yielding 7.1% which falls back down to 5.7% on the dividend going forward. These pay outs are definitely not covered by cash earnings, however, so care need to be taken.

So, this has been a difficult year for the group which has been characterised by their one blockbuster drug, Seretide, which is by far the biggest in sales, coming under competitive pressure. It is difficult to analyse profits as they are heavily influenced by the Novartis transaction and the company likes to take off all sort of costs in its calculations for core profits. Net assets did increase during the year, although the put option liabilities will be added next year so that should be taken into account. The operating cash flow was poor, falling year on year and not covering the dividend output, although the disposals meant that the group did get quite a bit of cash in during the year.

As well as Seretitde, Lovaza and Avodart both seem to be under pressure but the Ellipta drugs seem to be starting to make a meaningful contribution. The real saviours for the group at the moment, though, are the HIV drugs Triumeq and Tivicay with the former becoming the group’s second largest by sales. Given that it more than doubled this year, it would be very surprising if sales didn’t grow in 2016 too – I wonder just how important they can become for the group. It is a shame that the benefits have to be shared with the two partners in the associate really.

Overall, I do think there are some glimmers of hope here and the 5.7% forward dividend looks good, although as mentioned, this is no-where near close to being covered by operational cash flow or indeed earnings so the group needs the new drugs to come on stream quickly to maintain the dividend and prevent an outflow of cash. The forward PE of 16.6 does not look very exciting, particularly as it is likely based on GSK’s definition of core earnings which don’t include things like amortisation and legal fees – both of which seem pretty core to me – so I can’t help thinking that too much future growth is being assumed here and the shares look a bit pricey to me. Unless something changes in this regard, I will not be updating the company going forward.