Redrow has now released its interim results for the year ending 2016.

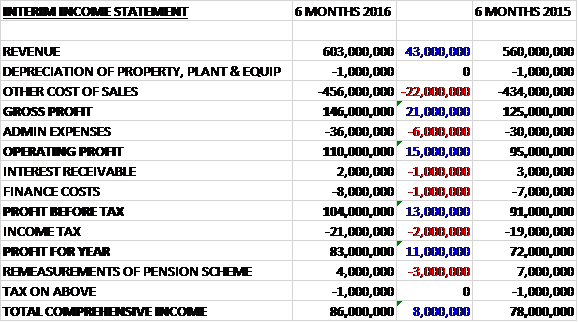

Revenues grew by £43M when compared to the first half of last year and with cost of sales up by just £22M, the gross profit increased by £21M. Admin expenses were £6M higher and there was a small reduction in interest receivable along with a modest growth in finance costs and tax which meant that the profit for the half year period came in at £83M, a growth of £11M year on year.

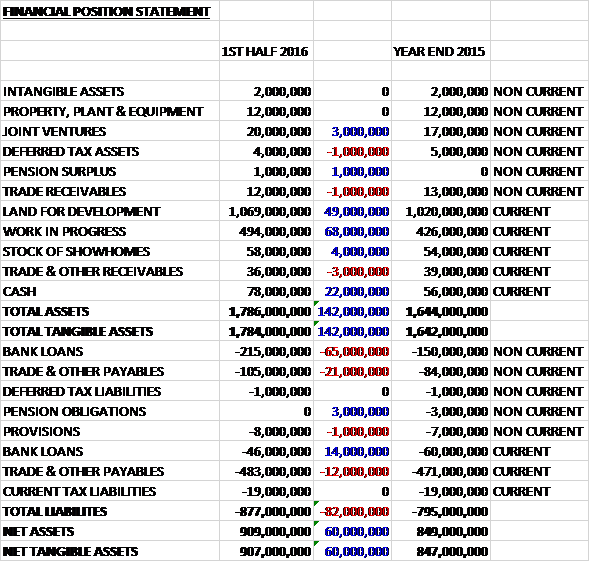

When compared to the end point of last year, total assets increased by £142M driven by a £68M growth in work in progress, a £49M increase in land for development and a £22M growth in cash. Total liabilities also increased during the period due to a £51M increase in bank loans and a £33M growth in payables. The end result is a net tangible asset level of £907M, an increase of £60M over the past six month period.

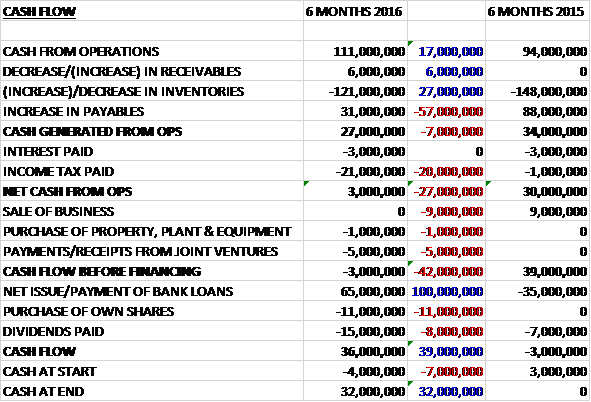

Before movements in working capital, cash profits increased by £17M to £111M. There was a large cash outflow through working capital, however, with a £121M growth in inventories along with a £31M increase in payables that was some £57M lower than last time. The income tax paid was also £20M above that of the first half of 2015 which meant that there was a net cash inflow of just £3M from operations, a deterioration of £27M year on year. The group spent just £1M on property, plant and equipment and £5M on their joint venture investments to give a cash outflow of £3M before financing. They then took out a net £65M in new loans to pay for the £15M of dividends and £11M of their own shares, presumably to pay out in incentive schemes which meant that there was a cash inflow of £36M for the half year period and a cash level of £32M at the end of the half.

During the first half of the year the group increased their legal completions by 18% to 2,178. Homes revenue in the period increased by 14% to £584M due to the increased number of completions and total revenues increased by 8% to £603M, impacted by revenues from commercial and land sales being £27M lower. The average selling price of their private homes increased 2% due to the shift of their London business away from high priced Central London apartments to concentrate on the Outer London commuter market where demand remains strong. Overheads increased by £6M due to the opening of two new divisions, one covering Kent and Sussex and the other to manage what will be the flagship development at Colindale in North London.

Demand for new homes was strong throughout the period and the Government’s Help to Buy scheme continues to give the board confidence to increase output. The only area where a slow-down has been seen is in Central London, but this had a limited effect on the group as they previously made the decision to re-focus their London business on Outer London where demand remains robust. In the period, some 44% of the private legal completions used the Help to Buy scheme and mortgage availability and rates continue to improve. As a result the group’s sales per outlet per week were 0.65, up 10% on the prior year. The value of private reservations in the first half increased by 51% to £679M which resulted in a closing order book of £655M, up 51% year on year.

During the period the group added over 5,700 plots to their current land bank, of which over 1,500 were converted from their forward land bank. These included 920 plots on their major Garden Village project in Cheshire. At the end of December the current land bank totalled 21,435 plots, an 18% increase compared to the end of last year and since the end of the period the group have obtained a fully implementable planning consent on the Colindale site, converting another 2,900 plots from forward to current land which has caused the forward land bank to reduce slightly. There were also some small land sales both in Harrow Estates and in the homes business as the group completed on some freehold reversion sales.

One consequence of selling faster is that sites are coming to an end quicker yet bringing new outlets on stream continues to be delayed by the planning system. About 42% of the current land bank is tied up at one stage or another. The shortage of skilled people also continues to be a constraint on output but this situation has eased over the past six months.

The group are only at the beginning of the spring selling season, but demand for new homes remains robust. They ended the first half with an order book up 51% on this time last year and in the first six weeks of the second half they have secured 455 private reservations, 10% ahead of last year. They have a strong pipeline of new sites in planning and the strategy to grow the business and increase the number of homes they build remains on track. Demand for new homes remains robust despite recent turmoil in the financial markets and the board are confident of another strong year of growth for the group.

At the period-end, the group had a net debt position of £183M compared to £154M at the end point of last year. After a doubling of the interim dividend, the shares trade on a yield of 1.9% which increases to 2.3% on the full year guidance of 10p per share for the year.

Overall then, this was another period of good progress for the group. Profits were up and net assets increased. The operating cash flow did decline year on year, however, mainly as a result of higher taxes paid but a smaller increase in payables also had an effect and there was no free cash generated during the period. The cash profits did increase, however. Overall, completions were up and the sale of homes was very strong with the more modest growth in revenues due to lower commercial and land sales. The average selling price only increased by 2% due to a shift in focus away from Central London where demand has slowed.

The closing order book is up an impressive 51% and demand for homes apparently remain robust despite the current economic turmoil. Despite a bit increase in the dividend, the shares still only yield 2.3% but considering the performance here I am tempted to make a purchase.

On the 10th February it was announced that non-executive director Sir Michael Lyons had purchased 3,000 shares at a value of £12K. This represents his maiden purchase.

On the 28th June the group released a statement for trading in 2016 which will be a pre-tax profit above current market estimates (£240M). In the run up to the EU referendum there was no impact on house sales or visitor levels. Although it is too early to tell if Brexit will have an effect on future sales, initial feedback is that sites remain busy, reservations continue to be taken and there were strong reservations at the new sites launches last week.

The value of private reservations was up 46% at £1.56BN, driven by strong regional growth. The private order book at the end of June is £807M, up over 50% year on year and the number of active outlets at the year-end increased by 11 to 128 in line with previous guidance.

In Central London the developments at Commercial Street and Amberley Waterfront are now completed and significant progress has been made at Holland Park Avenue and Connaught Place where just a handful of plots remain. All other London developments, including the Croydon joint venture, have sold either in line with or exceeding management expectations. At Colindale, in just a few months the order book has reached £116M, including a 211 unit sale to L&Q.

Turnover for the year increased by 20% to £1.38BN. The number of homes legally completed increased by 17% to 4,716, with private completions increasing by 12% 3,882 and the average selling price of private homes increasing by £31.2K to £328.5K. The closing net debt position was £139M, a 10% reduction on 2015.

This all sounds good to me – the huge cloud hanging over this statement is the uncertainty over Brexit and the effect on housebuilding – the latest construction PMIs are terrible. I will therefore hold fire for now I think.

On the 1st July the group announced some director purchase. Non-executive director Nick Hewson purchased 1,500 shares at a value of £5K and non-executive director Debbie Hewitt purchased 9,082 shares at a value of £30K. Nick now owns 20,500 shares and Debbie owns 30,687.