Spectris has now released its final results for the year ended 2015.

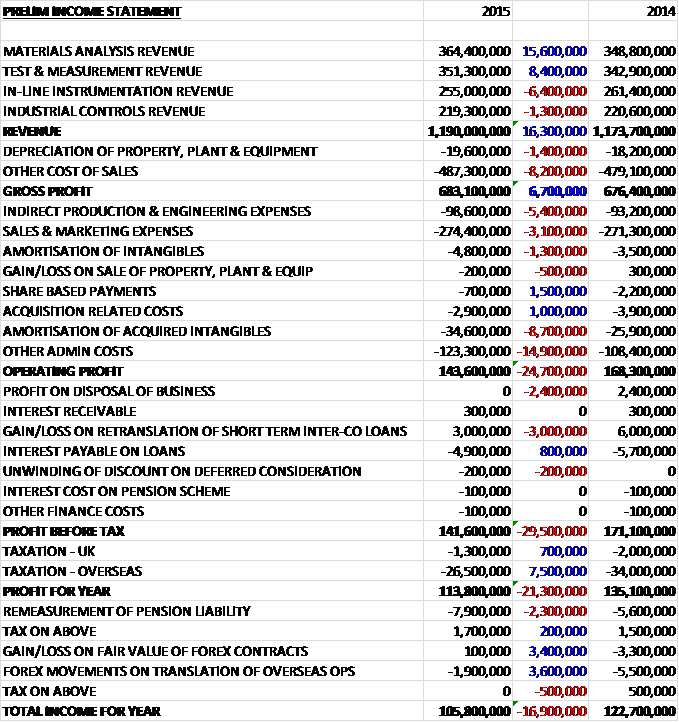

Revenues increased when compared to last year, although on a like for like basis they were flat as a £15.6M growth in Materials Analysis revenue and an £8.4M increase in Test & Measurement revenue was partially offset by a £6.4M decline in In-line Instrumentation revenue and a £1.3M fall in Industrial Controls revenue. Depreciation was up £1.4M and other cost of sales grew by £8.2M to give a gross profit £6.7M above that of last year. Indirect production and engineering expenses were up £5.4M, sales and marketing costs grew by £3.1M and amortisation of intangibles were up £1.3M but share based payments fell by £1.5M and acquisition related costs were down £1M before an £8.7M growth in the amortisation of acquired intangibles and a £14.9M increase in other admin costs gave an operating profit £24.7M below that of 2014. We then see the lack of £2.4M-worth of business disposal profits and a £3M decline in the gain from short-term internal company loan retranslations partially offset by an £800K decline in loan interest after the group renegotiated their bank loans during the year at lower interest rates before an £8.2M fall in tax, helped by increased R&D tax incentives and a higher tax credit on the amortisation of intangibles, meant that the profit for the year came in at £113.8M, a decline of £21.3M year on year.

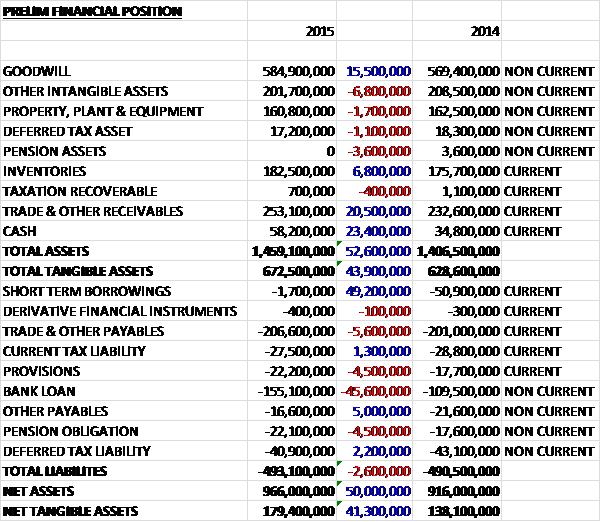

When compared to the end point of last year, total assets increased by £52.6M driven by a £23.4M growth in cash, a £20.5M increase in receivables, a £15.5M growth in goodwill and a £6.8M increase in inventories, partially offset by a £6.8M decline in other intangible assets, a £3.6M eradication of pension assets as investment returns were lower than expected and a £1.7M fall in property, plant and equipment. Total liabilities also increased during the year as a £5.6M growth in payables, a £4.5M increase in pension obligations and a £4.5M growth in provisions were partially offset by a £3.6M decline in borrowings, a £5M fall in other payables and a £2.2M decrease in deferred tax liabilities. The end result is a net tangible asset level of £179.4M, a growth of £41.3M year on year.

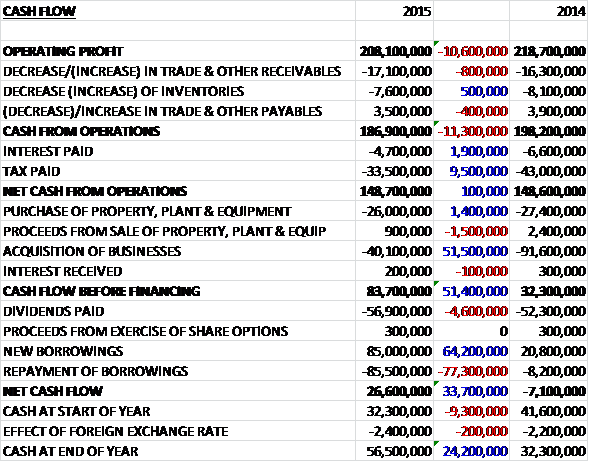

Before movements in working capital, cash profits declined by £10.6M to £208.1M. There was an outflow of cash through working capital, in particular and increase in receivables but interest payments fell by £1.9M and tax payments declined by £9.5M to give a net cash from operations of £148.7M, which was flat year on year. The group spent a net £25.1M on property, plant and equipment along with £40.1M on new business acquisitions to give a free cash flow of £83.7M which easily covered the £56.9M in dividend payments to leave a cash flow of £26.6M for the year and a cash level of £56.5M at the year-end.

Overall the year was characterised by mixed trading conditions, with growth in Europe and Asia offset by a challenging environment in North America and the rest of the world. North America experienced a broad-based deterioration in industrial production which particularly impacted sales growth in the industrial controls segment. This weakness accelerated as the year progressed and was especially pronounced in the oil and gas related sectors. Sales to the rest of the world also declined, primarily due to low demand in Russia, reflecting a weak economy and the imposition of certain technology sanctions in mid-2014.

As well as the subdued sales, the profit was affected by increased investment in R&D programmes and overhead cost inflation. Given the trading conditions, the group has initiated a number of cost reduction measures including selective restructuring in certain businesses. The combined effect of a reduction in restructuring charges and incremental benefits arising from that activity, is anticipated to result in a net increase in operating profit of about £10M. The acquisitions contributed £5.2M to operating profit but foreign currency movements had an adverse impact of £4.8M.

The operating profit in the Materials Analysis business was £53.7M, a growth of 1% although on a like for like basis, the profit declined by 2% reflecting the annualised effect of prior year headcount increases, the cost of restructuring and the absence of a £3M one-off R&D related government grant which benefited last year. Reported sales increased 4%, including a four percentage point contribution from acquisitions and a three percentage point adverse impact from currency movements which meant that like for like sales growth was 3%, driven by North America and Europe as sales to the rest of the world declined.

Sales to the pharmaceuticals and fine chemicals sector increased, driven by strong demand from biopharmaceutical and generic drug manufacturers. Sales also benefited from good progress by the particle measuring business together with their investments in solutions focussed on the life science industry, such as a biophysical characterisation tool, the Viscosizer, and a next generation calorimeter, the MicroCal PEAQ-ITC. Regulatory compliance, having previously been a strong growth driver for the operations in China, is now also a positive driver of growth in India, where the generic drug manufacturers are focused on achieving the standards necessary to export their drugs to the US. Elsewhere there was good sales growth in the major developed markets of North America and Europe.

Following weak demand from the metals, minerals and mining industries last year, there was a resumption of sales growth this year. There was good sales growth from North America, China, India and Brazil but sales declined in Australia, Germany and Japan. Generally sales growth in the mining sector came from aftermarket sales, with customers preferring to repair and support existing equipment rather than invest in new products. In the metals and minerals sectors, however, sales of new instruments were strong. Whilst managing the cost base to align it to the lower demand levels, the group have continued to develop new products and this year they launched a major new product family, the Zetium x-ray spectrometer, sales of which have been encouraging so far.

Sales to academic research institutes declined, with pressure on public finances and low levels of private funding from industries such as mining continuing to adversely impact trading conditions for the businesses. Among the major markets, only Germany and Japan delivered sales growth in this sector and there was a significant decline in China following what had been a strong year in 2014 when the Chinese state universities invested in projects related to water quality and energy storage.

Sales to the semiconductor industry grew strongly, benefiting from the group’s innovation as they launched the first particle liquid counter which can measure contaminants as small as 20 nanometres, and from the strong relationships they have with the leading semiconductor manufacturers in North America and Asia which have been enhanced with the acquisition of their distributers in South Korea and Taiwan where they are now directly serving the manufacturers.

The board expect the division to show further progress in 2016. Continued investment in new products should deliver progress in the pharmaceuticals, life science and semiconductors sectors. Investment by the mining sector is expected to remain low, with growth coming from aftermarket sales, although the metals and minerals sectors are expected to remain robust. It is expected that these factors will more than offset a subdued academic research market given public sector budget constraints and the cost reduction measures taken during the second half of this year are expected to improve future profitability.

The operating profit in the Test and Measurement division was £55.3M, a growth of 6% year on year with a 9% like for like change, primarily reflecting positive sales mix and the benefit of restructuring measures undertaken during the year. Reported sales increased 2%, including a six percentage point contribution from acquisitions and a five percentage point adverse currency movement. There was like for like sales growth in Europe and China with falls in other Asian markets.

Underlying demand from the automotive sector remains healthy. Whilst direct sales to this sector were broadly unchanged this year, due to the lack of large projects in North America which had benefited the prior year, there was strong sales growth to machine manufacturers, a significant proportion of which represented sales into the automotive supply chain. Automotive customers are increasingly demanding the provision of an integrated solution, combining hardware, software and services. For example, they won a significant contract with a major UK-based automotive manufacturer to provide not only hardware but also a broad range of services including calibration, on-site maintenance, spare part supply, training and dedicated hotline support and European on-site support.

In January the group acquired ReliaSoft, a US-based reliability engineering software and services business which has strengthened and extended their software applications offering. During the year they made good progress with their NVH simulator, winning important contracts with major automotive manufacturers in the US, UK and Europe, and they are expecting their noise, vibration and harshness offering to include engineering services with the acquisition in November of Sound Answers, a US-based provider of NVH consulting expertise. The business has been a strategic partner for nine years and they will now be able to offer their customers new capabilities such as troubleshooting and product development services.

Underlying demand from the aerospace sector remains robust but sales in this sector decreased during the year reflecting the adverse impact that economic sanctions on Russia had on their sales of satellite vibration test systems to this country, together with fewer large orders in the US. Aerospace companies continue to invest in the use of advanced composite materials to develop more fuel efficient aircraft, and the group are one of the few key suppliers capable of meeting their requirements to test and verify the key characteristics of these new materials. During the year they secured important orders from a major US aerospace company for data acquisition systems to stress test the Orion spacecraft and PULSE software analysers to test sound and vibration in its satellite systems.

Sales of the environmental noise monitoring services grew, benefiting from good demand in Europe. They won a major contract with the Italian government for noise monitoring in its vehicle inspection centres and extended their relationship with Aena, the Spanish airports operator to centralise the group’s systems across the six airports they already serve and extend their coverage to new sites. As was the case in Materials Analysis, and reflecting pressure on public finances, the division’s sales to academic research institutes declined. Amongst their major markets, only Germany delivered sales growth in this sector, whilst there was a significant decline in sales to China.

Sales to telecoms customers declined in the year following strong growth last year. The group see good opportunities in this market to provide additional services such as in test-rig design and calibration, thereby improving the resilience of revenues in this sector where sales patterns are lumpy.

Whilst the weakness in the oil and gas and mining markets this year led to reduced demand for the group’s microseismic monitoring solutions, they made good progress developing and extending their offering to these industries. As well as continuing to win key contracts against larger competitors, they have begun to expand their international presence outside North America, establishing offices in the Middle East and Mexico. In October the group acquired Spectraseis, a US-based leader in surface based microseismic monitoring technology which is complementary to the existing offering.

Over the coming year, the board expect conditions in the automotive and aerospace sectors to benefit from further growth in engineering software applications, together with improving demand from the telecoms market and a good contribution from acquisitions. The academic research market is expected to remain subdued and market conditions in the oil and gas and mining industries are expected to remain challenging, although there are good prospects for the increased adoption of microseismic monitoring solutions in the coming years as customers seek to make better use of data analytics to improve productivity.

The operating profit in the In-line Instrumentation division was £36.8M, a decline of 23% year on year with a 19% like for like fall reflecting falling sales and an adverse product mix. Reported sales decreased 2%, reflecting an adverse impact of 1% from forex movements and a like for like sales decline of 1%. Geographically, North American sales were broadly flat while sales to Asia and Europe were marginally lower.

In the pulp and paper market, growth improved progressively throughout the year with a good second half performance more than compensating for the sales decline in the first half. Growth in sales to the tissue and pulp segments reflected continuing positive trends in those markets as well as some success in offering customers new products incorporating high-performance creping blades and other instrumentation, such as the new control sensors for pulp mill automation. This growth was partially offset by lower sales into the graphic paper segment. While excess capacity in China in particular, continued to limit growth opportunities in this segment, there has been a positive market reaction to the new advanced material coating blades which drove higher sales into the segment in the second half.

In the energy and utilities market, the group achieved modest sales growth, with a strong growth in sales to the wind energy market being partially offset by a modest fall in sales to the downstream petrochemicals industry. In the wind energy market they continue to see favourable global trends, which contributed to good sales growth across all regions and in addition to an increase in sales to existing customers, they also managed to broaden their customer base with a number of significant contract wins from wind farm operators. They are in the process of strengthening their sales and marketing organisation, including the expansion of their regional office network, and they have increased their focus on the provision of innovative solutions to customers with an example being a solution that combines hardware and software to enable customers to view all information from any machine protection system in their plant on one diagnostic system. Since its launch in the middle of this year, this product has been positively received by customers.

Sales to the downstream petrochemicals industry fell modestly over the year after showing good growth in the first half of the year. This reflects the slowdown in the sector, which has resulted in falling investment levels and fewer large projects being progressed. The group launched a major new product platform in the industrial gases market, a laser gas analyser called the MiniLaser, which is more powerful, smaller and lighter than other products in the market, resulting in significantly easier and lower-cost installation for customers. During the year they launched important applications of the MiniLaser for the petrochemicals, combustion and power markets and customer reaction to date has been positive.

Sales to the web and converting industries declined significantly during the year, mainly due to a lack of large projects in North America and Asia. Whilst these industries have recently been experiencing cyclical softness, the group continue to see growth opportunities. They made good progress developing new systems that extend their offering for these industries such as the Slim TraK single beam scanner, a compact scanner for narrow web converting processes that is targeted at paper and plastic film converting applications. Following the creation in 2014 of NDC Technologies, the group have now aligned the combined sales forces of the previous businesses around single industry verticals in order to give them more effective coverage.

Going forward, the board are encouraged by the improved performance of the pulp and paper business in the second half of the year but growth from the energy and utilities sector is expected to be modest next year. Underlying market conditions in the renewable energy sector remain healthy and the new products for this market have been well received but the slowdown in the oil and gas sector that impacted sales to the petrochemicals industry in the latter part of 2015 is expected to continue into 2016. In the web and converting industries, they expect to see some modest growth after a weak year in 2015, together with modest benefits from the new product launches and the creation of single sales teams to service key industries.

In Industrial Controls, the operating profit declined by 21% on a reported basis and 27% on a like for like basis reflecting the impact of reduced sales, adverse sales mix and restructuring costs along with additional costs at Omega which were required to maintain service levels during the launch of a new ERP system. Reported sales decreased 1% including a one percentage point contribution from acquisitions and a positive impact of five percentage points from foreign currency movements which meant that like for like sales decreased 7%.

With over 70% of the segment’s sales being customers in North America, the key driver behind the sales decline was significant weakness in US industrial production, particularly in the second half of the year. The oil and gas sector particularly suffered and this was felt most acutely in the group’s industrial networking business following strong sales in 2014. In Asia they saw continued good progress on the development of their process measurement and control business and in Europe they saw a mixed performance with a challenging year for the industrial networking business being partially offset by growth in sales of process measurement and control products and automatic identification and machine vision solutions.

Omega continued to invest in its digital marketing capabilities, installed a common ERP system across the majority of its business and delivered good growth from its operations established in recent years in Asia, Latin America and Europe. The industrial internet of things is one of the key strategic markets and during the year the group established an innovation centre for the market in the US with a focussed engineering, product and sales team dedicated to the area.

In August the group acquired Label Vision Systems, a US-based business whose technology enables companies to comply with new US legislation on product identification marking to improve traceability throughout the supply chain. The business is performing well and its integration into Microscan is proceeding to plan.

The year also saw a number of key product launches and developments. In September, the machine vision business launched the Micro Hawk, a modular and scalable industrial barcode imager and smart camera platform. They also enhanced their series of industrial cellular routers through the addition of functionality to provide automatic alerts to operatives, and launched a major new series of temperature and process controllers targeted at customers in the laboratory and in the factory automation and chemical industries.

Going forward, given the significant exposure to the US, sales progress in 2016 will be largely dependent on the recovery of the industrial markets there. The board expect contributions from recent product launches, the acquisition of Label Vision Systems and the investments made in Omega to improve future profitability. In the medium term, the need for customers to improve productivity is expected to result in increased demand for factory automation and industrial networking products, particularly in China and Mexico.

There were a large number of acquisition during the year. In January the group acquired ReliaSoft, a company based in the US for a total consideration of £28.3M with the transaction generating goodwill of £17M. The business is a provider of engineering software, education, consulting and related services to product manufacturers and maintenance organisations around the world and is being integrated into the Test and Measurement segment. In March they acquired Sunway Scientific, a Taiwanese distributor, for a total consideration of £2.2M, including £400K of contingent consideration. This transaction generated goodwill of £900K and the business is being integrated into the Materials Analysis segment.

In August the group acquired Label Vision Systems, a US business, for a total consideration of £4.5M including £1.6M of contingent consideration. The transaction generated goodwill of £2.6M and the business is being integrated into the Industrial Controls segment. In October they acquired 96% of the share capital of Spectraseis, a company based in Switzerland which operates in the US and Canada, for a total consideration of £5M, including £100K of contingent consideration. This acquisition extends the group’s capabilities in surface-based microseismic sensing equipment for hydraulic fracturing monitoring and induced seismicity monitoring and generated goodwill of £2.1M. The business is being integrated into the Test and Measurement segment and the remaining 4% of the share capital is currently in the process of being purchased.

In November the group acquired Sound Answers, a company based in the US, for a total consideration of £2.3M including £900K of contingent consideration. The transaction generated goodwill of £1.4M and the business is a provider of engineering services that specialise in noise, vibration and harshness design and simulation, primarily for the automotive market and the business is being integrated into the Test and Measurement sector. All of these acquisitions contributed an operating profit of £2.5M to the group in the period since their purchase.

Lisa Davis will retire as a non-executive director following the AGM after her promotion to the Siemens managing board last year. She was in the role for two years.

Going forward, the group are on track with the restructuring measures and the benefit of these will help them better align cost growth with sales growth next year. New product launches and acquisitions are expected to continue to play an important role in the group’s development and these investments, together with the broad end market exposure provide the board with confidence that the company is well positioned for 2016.

The group is well covered with borrowings with some £371.1M undrawn facilities available. The net debt position at the year-end was £98.6M compared to £125.6M at the end point of last year. At the current share price the shares are trading on a fairly hefty PE ratio of 18.2 which falls to 15 on next year’s consensus forecast. After a 6% increase in the dividend the shares are now yielding 2.9% which increases to 3% on next year’s forecast.

Overall then this has been a bit of a mixed year for the group. Profits fell, not helped by a big increase in the amortisation of acquired intangibles; but net assets showed an impressive growth. The operating cash flow was flat but this was due to a big fall in tax along with a decline in interest payments following better terms agreed with the lenders, and cash profits declined. The group still generated an impressive level of free cash, however.

Operationally the best performing division was Test & Measurement which saw increased like for like profits but this due to a positive sales mix and prior cost-cutting rather than growth in their markets as the noise monitoring products did well but most of the other areas suffered. There was a decent performance in the Materials Analysis division was the modest decline in like for like profits was due to the lack of an R&D grant that occurred last year and the costs of restructuring, with sales actually up due to a strong performance in the semiconductor, pharmaceuticals and metals & mining markets, partially offset by weakness in academic research.

Profits declined considerably in the In-line Instrumentation division manly due to adverse product mix and lower sales as a good performance in pulp and paper along with a strong showing in the wind power generation market was more than offset by weakness in the downstream petrochemicals industry and the web and converting industry. The performance at Industrial Controls was poor due to reduced sales, an adverse product mix and restructuring costs. The division suffered weakness in the US industrial production market which actually worsened as the year progressed.

Going forward the board see profitability increasing in the materials analysis division but the outlook in Test & Measurement along with In-line Instrumentation is much more mixed whilst the outlook for the Industrial Controls business is dependent on US industrial production which is currently undergoing weakness. Whilst this remains a quality, cash generative company, the forward PE of 15 and dividend yield of 3% seems a bit expensive to me given the uncertainties over the performance next year so I will continue to keep a watching brief.

On the 23rd February the group announced the acquisition of privately owned CAS Clean Air Service. The business was established in Switzerland and is a cleanroom services company, providing measurement services, process qualification, calibration services and product sales primarily to the pharmaceuticals manufacturing market. The business generates annual revenue of about £7.2M and will be integrated into the Materials Analysis segment. There are no details of how much they paid for the acquisition.

On the 4th March, the spouse of non-executive director Ulf Quellmann purchased 500 shares at a value of just over £9K which gives Ulf a holding of 1,500. Although nice to see, this really isn’t a particularly material amount.

On the 20th May the group released a trading update covering the first four months of the year. Reported sales increased by 2% which all came from acquisitions. Favourable forex movements also positively impacted growth by 4% which meant that like for like sales were down 4%. Regionally like for like sales grew by 2% in Asia Pacific whilst sales to North America, Europe and the ROW declined by 4%, 8% and 11% respectively.

During the period the group completed the acquisition of Clean Air Service, a cleanroom services company which provides measurement services, process qualification, calibration services and product sales to the pharmaceutical and life science sector.

Trading conditions in the period continued to be challenging and the group are focused on implementing their restructuring programmes. The benefits of these will enable them to better align their cost and sales bases. Whilst there is limited visibility on trading, the outlook for 2016 remains unchanged. Nonetheless, this decline in sales is a concern and I am not rushing to jump in here.

On the 20th June the group announced the acquisition of US company Capstone Technology for a consideration of $22.5M. The business is a provider of software solutions for process control optimisation and decision support, serving multiple process industries such as pulp & paper, chemicals, utilities, oil & gas and food & beverage. It comprises two software platforms: the MACS software suite provides engineering services and software for advanced process control optimisation while data PARC is a data historian, visualisation and analytics software suite for operational decision support. The business will be integrated into the group’s in-line instrumentation segment.