Amino Technologies has now released its final results for the year ended 2015.

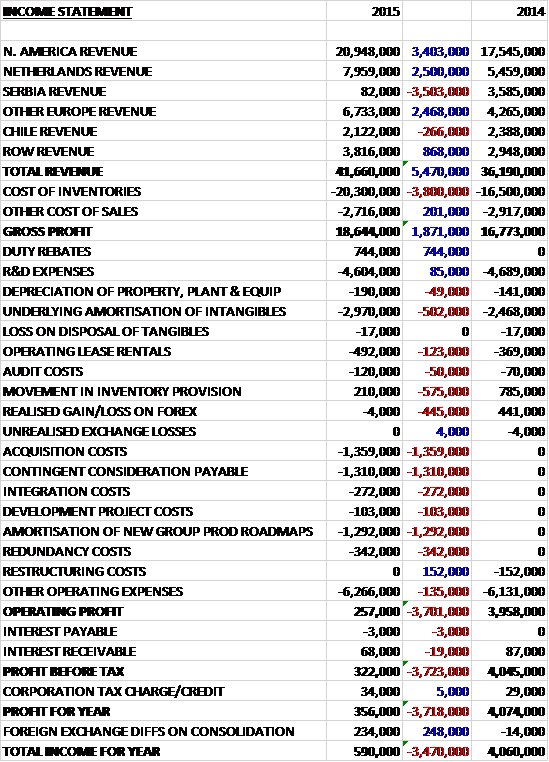

Revenues increased when compared to last year as a result of the acquisitions as a £3.5M crash in Serbian revenue and a £266K decline in Chile revenue was more than offset by a £3.4M growth in North American revenue, a £2.5M increase in Netherlands revenue, a £2.5M growth in other European revenue and an £868K increase in ROW revenue. Cost of inventories also increased, but to a lesser degree, to give a gross profit some £1.9M ahead of 2014. The amortisation of underlying intangibles increased by £502K, operating leases were up £123K, there was a £575K reduction in the positive movement in the inventory provision and a £445K negative swing on the realised loss of foreign exchange along with a £135K growth in other “underlying” operating costs.

There were also a number of non-underlying costs and income which included a £744K duty rebate, £1.4M in acquisition costs with a further £1.3M in contingent consideration, £272K of integration costs, £342K of redundancy costs and a £1.3M amortisation of the new group product roadmaps following rationalisation after the acquisition. The upshot of all this is an operating profit that fell by £3.7M. There were negligible changes in finance costs and tax so the profit for the year came at £356K, a decline of £3.7M year on year, although without all of the acquisition related costs, the profit would have grown by £113K to £4.2M, but given at the half year stage the profit was £1.9M up at £2.9M (excluding the duty rebate), this performance is not all that impressive!

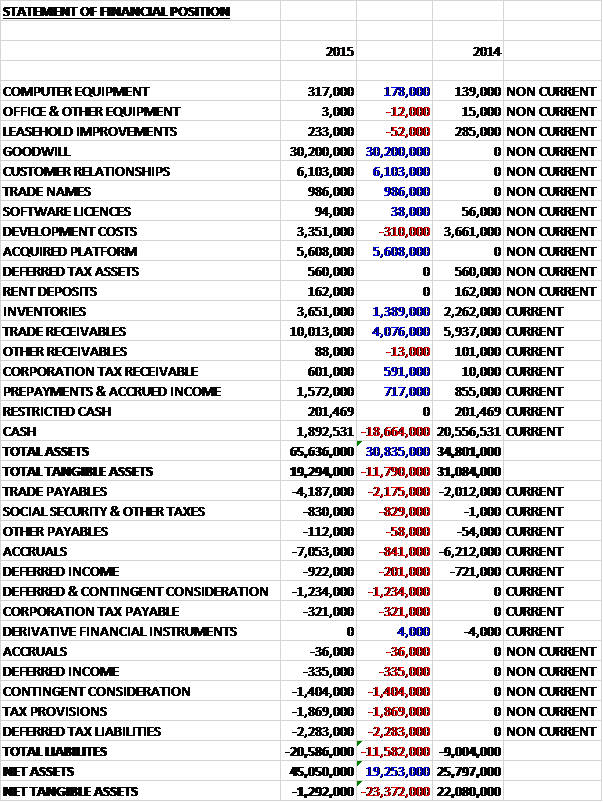

When compared to the end point of last year, total assets increased by £30.8M driven by a £30.2M growth in goodwill, a £6.1M increase in customer relationships, a £5.6M growth in “acquired platforms”, a £4.1M increase in trade receivables and a £1.4M growth in inventories, partially offset by an £18.7M fall in cash levels. Total liabilities also increased during the year due to a £2.3M growth in deferred tax liabilities relating to the temporary differences following the acquisition, a £2.2M increase in trade payables, a £1.9M increase in tax provisions, and a £2.6M growth in continent consideration. The end result is a net tangible asset level of -£1.3M, a deterioration of £23.4M year on year.

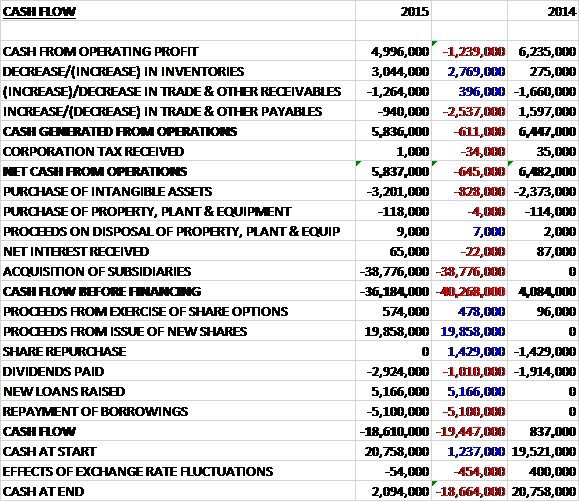

Before movements in working capital, cash profits declined by £1.2M to £5M. There was a small inflow from working capital, with a larger fall in inventories than last year so that the net cash from operations was £5.8M, a decline of £645K year on year although there was a £1.9M operating cash outflow from the acquisitions. The group spent £3.2M of this on intangible assets and £118K on property, plant and equipment before the £38.8M spent on the acquisitions meant that before financing there was a cash outflow of £36.2M. The group issued new shares to cover the bulk of this, with proceeds of £19.9M before a £2.9M dividend payment meant that the cash outflow for the year was £18.6M to give a cash level of £2.1M at the year-end.

The integration of Entone has been substantially completed with key technical, operational and marketing decisions taken. Cost synergies continue to track ahead of previously stated expectations with the full benefit being reflected in 2016. The board have realigned the group to create two drivers of growth, which are Hybrid TV and Cloud Services. The acquisition of Booxmedia provided the basis for the latter but it will also include Fusion Home and other cloud offerings.

Booxmedia sales and marketing plans have progressed well with two major customer wins secured in the second half of the year. Dutch utilities and digital services company DELTA selected their white-label platform and products to provide, install and maintain a new end to end multiscreen cloud TV solution. Also Belgian broadcaster RTL selected the group to provide, install and maintain a full end to end cloud video on demand platform.

Following the acquisition of Entone, the company has engaged in a number of new hybrid TV opportunities based on its portfolio. After the period-end, the group and Cincinnati Bell Telephone have started the migration of legacy IPTV devices to Amino’s Enable TV software platform, instantly enabling Cincinnati Bell’s entire Fioptics TV installed base to be upgraded with a rich media interface and advanced applications. The group has launched the new 6 Series, a comprehensive 4K Ultra HD and HEVC hybrid TV device range.

Strong demand remains for simple, reliable IPTV devices, particularly in emerging markets, but more and more customers are looking to operators for higher performance devices that can blend traditional IPTV with OTT content delivered over the internet. The transition to all-IP entertainment delivery has continued as has the growth in OTT video consumption, especially on mobile devices and the increasing importance of interconnectivity between devices around the “TV everywhere” concept. At the same time the timeframe within which new 4K Ultra HD services are expected to be developed by service providers has also shortened.

The group have developed a new integrated sales organisation across the enlarged business, directed by Steve McKay who led Entone’s international expansion and secured a number of tier 2 customers such as Cincinnati Bell in his former role as CEO of Entone. The company now has a targeted sales focus in all key regions with dedicated teams for Latin America and Europe and a new combined sales team for North America.

Some parts of Eastern Europe remained challenging and Serbia saw the potential consolidation of a major customer, impacting further roll out of their IPTV solution which resulted in a sharp drop in sales. The rest of Europe saw growth, however, with additional sales to France, Switzerland and Malta with continuing demand in Albania. Consistent demand was also seen in Chile whilst rest of the world revenue increased with ongoing demand in Argentina and the enlarged group brining sales in some new territories including Trinidad and Moldova.

One area of focus for R&D was cable hybrid and during the year the group introduced further x5x products with the A550 and H150 which are further variants of the mainstream A150 IPTV device, leading to more resource being involved in the enhancement and support of products.

There is some susceptibility with the exchange rate against the US dollar with a 5% strengthening of Sterling against the currency giving rise to a decline in profits of £100K. Despite a £2.8M decline in sales from the group’s largest customer in the USA, the client still represents 18% of total revenues. There also another US-based customer that accounts for 14% and a Dutch customer that accounts for 10%, which represents a new client for the group following the Entone acquisition.

The group has also announced that CFO Julia Hubbard has resigned with immediate effect having spent five years in the role. The finance operations will continue to be led and managed by Julian Sanders who has been interim CFO during Julia’s leave.

There were two acquisitions during the year. In May the group acquired Booxmedia, a software as a service cloud TV platform provider. The business was acquired to enhance the group’s offering by adding a field-proven cloud-based platform which can enable the delivery of “TV everywhere” entertainment to a full range of IP connected devices as it becomes more important in the industry. The total consideration was £7.5M with £5M satisfied in cash on acquisition and most of the rest contingent consideration and the business contributed £66K to the group’s profit during the year and the acquisition generated goodwill of £4.7M.

The other acquisition was Entone, which was acquired in August. The business is a provider of broadcast hybrid TV and connected home solutions and it was acquired to increase the group’s global footprint and scale as well as to consolidate a direct competitor. The consideration was £41.1M, all in cash and the acquisition generated goodwill of £25.6M. Since the date of acquisition the business contributed £2.4M to the group’s profit which shows what a dramatic reduction in profitability the rest of the group suffered. Curiously, has the acquisition been made at the start of the year, the business would have contributed a loss of over £300K which is rather concerning.

As can be seen there were a number of exceptional items that occurred during the year. There were acquisition costs of £1.4M, of which £300K related to the acquisition of Booxmedia and the rest was related to the acquisition of Entone. There was also contingent remuneration payable relating to the Entone acquisition. There were general integration costs of £272K which included additional travel and contractor costs resulting from activities to integrate the new enlarged group; there were development project costs expenses of £103K and amortisation costs of £1.3M resulting from the rationalisation of the new group’s product roadmaps; and redundancy costs of £342K. Finally, there was a final rebate of £744K in respect of duties paid on previously recognised international product sales following the favourable ruling at a tax tribunal in January 2015.

The group has a decent amount of access to funding should it be required with an undrawn facility of £15M although £5.1M was used during the year around the time of the Entone acquisition.

Overall the board reports a positive outlook for 2016 and feel that the group is well placed to deliver growth in the year.

At the current share price the shares are trading on an underlying PE of 16.1 which falls to 12.6 on next year’s consensus forecast. After a 10% increase in the dividend, the shares are currently enjoying a yield of 4.7% which increases to 5.2% on next year’s forecast after the board stated they will increase the dividend by at least 10% again in 2016.

Overall then, this is a bit of a disappointing set of results. Profits declined, although if we take out the acquisition related costs, they were up. It has to be said, though, that the performance in the second half was much worse than the first half and that includes a contribution form the acquired businesses so the underlying performance in H2 must have been terrible. Net tangible assets were also, down and there is not a negative tangible book value which is never good to see. The operating cash flow declined, although if we take out the acquisition-related operating items the cash profits were broadly flat. Before the acquisition there was some free cash flow but not enough to cover the dividend and I have to say I think it is a bit reckless to commit to an increase in the dividend next year when it was not even fully covered by operating cash flows this year.

The two acquired businesses at least do seem to be performing well and the Entone acquisition has apparently resulted in better synergies than expected and Booxmedia is progressing nicely. Following the difficulties in the sale team, that has now been restructured but the fall in sales doesn’t just seem to be sales team-related here. They mention that in Serbia a potential consolidation of a major customer has resulted in falling sales in that country. Indeed, sales there have been almost eradicated by this event. I am not sure exactly what the potential consolidation of a customer means but this hints at more wrong here than is being let on in my view.

With a forward PE of 12.6 and dividend yield of 5.2% the shares look cheap on the face of it but I am not happy about these results and I will not be investing. In fact, this will be my last update here unless things change materially for the better when I will revisit them. What a shame.

On the 29th February the group announced that Karen Bach was joining as a non-executive director and will replace Colin Smithers who retires today after spending fourteen years in the role. Karen has spent the last twelve years working as CFP at various software businesses before founding KalliKids in 2012 where she is CEO.

On the 6th June the group released a trading update covering the first half of the year. Trading for the period was in line with market expectations with regards profit but net cash of £3.1M was above expectations.

The group delivered a decent performance with record order intake and an encouraging backlog to take into the second half of the year following sales growth in key regions. The integration of the two acquisitions was completed during the period and cost savings from synergies between the businesses are in line with previously revised expectations.

Sales performance was particularly strong in Latin America with repeat orders from existing customers and new contract wins from operators transitioning to IPTV deployments as part of fibre network rollouts. There has also been continued traction in North America, across both IPTV and cable customers with good progress in the contract with Cincinatti Bell to migrate its legacy IPTV devices to the group’s Enable TV software platform. A number of new customer wins have also been secured in the region during the period.

In Europe there was the renewal of an existing contract with Vodafone Netherlands and the recent launch by Dutch operator DELTA of cloud TV services, based on Amino’s platform, underlines the growing appetite for multiscreen entertainment service delivery. The board is recommending a dividend increase of 10% and it seems to me that the worst might be over here – I am considering buying back in although would prefer to wait to have a gander at the balance sheet at the upcoming results next month.