Vast Resources has now released its interim results for the year ending 2016.

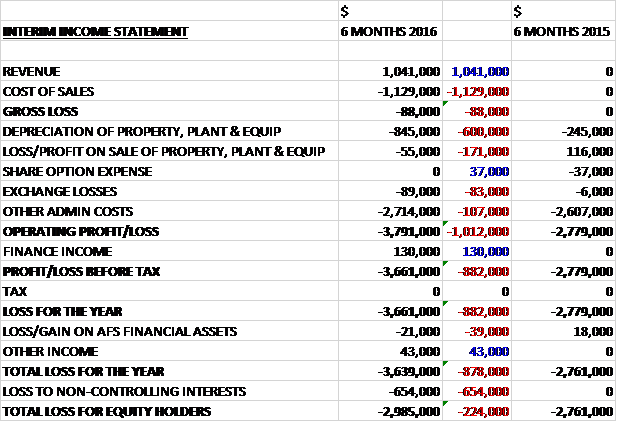

We now have some revenues with a two month contribution from the mines but they were below cost of sales which meant that there was a gross loss of 88K for the period. Depreciation increased by $600K and there was a $171K negative swing to losses on the sale of property, plant and equipment, and after an increase in some other admin costs, the operating loss was $1M worse than in the first half of last year. There was a finance income of $130K, however, which gave a total loss attributable to equity holders of $3M, an increase of $224K year on year.

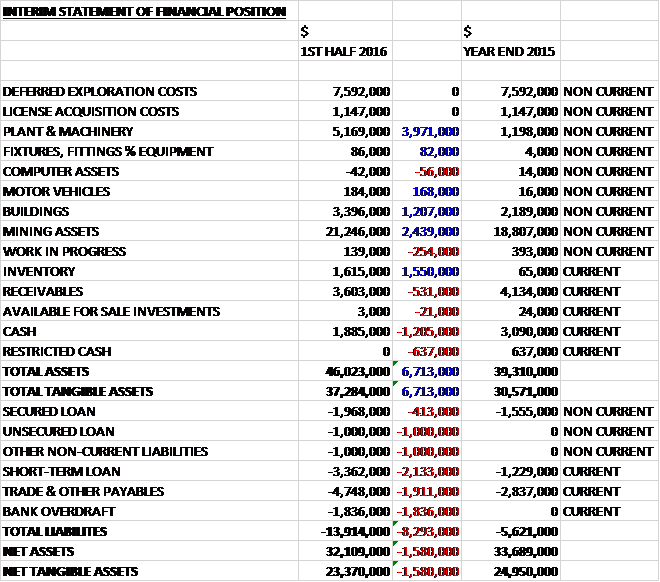

When compared to the end point of last year, total assets increased by $6.7M driven by a $4M growth in plant and machinery as they were moved from assets under construction, a $2.4M increase in mining assets, a $1.6M growth in inventory and a $1.2M increase in the value of buildings due to acquisitions, partially offset by a $1.2M fall in cash, a $637K decline in restricted cash and a $531K decrease in receivables. Incidentally I am not sure how they managed to get a negative $42K of computer assets on the books – I have not seen that one before! Total liabilities also increased during the period due to a $5.4M growth in borrowings, a $1.9M increase in payables and a $1M growth in “other” non-current liabilities. The end result was a net tangible asset level of $23.4M, a decline of $1.6M over the past six months.

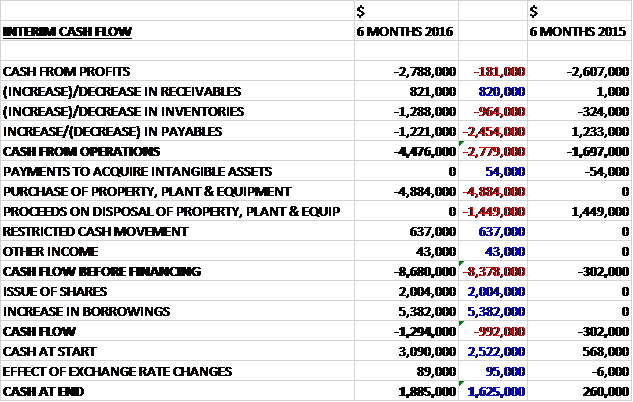

Before movements in working capital, there was an operational cash outflow of $2.8M, a detrimental movement of $181K when compared to the first half of last year. We then see a cash outflow through working capital with an increase in inventories and a reduction in payables so that there was a $4.5M cash outflow from operations, an increase of $2.8M year on year. The group then spent $4.9M on property, plant and equipment to give a cash outflow of $8.7M before financing and after the issue of shares brought in $2M and the group increased borrowings by $5.4M, there was a cash outflow of $1.3M during the period and a cash level of $1.9M at the period-end.

The gross loss has arisen during the first two months of production where throughput has not yet reached a steady state level which allows for full absorption of mining and processing costs but management are confident that the trend will reverse in the second half of the year.

The period saw the first gold pour at Pickstone-Peerless in September and the first sale of concentrate at Manaila Polymetallic mine, also in September. The construction and commissioning of Pickstone-Peerless has therefore been completed and production at the mine is ramping up to a steady state. Exploration activities in Zimbabwe and Zambia have been terminated apart from the Nkombwa Hill rare earth project in Zambia which is being funded and managed by a partner.

Production at the Baita Plai mine is planned to start in early 2016 and a small administrative office has been established in Romania to assist in the management of the two mines.

The short term objectives at the Manaila Open cast mine include improvements to the open cast mine to facilitate increased mining volumes and compliance with international best practices; expansion of the mining license area to increase the potential to expand the mine life; the undertaking of an exploration programme to firm-up the expansion of the phase one open pit and phase two underground mining resources; the completion of metallurgical test work on the ore to assist in the design of the proposed processing facilities that may be constructed at the mine, subject to a positive feasibility study, to avoid transporting ore 34km to the Iacobeni concentrator, and tailings 20km to the tailings facility; and the conversion of the resources and reserves defined according to the Russian code to JORC, which will be undertaken in 2016.

At the Iacobeni Concentrator, the short term objectives include the recommissioning of the second ball mill to increase milling capacity to 20,000 tonnes per month; the repair and re-commissioning of the second and third float lines to facilitate the production of high quality copper concentrate and high quality zinc/lead concentrate; the upgrade of the milling and flotation facilities to comply with international standards; the elimination of material double handling wherever possible; and establishing warehouse facilities for concentrate to make timeous payments for concentrates sold without waiting for transport delays.

At Baita Plai, the short term objectives include re-starting the underground mining operations in early 2016 with an initial steady state objective of 10,000 tonnes per month; the recommission of two of the three ball mills, the service of four flotation circuits and the recommission of a fifth for molybdenum; the start of a study to increase production to 20,000 tonnes per months which is the total installed processing capacity; the conversion of the resources to JORC; the review of current mining methods and plan to reduce waste volumes; to undertake a feasibility study on the benefits of beneficiation of ore prior to milling; the evaluation of near surface resources in adjacent undeveloped skarn pipes for future mining; and the planning of systemic modernisation of all mining and processing equipment and plant.

The group are also looking to re-engage with SC Remin and the government of Romania to negotiate the acquisition of target mines identified during the exclusivity period that resulted from the past memorandum of understanding entered into by Remin and Vast but at the request of the government, negotiations have been suspended pending changes planned for mining and investment in the country which are expected in 2016. The group have also been offered additional mining projects which are being evaluated.

While the group is now earning operational income on Manaila and Pickstone-Peerless, it will require additional funding in order to meet its capital requirements to bring Baita Plai Polymetallic mine into production and for further capex required to increase production. The company is in an advanced discussion with a funding source and the directors are very confident of being able to raise such funds as are required.

In July the group concluded an agreement to purchase 50.1% of the share capital of Sinarom Mining for €1. Sinarom currently operates the open pit mine at Manaila Polymetallic mine. No assets were acquired with the business as they were offset by payables but management is of the opinion that the final fair value of this acquisition is in excess of the amounts stated.

In November, the appeal court of Cluj confirmed the merger with Mineral Mining in Romania. The group has therefore been advised that it has a direct legal right to obtain the right to mine at Baita Plai Polymetallic mine without any further legal argument from the holder of the head license, Baita and that the grant of the mining sub-license should now only be a matter of due process. In December the company received a letter from Baita to request a meeting in January to conclude the grant of the license. This grant requires the approval of the Romanian National Mining Agency and such approval is required to be given if Vast fulfils the criteria laid down under Romanian mining law, which the directors expect to be satisfied.

In July the company announced that the lender of the short term loan of $1.22M had notified them that the conversion rights would be exercised so 154,649,140 shares became due to be issued to the lender at an issue price of 0.5p which were issued after the period end, in October. Also in October, 7,500,000 new shares were issued due to an exercise of warrants for a cash consideration of £42K; and 23,097,237 new shares were issued to a consultant to satisfy obligations to pay commissions in relation to a prior fundraising.

After the period-end the cash level fell to just $250K as of the end of December.

On the 4th January the group announced that it has entered into an agreement with Crede Capital whereby they will subscribe for new shares in order to raise up to £5M. 156,250,000 new shares will make up the first tranche of the subscription shares at an issue price of 0.8p per share and in addition, the same number of warrants to acquire shares in the company have been issued, exercisable up to 2021. Overall there will be four tranches, occurring quarterly with each tranche raising £1.25M with the issue of 156,250,000 shares and an equal number of warrants.

For each subscription of shares by Crede Capital, a commission equal to 10% of the aggregate purchase price of the shares may become payable by the company to Crede in the event that Crede subsequently subscribes for shares pursuant to the exercise of warrants. Crede is apparently a passive investor and does not seek board seats or control positions.

On the 6th January the group announced that certain directors subscribed for 62,500,000 shares, raising £500K along with warrants on the same terms that Crede have been issued shares.

On the 8th February the group released a quarterly production summary. The Manaila Polymetallic mine and the Pickstone-Peerless gold mine were both commissioned in August and operationally the two mines have achieved break even status in the quarter to the end of December. Costs and efficiencies are improving and further improvements are possible going forward.

At Manaila, the mining rate averaged more than 11,200 tonnes of ore per month. During the quarter the existing operational mill was still ramping up to its design capacity of 10,000 tonnes per month and has undergone a full refurbishment, including new liners. The second mill, currently non-operational, is being refurbished and is expected to be in production from April. With both mills operational, the mine will have an installed milling capacity of 20,000 per month.

In conjunction with the increased procession capacity, a second flotation line is being installed enabling the mine to produce separate copper and lead/zinc concentrates. Metallurgical testwork undertaken by the company indicates that the second flotation circuit will increase plant recoveries resulting in higher-grade concentrates. In addition to the improved grade, moving away from a bulk concentrate will increase the marketing flexibility of the product.

In all, the mine mined 33,756 tonnes of ore and milled 26,375 tonnes which produced 745 tonnes of concentrate, of which 550 tonnes were sold in the period. The cash costs of the concentrate was $1,064 per tonne with an average selling price of $1,033 per tonne so not much money being made here yet.

At Pickstone-Peerless, the plant processed an average of 15,400 tonnes per month at an average plant head grade of 1.97g/t, producing 2,601 ounces for the quarter. The strategy is to now work towards achieving up to 20,000 tonnes per month. Head grades during the quarter were negatively impacted by the presence of artisanal miners in the shallower parts of the mine. With the assistance of the authorities, the miners have now been removed and the short term mine plans are being reviewed in order to optimise the tonnage and mill feed grade. Consideration is now being given to the further higher grade sulphide resources that are scheduled for future mining.

During the quarter the mine mined 46,285 tonnes of ore with a similar amount being milled which produced 2,601 ounces of gold, of which 2,375 ounces were sold. The cash costs were $831 per ounce of gold and the average sales price achieved was $1,080 per ounce.

On the 7th March the group announced that it had entered into an agreement with a number of existing shareholders whereby they will subscribe in four tranches of new shares and associated warrants in order to raise up to £800K. The first tranche of the financing of £400K was completed on the 4th at an issue price of 0.8p resulting in 50,000,000 new shares being issued with the same number of warrants. The next three tranches will be priced at the closing price of the shares on the prior trading day and will raise £133K each.

At Manaila, there are two installed ball mills and associated flotation circuits. At present one ball mill and part of the flotation circuits have been successfully re-commissioned, providing the mine with processing facilities of up to 10,000 tonnes of ore per month. About 250 to 300 tonnes of copper concentrate are being produced per month. The single flotation circuit results in high levels of zinc and lead in the copper concentrate which reduces the per tonne value of the concentrate. The unrecovered lead and zinc is being lost.

In order to improve revenues, it is therefore necessary to commission the second mill and flotation circuit, produce a copper concentrate with much lower levels of lead and zinc, to produce a high grade lead and zinc concentrate, to increase monthly tonnages from 10,000 tonnes to closer to 20,000 tonnes, to improve plant efficiencies, and to reduce transport and double handling costs. The funding from Crede has been facilitating and will continue to facilitate the above improvements but the staged instalments from Crede delays the full implementation of these improvements and the positive financial impact that they are expected to have hence the additional funding that has been sought.

Gold production at Pickstone-Peerless is in line with expectations. Costs are stabilising at anticipated levels and the higher gold price is improving revenues. The plant design capacity of 10,000 tonnes per month has been exceeded and is currently operating at 15,000 tonnes per month. The expected production of about 30kg per month is being achieved as a consequence of this increase throughput and the group continue to evaluate operational improvements.

Examination is in process so as to decide the best option for the start-up of some small scale mining at the 500,000 ounce Giant Gold Mine, whilst a better understanding of the potential of the mine is determined through exploration activities. The gold occurrence is open at depth and along strike and further drilling is necessary to determine the extent of the in-situ gold potential. Exploration work by former holders of the mining claims suggests that the mine has the potential of a larger resource.

The Baita Plai mine is being readied and prepared for the investment required for its restart after receipt of the license that is currently still being processed by the authorities.

The company’s options for utilisation of surplus funds after the expansion of operations at Manaila, the restart of Baita Plai and the receipt of the final tranches of the Crede investment include an estimated $350K for expanded phase one resource drilling at Manaila as part of the overall drilling programme expected to cost a total of $800K when finalised, which includes the work necessary to convert the resources to the JORC reporting code; an estimated $500K for resource drilling at Baita Plai; an estimated $50K for auguring and assaying of the tailings dam at Baita Plai to assess the potential of retreating the dump for any contained minerals; and estimated $200K for upgrading the lab at Manaila to facilitate assaying for gold and silver concentrates prior to shipping ; and the design and construction of a milling and flotation circuit at Manaila to remove the transport costs of ore from the mine to the mill and flotation facilities to the tailings facility.

Overall then there has been some considerable progress over the period with both the Pickstone-Peerless and the Manaila mines starting up and broadly breaking even. There are continued delays at Baita Plai, however. The group is obviously consuming some considerable cash at the moment and whilst the Crede Capital investment is welcome, it was not enough and new shares have been issued like confetti. I feel that at the moment with the amount of ongoing dilution taking place this is not something I want to be invested in but I will keep it on watch.

On the 16th March it was announced that having sold their last tranche of shares, Crede were converting 32,200,000 warrants to shares at 0.8p which meant that the group issued just over 55M new shares to Crede and they now own 2.77% of the total share capital. Inexplicably, pursuant to the terms of the subscription agreement, an admin charge is due to the investor of £55K! Incredible! I’m not going anywhere near these until this agreement has finished.

On the 30th March the group announced the extension of the prospecting license at Manaila. The current mining license covers an area of about 0.0675km squared and following the extension will cover an area of about 1.323km squared, an increase of more than 20 times. Historical exploration has indicated that the ore body extends to the NW and SE and on completion of the exploration programme, the defining of reserves and resources, and the preparation of a mine plan, the group is entitled to apply for a mining license on the additional area.

Resource drilling completed in Q3 2015 on the existing mining license has indicated a likely increase in the current open pit resource. Additional open pit mineralisation has been identified to the SE of the current resource, which will be targeted during the Phase 1 drilling campaign, planned to start in Q2 2016. It is expected that the group will be able to convert all of the resource to the JORC reporting code during Q4 2016.

This is all very good but these shares are not going anywhere until the ridiculous financing agreement with Crede is sorted out…

On the 5th April the group announced that it has decided not to give consent to the subscription of £1.25M from Crede, the second tranche of the financing agreed. The grounds for withholding this consent are that the subscription for the tranche would result in Crede being interested in more than 25% of the share capital of the company.

The company’s share price has fallen substantially since the financing was agreed (this is not a coincidence!) and as a result of this, the ordinary shares of 0.1p each issued to Crede on exercise of certain warrants granted to it as part of the first tranche of financing have been highly dilutive to shareholders. The new shares that would have been issued to Crede as part of the second tranche would have been issued at 0.24p per share and would have entitled them to a futher 520,833,333 shares with an equal number of warrants.

The cancellation of this tranche does not affect the contractual rights and obligations between the parties in relation to the third and fourth tranches but the directors intend to replace the second tranche of £1.25M so that the momentum of increasing production can be maintained. Initial discussions indicate that the terms of this funding will be on more favourable terms and on a basis that will not conflict with the terms of the subscription agreement.

This is certainly a positive development but it is unclear how this affects the relationship with Crede, how easy it will be to gain this financing from elsewhere and also how the further two tranches will affect the share price.

On the 6th April the group announced that it has received subscription of £133K for the issue of 55,555,550 new shares at an issue price of 0.24p per share and 55,555,550 warrants pursuant to the agreement entered into with a number of existing shareholders.

On the 11th May the group released an operational update covering trading in Q1. At Pickstone-Peerless the plant milled 54,237 tonnes and produced 2,808 ounces of gold, an increase of 17% and 8% on the previous quarter. Operational efficiencies have started to take effect with production costs decreasing in line with gold production. Head grades averaged between 1.9 and 2.1g/t during the quarter and are expected to increase in future as the open pits are developed to deeper levels. Overall 2,475 ounces of gold was sold at an average price of $1,139 per ounce and cash costs of $910 per ounce, both of which increased 5% quarter on quarter.

The improved production profile has continued into the current quarter with the milling tonnage again exceeding 20,000 tonnes in April which along with the higher grades enabled the monthly production to exceed 40Kg of gold for the first time. The domestic bank overdraft has been reduced from about $2M at the start of operations to $1.2M in early April. Attention is now being focused on the design and installation of the sulphide processing plant which will be required for the next phase of mining once oxide resources are depleted. In addition, development at the nearby Giant Gold Mine is being considered although further exploration work is required to increase the current inferred resource of about 500KT.

At Manaila, the group has undertaken a number of capital projects to improve operational efficiency, including some maintenance work which had been neglected by the previous owner. As a result, some plant downtime was incurred and furthermore, severe cold weather in January negatively impacted flotation recoveries which resulted in a reduced concentrate quality. Additional mining areas were exposed in anticipation of the increased plant throughput, resulting in an increase in waste tonnage mined whilst the single, mainly copper concentrate, produced during the quarter contained high levels of zinc that resulted in the mine incurring penalties when selling.

In order to reduce the quantity of zinc in the product, a second flotation circuit has been constructed during the quarter and is now being tested, along with new reagents identified by flotation test work. Additional capital projects undertaken include the relining of the new primary mill which was completed towards the end of the quarter allowing for higher milling tonnage throughput and improved grind and recoveries. The refurbishment and relining of an older second mill also started during the quarter and was commissioned in April. This mill is being tested as a regrind mill which will enable separate copper and zinc concentrates to be produced. In addition to now having the ability to produce two saleable concentrates, the grade of the copper concentrate is expected to improve and with the production of a separate zinc concentrate, the penalties of zinc in the copper product will decline. With both mills operational the mine will have an installed capacity of 20,000 tonnes per month from May.

More intensive metallurgical test work has been commissioned for the mine with two objectives in mind. The first is to provide data for the design of the new milling and flotation circuit that the group wishes to construct at the open cast mine site to avoid the extensive ore and waste transport costs associated with using the concentrator 34 km away. Secondly the data will be used to determine the optimal process flow at Lacobeni using the existing concentrator until the new unit is constructed at Manaila.

In all Manaila mined 20,362 tonnes of ore and milled 22,510 tonnes to produce 677 tonnes of concentrate which represents a 40%, 15% and 9% decline respectively. The amount of concentrate sold increased by 57% to 866 tonnes, however. The average sales price declined by 8% to $949 per tonne of concentrate but due to the zinc contamination, cash costs increased by 45% to $1,542 per tonne so this is certainly not profitable at the current time.

The Baita Plai license process is apparently nearing completion. All the legal work to facilitate the merger has been completed. Numerous legal proceedings by parties opposing the merger have also been concluded and meetings between various parties are to be convened shortly to arrange the granting of an associate mining license. The group has undertaken certain capex to comply with underground mining safety which includes new man-carrying cages, hoist ropes and making safe areas that will be accessed in the initial stages of reopening the mine. Metallurgical test work will be undertaken during the rehab of the mine and processing facilities to confirm that the current processing layout is appropriate.

The group also announced that they have been granted a prospecting license over the Faneata tailings dam located 7km from Baita Plai. This license constitutes a separate right from the anticipated right to mine at BPPM itself. The 4.6MT dam is comprised of forty years of tailings from Baita Plai and historical data indicates that they contain economic quantities of minerals including gold, silver, copper, lead and zinc. The company will undertake an 825m auger exploration programme starting in Q3 to upgrade the dam to a JORC compliant mineral resource and thereafter undertake a feasibility study to assess the viability of the resource. The total cost for the drilling, assaying and feasibility study is expected to be just $125K.

The dam has the potential to be a stand-alone mining operation when enhanced processing technologies that have the ability to enable the economic extraction of the metalliferous content of the tailings are used. A sampling programme undertaken in 2011 estimated that the dam contains 4,080 tonnes of copper, 6,640 tonnes of zinc, 3,100 tonnes of lead, 35 tonnes of silver and 309kg of gold. This dam seems as though it will provide a decent source of feedstock and it will also reduce operational risk by having two sources of feed for the processing facility.

On the 16th May the group announced that it had entered into a bridge loan with Darwin Capital for up to £1M. An initial note of £650K, which will be used for ongoing capital requirements, has been issued so far. The note will mature in two halves, with the first falling due on the 10th July and the second on the 10th October. It will accrue hefty interest of 20% per annum. If the company fails to pay on these says, the amount owed will increase to 120% of all outstanding payment obligations and the dates will move to 10th January and 10th April. Also, if this happens, Darwin will have the right to convert the amount outstanding into shares at the prevailing price.

The purpose of the loan is to provide cover for the working capital requirements until the Crede Tranche 3 financing has taken place which they will use to pay off the loan. I would have thought this just kicks the can down the road a bit but desperate times call for desperate measures I guess.

Overall then, the gold mine seems to be working well and contributing but the Manaila mine is consuming cash rather than making it at the moment and the license for the Baita Plai is still not forthcoming. The group are sailing very close to the wind with regards financing at the moment and I feel that buying shares here is akin to gambling – when(if) the license news comes in for Baita Plai I would expect a short-term jump in the share price, however.

On the 16th June the company released an update. As has been mentioned previously, due to movements in the share price the authorities granted to the company at the general meeting may not be sufficient to allow them to issue the Tranche III shares to Crede together with the warrants. In order to issue the shares on the 4th July, the date for the next issue, they are obliged to seek further authority to allot rights.

The group expected that it will utilise part of the amount drawn down from Crede in the Tranche III issue to pay the amounts due to Darwin on the 10th July. In the event that they do not repay this, Darwin will have the right to exercise the conversion. The company is therefore seeking the authority to allot and to disapply pre-emption rights to issue shares to Darwin in the event that they are unable to pay back the loan. They are further seeking to refresh its existing allotment authority for rights up to an amount of £500K until the next AGM.

The company most definitely needs this cash. The recent fall in copper and lead prices has reduced cash flow from Manaila. It has been further affected by the reduced concentrate grade at the mine as a consequence of extreme cold weather in Q1 and the commissioning of the second mill and flotation line. Cash flow from Manaila and Baita Plai had been expected to fund a significant part of the group’s capex.

Curiously the group have stated that shareholder support for the share price is now sought to ensure that the future tranche of shares are issued at increasing share prices – as if shareholders could control the price of the stock somehow! I suppose they are pleading to shareholders not to sell!

If resolutions 1 and 4 are not passed at the upcoming GM, the group has the right to terminate the subscription agreement with Crede. On termination, all of their obligations to Crede will fall away and the company will have to identify alternative sources of funding which could include an open offer.

In Zimbabwe, Pickstone-Peerless is producing higher than expected grades and milling tonnages are significantly above the original design capacity of the plant. In April and May the total tonnage milled has exceeded 20,000 tonnes per month in both months, producing more than 2,900 ounces of gold during that period. A better understanding of the ore bodies is being developed as the open pits are expanded and the grade control drilling provides additional information.

Additional potential ore sources are also being evaluated within the existing mining lease. The mine is also considering improvements and additions to the existing oxide plant which would form part of the expansion of the processed facilities that will handle the higher grade sulphide ore to be mined when the oxide resources are depleted.

The company is now looking to develop the Giant Gold Mine where there is currently an inferred resource of about 500K ounces of gold. They have secured additional information and further exploration drilling now needs to be undertaken to upgrade and increase the known level of resources at the mine. Artisanal miners working in the area will need to be relocated and consultations with their representatives have begun. The mine provides the company with the potential to develop a second significant fold mine and management will now focus on this objective.

At Manaila, Q2 has seen the mine face a number of challenges that have impacted performance. Extreme cold weather in January and February affected recoveries as the heating of the flotation facility and cells was not adequate and it was not possible to upgrade the heating system in time. It will now be upgraded for the next winter. The mine is also still producing a combined copper and lead concentrate, which incurs penalties with the refurbishment of the flotation circuit that is designed to prevent this not being ready until the end of June. Additionally it was expected that a change in reagents and the separated flotation circuits should result in improved recoveries, a clean copper concentrate and a second zinc concentrate but initial application of the test outcomes to the plant did not achieve the anticipated results.

The delay in obtaining the right to mine at BPPM is still ongoing. Not only has it delayed cash flow generation from what management regard as the company’s most valuable asset but also monthly dewateing and maintenance costs are being incurred. The company remains confident that it will obtain its due right to mine at BPPM but it has had little control over the speed of the process. Some more information regarding the whole sorry saga has been given.

The legal process for the merger was started in February 2015 and at the time the group was advised that the process would be complete by May 2015. The previous management of Baita were uncooperative, however, and the whole legal process was spun out until a final court of appeal decision was reached in November 2015 confirming the merger with the termination of the bureaucratic process following this decision occurring in February this year.

While the legal proceedings were taking their course, the company was attempting to bypass the legal process by negotiation with the government. In a meeting, the president of the Romanian Mining Agency, a secretary of state at the ministry of economy and the minister of economy promised a swift resolution of the matter which resulted in a new agreement announced in November.

Unfortunately the then government was removed and the ministers were replaced by people who were not familiar with the background of the situation and it has taken a long time to promote a proper understanding of the facts. Since February there has been new management at Baita and it has become evident that there is now no opposition in principle from any quarter to the company receiving the sub-license. The new secretary of state verbally confirmed in February that it would be granted upon clarification of the current position which could take up to the end of April.

The process has, however, remained slow for a number of reasons. One of the senior directors of Baita was in hospital for about five weeks which meant, under the Romanian system, that they were not able to hold any board meetings at all during that period. Meetings at the ministry of economy have taken a long time to arrange due to other pressures on them and the fact that key officials have been on holiday or on assignments! The officials still have no clear understanding of the detail involved and seem to be acting on different information.

In particularly, the previous management of Baita had materially overcharged for dewatering costs prior to Vast’s involvement. The amount that will become due to Baita on grant of the sub-license is subject to judicial audit that is still ongoing but in the interim the court has ordered that the maximum amount due is about $620K and the group have offered to pay this sum into an escrow account against delivery of the license.

The amount shown as due in Baita’s official accounts is about $1.7M, however, and although their current management accept that only $620K is legally due, this fact has never been communicated to the section of the Ministry of Economy within whose remit the shares in Baita lie. The ministry has now understanding as to why the group should not be paying $1.7M and the lack of provision of this information has only been revealed to the group over the past week.

The up to date position is that Baita has now mandated its GM to confirm the current position officially in writing to the relevant section of the ministry and the company is in advanced discussions to procure the additional funding required for the deposit in the escrow on terms which are considered acceptable to the company.

You really couldn’t make this up! It does seem as though the license should be forthcoming soon, but we have been in that position before and with material uncertainty surrounding funding I am not going near these shares for the time being.

On the 1st July the group announced that at the GM, resolutions 1 and 4 were defeated. These resolutions were required to five the company authority to issue shares sufficient to meet the requirements of the Crede tranche three which means the financing is cancelled in accordance with its terms.

On the 5th July the group announced that it had received a subscription of £133K for the issue of 37,037,036 new shares at an issue price of 0.36p per share and the same number of warrants. This represents the third tranche of financing. They have also announced the appointment of Brandon Hill Capital as joint broker.

On the 6th July the group announced that it has raised $1.14M before costs through a placing and subscription of 300,000,000 shares at a price of 0.285p per share. These shares will represent about 10.4% of the enlarged share capital of the company.

Whilst this is clearly good news, there remains a dire need of further capital here and for that reason I remain un-invested.

On the 14th July the group gave an update. Following the rejection by shareholders to grant additional head room to facilitate the third tranche of finance from Crede on the ground that its terms were too onerous, the group needed urgent injection of cash. They found support at 0.285p per share which came from the shareholders that voted down the Crede offer, together with other new shareholders identified by the new broker. At that price, the maximum sum that could be raised was £855K because they had available authorities to issue about 300M shares.

They will need further funding to allow the company to fulfil its development programme and therefore the directors are now proposing an open offer to shareholders on the same terms as the placing. Unfortunately the shares have been in decline so that 0.285p does not now represent an attractive discount but warrants attached to them might have some appeal. It is expected therefore that the open offer might not be enthusiastically supported. As such the group may seek to raise capital at project level, entering into financing structures that limit dilution at the company level or to enter into joint venture arrangements. The directors will not be participating in the open offer as they deem that they are in a close period.

Since the last update, production continues above expectations at Pickstone-Peerless and satisfactory progress was made towards advancing the grant of the sub licence at Baita Plai. At Manaila, progress was made concerning the separation of the copper and zinc concentrates. Improvement suggested by consultants are being implemented and consultants will remain on site for the next two months to monitor progress.

The group needs about £4.1M over the next six months. £1.2M is needed for loan repayments, £752K is needed to pay liabilities on taking over the mining sub-license, £684K is needed for general capex, £555K is needed for working capital, £456K is needed for start-up working capital and £456K is needed to pay acquisition creditors at Manaila. This clearly shows the further sums needed to make up the balance.

So, after not including private investors in an open offer when the placing was done at a discount, they are now “generously” including offering shares, which are worth 0.25p on the open market and opportunity to buy shares in an open offer at 0.285p! Of course the directors are not taking part in the open offer but that is not because it is a terrible deal of course, that is just because they are in a close period! It is very clear that the company desperately needs cash, and more than has been raised at the latest placing. This is all a terrible mess.

On the 28th July the group announced the appointment of Peterhouse Corporate Finance as joint broker and they have terminated their relationship with Daniel Stewart. They also announced that they repaid the £325K loan to Darwin, being half of the Bridge loan note.

On the 1st August the group announced that nearly 52% of shareholders opted to take part in the open offer which meant the issue of 181,992,582 new shares and the receipt of £519K. I have to say I am surprise it has been this successful and the group should be able to keep going until the next fundraise for a little longer now.

On the 11th August the group announced the results from the drilling operation in Manaila which is anticipated to produce JORC compliant resource at the mine in Q3 and to extend its life. Highlights include 11.7m @ 1.19% Copper and 0.69% Zinc from 20m in FZ60; 8.5m @ 1.47% Copper and 1.03% Zinc from 54m in FZ67; 13.9m @ 1.11% Copper and 0.31% Zinc from 25m in FZ3; and 17.8m @ 2.34% Copper and 1.83% Zinc from 30m in FZ4.

On the same date the group also announced that it had raised £364K before costs through a placing of 128,035,087 shares at a price of 0.285p per share.

The group has now released a quarterly update. At Pickstone-Peerless, the group mined 83,035 tonnes of ore, an increase of 30% quarter on quarter. They milled 61,577 tonnes with the plant now at steady state, and produced 4,542 ounces of gold, an increase of 62%. The average sales price achieved increased by 8% to $1,229 per ounce and cash costs fell by 24% to $695 per ounce.

Attention is now being focussed on the design of the PPHM sulphide processing plant that will be required when the oxide resources are depleted in the open pits. In addition, development at the nearby Giant Gold Mine is being considered. Further exploration work is required to increase the current inferred resource of about 500,000 ounces.

At Manaila, the group mined 24,711 tonnes of ore, an increase of 21% quarter on quarter. They milled 29,830 tonnes, an increase of 33%, but the concentrate produced declined by 12% to 727 tonnes due to the inclusion of an additional 144 tonnes of low-grade concentrate that was initially stockpiled. The average sales price increased by 4% to $844 per tonne but cash costs ballooned by 45% to $1,341 per tonne.

During the period the group continued to focus on cost control and operational efficiencies. The progress in controlling costs has led to a 3% reduction but the plant efficiencies have not met expectations and are reflected in the increase of cost per tonne of concentrate produced. The increase in coasts was largely due to a reduction in the plant mass pull when new reagents, based on the initial metallurgical work undertaken in the prior quarter, were introduced to reduce the zinc levels in the concentrate. The lab scale test work results did not materialise in the plant which reflected directly in the lower than expected average sales price as a result of less copper and higher levels of zinc in the concentrate.

Mining constraints due to the pit configuration resulted in a blend of ore containing higher than normal pyrite levels, which affected the recovery of metal and reduced the mass pull. Improved mine planning has resulted in a more consistent ore feed to the plant. Test work and plant optimisation being carried out has been in progress since May. The prior quarter upgrades in the flotation plant are now being optimised to achieve a steady state production of separate copper and zinc concentrates and the board are confident that this will reflect in increased plant efficiencies and concentrate grades.

At Baita Plai, a prospecting license was granted over the Faneata tailings dam located 7km from the mine. The 4.6MT dam is estimated to contain 4,080 tonnes of copper, 6,640 tonnes of zinc, 3,100 tonnes of lead, 35 tonnes of silver and 309kg of gold in-situ. The group plans to undertake an 825m auger exploration programme to upgrade the dam to a JORC compliant mineral resource and thereafter undertake a feasibility study to assess the viability of the resource. The drilling programme is expected to take up to eight weeks to complete and the initial metallurgical test work is expected to take up to 12 weeks. The estimated timeframe from initial drilling to first production is estimated to be 6 to 9 months but the programme has been delayed due to funding constraints and is expected to commence when the MPM revenue stream is achieved.

The BPPM license process is still ongoing. All the legal work to facilitate the merger of Mineral Mining and AFCRR has been completed and the company continues to engage with the relevant authorities. Prior to starting production at BPPM the group will undertake metallurgical test work on the MPPM ore to optimise the plant configuration. During this time the underground mining plan will be optimised.

After the period-end, the group required additional working capital following the termination of the equity subscription agreement with Crede. In July they raised £855K through a placing of 300,000,000 new shares at a price of 0.285p per share. Later in the month they raised $519K through a subscription of 181,992,582 new shares at the same price; and in August they raised £364K through a supplementary placing of 128,035,087 shares. This will provide the board with flexibility and time to review a number of alternate financing scenarios. In late July they repaid the first tranche (50%) of £325K plus interest due to Darwin. Once the BPPM license is received, they will require further funding to bring it into production.

Overall then this is still very mixed. The Pickstone-Peerless gold mine seems to be going very well but the performance at Manaila has been poor as the group continues to struggle to separate the copper concentrate from the zinc concentrate, further constrained by higher pyrite levels. The BPPM license is still not forthcoming and there seems to be little that can be done to expedite the decision. In any case, there is not enough funding in place to develop that mine so it is hard to see how the group can continue without substantial dilution taking place to current shareholders. I am still avoiding this for now.

On the 30th August the group released an update for the Manaila mine. The aim of the test work carried out in the first half of the year was to optimise flotation parameters in order to separate the contained copper and zinc into separate products with minimal cross contamination in the concentrates. The head grade of the composite sample as tested was 1.38% copper, 0.44% lead, 1.17% zinc, 1.08g/t gold and 41.5g/t silver.

The test work confirmed that the current grind size at the plant is optimum at 85% and the results of the flotation tests were: 80.97% recovery of copper in the copper rougher concentrate with a corresponding 23.53% recovery of zinc; 66.87% recovery of zinc in a zinc rougher concentrate with a resultant grade of 14.63% zinc; a theoretical grade recovery curve for copper indicates a 92% recovery at a resultant 20% copper concentrate grade is possible; and a theoretical grade recovery curve for zinc indicates an 85% recovery at a resultant 50% zinc concentrate grade is possible.

Optimisation work began on the MPM plant in May to reconfigure the float lines with the goal of replicating the SGS recovery and grade results achieved at the lab scale and production in the past six weeks has resulted in a copper concentrate with increased copper grades and continued reduction in the zinc grades.

The average concentrate grade in the last quarter was 17.3% copper and 14% zinc; concentrate grades over the past six weeks have seen an increase in copper to 19% but a reduction in the zinc grade to around 4%. The group are now targeting a steady state production in order to maximise sales values within industry standards to reduce tolling charges and penalties. Commissioning has now started on a second float line to produce saleable zinc concentrate with first sales in September.

In parallel to the grade optimisation work, mass pull problems experienced in July have now been rectified through a combination of plant recovery enhancements and new pit designs that include beams and trenches at MPM to reduce the water ingress during periods of higher rainfall resulting in head grade dilution. The Iacobeni plant mass pull has increased from about 1.5% in July to 2.5% in August.

The group has awarded an outsourced mining and transport contract to an independent contractor to mine and transport the ore from the open pit to the flotation plant in Iacobeni. The contract will eliminate the upfront cash requirement thereby reducing working capital constraints, outsource mining fleet maintenance and reduce on site management and overhead costs to improve the profitability of MPM.

On the 6th September the group announced that it has signed a long-term offtake agreement with Transamine Trading, a Swiss-based trader of non-ferrous metals, for all concentrates produced at Manaila. The terms and conditions of the agreement, which is valid until December 2017, dictate the offtake pricing dependent on the quality of concentrate with favourable payment terms to reduce the group’s working capital constraints.

The first concentrate sale under the agreement was in September for 430 tonnes of copper concentrate grading 18.7% copper. The steady state copper concentrate now being achieved after the plant optimisation is grading 20% copper.