32 Red has now released its final results for the year ended 2015.

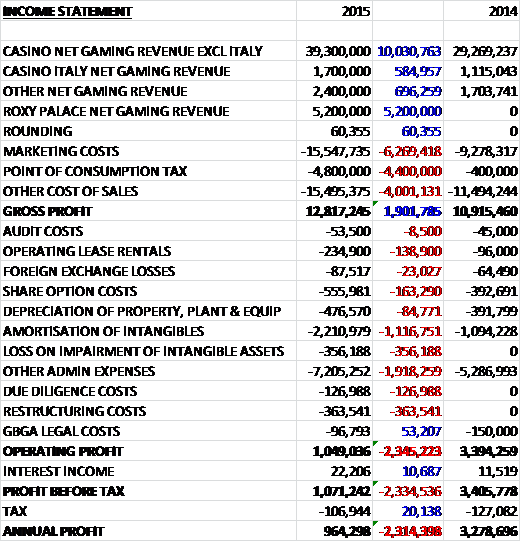

Revenues increased when compared to last year as the underlying casino revenue increased by £10M, Roxy Palace contributed £5.2M, Italian revenue grew by £585K and other gaming revenue increased by £696K. Marketing costs increased by £6.3M, point of consumption tax was up £4.4M and other cost of sales increased by £4M to give a gross profit some £1.9M ahead of 2014. Operating lease rentals increased by £139K as the company moved into larger offices, share options costs grew by £163K, amortisation grew by £1.1M following the acquisition of Roxy Palace, there was a £356K loss on impairments of intangible assets and other underlying admin costs were up £1.9M. We also see £127K of due diligence costs and £364K of restructuring costs and overall, operating profit declined by £2.3M. After a small decline in tax and increase in interest income, the profit for the year came in at £964K, a decline of £2.3M year on year.

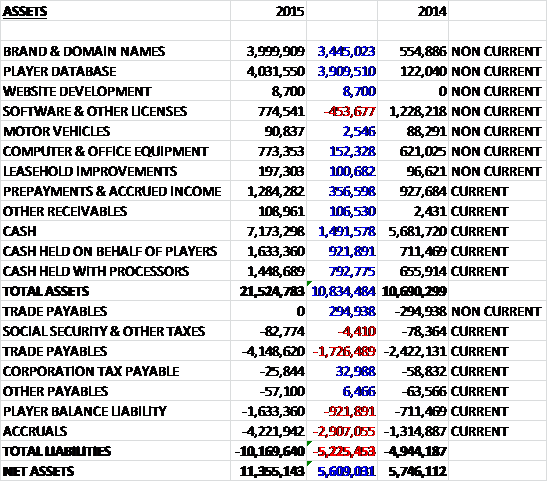

When compared to the end point of last year, total assets increased by £10.8M, driven by a £3.9M growth in player databases, a £3.4M increase in brands and domain names, a £1.5M growth in cash and a £1.7M growth in cash held on behalf of players and held with processors. Total liabilities also increased due to a £2.9M growth in accruals, a £1.7M increase in trade payables and a £922K growth in the player balance liability. The end result is a net asset level of £11.4M, a growth of £5.6M year on year.

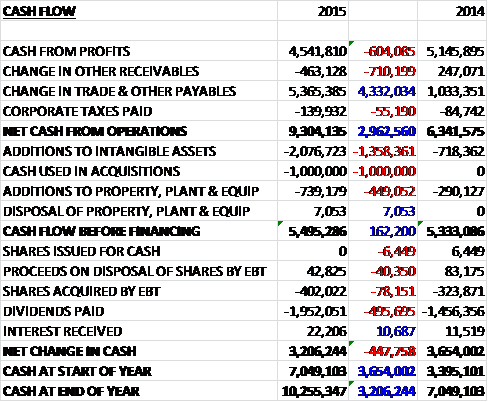

Before movements in working capital, cash profits declined by £604K to £4.5M. There was a strong cash inflow from working capital, with a £5.4M fall in payables, which meant that the net cash from operations came in at £9.3M, a growth of £3M year on year. The group then spent £2.1M on intangible assets, £739K on property, plant and equipment, and £1M on acquisitions to give a free cash flow of £5.5M. We then see £402K spent on shares by the employee share scheme and £2M spent on dividends to give a cash flow of £3.2M for the year and a cash level of £10.3M at the year-end.

The gross profit in the underlying business was £10.9M which was flat year on year with the core Casino brand showing NGR growth of £10M to £39.3M reflecting the effect that the point of consumption tax has had. Throughout the year, marketing expenditure incurred in any one month was paid back within three months in gross gaming revenue derived from new players directly attracted by that month’s marketing spend. Mobile devices remain the fastest growing platform and revenues derived from mobile customers increased by 71% year on year, representing 44% of the total.

Kambi Sports Solutions continues to provide a fully managed sportsbook solution, enabling the group to offer a competitive sports betting product to its customers. The group entered into an agreement with the British Horseracing Authority to become an authorised betting partner in December. They have made voluntary contributions to the Levy since it commenced operations and under this agreement, will continue to make voluntary contributions in respect of all bets placed on UK horseracing. Overall, sports betting revenues continue to grow and focus remains centred on cross-selling the casino products to new sportsbook players.

Poker and Bingo operations continue to benefit from increased investment in the marketing and value of the brand and from increased activity levels at the 32Red casino from which the group can cross-sell and maximise lifetime player value. In all, NGR of other products increased by 42% to £2.4M.

The gross loss in the Italian business was £792K, a detrimental movement of £1.1M when compared to 2014. The board saw opportunities to increase marketing investment in the market in order to further the long term development of the brand in the county which resulted for the loss recorded. NGR increased by 54% to £1.7M and a total of 6,413 new players were recruited, bringing the total number of active players to 12,774. The board expect the Italian operations to break even during 2016 as the brand gains continued traction.

The gross profit in the Roxy Palace business was £1.8M, which was the maiden contribution from the business. The integration of the business was completed ahead of schedule and will deliver material cost synergies in 2016 and beyond. NGR has been in line with expectations during this integration phase and the business will benefit from increases and more efficient marketing in the year ahead.

The company is focused on growing its established brands in the core UK market, where they continue to see significant growth potential. They will do this through developing return on investment driven marketing campaigns that deliver value for the business. Following the introduction of new regulatory and licensing regimes in the UK, NGR derived from the UK was subject to a new 15% point of consumption tax from the start of December 2014, resulting in a change in the dynamics in the UK market. Smaller operations have withdrawn from the UK and some larger operators have chosen to reduce their marketing expenditure which enables the group to grow its market share by accelerating marketing investment.

The marketing expenditure in the core UK market will continue to be supplemented by controlled investment in Italy where the group is establishing the brand to deliver on the long term potential seen in the country. Furthermore, the global online gaming regulatory landscape continues to evolve and the board is apparently encouraged by developments in potential new markets.

During the year the company moved to larger offices in Gibraltar and entered into a new ten year contract to lease the premises with the same landlord as the smaller office. The rent at the new office is subject to annual escalation clauses based on annual rent reviews and at the year-end there was a minimum operating lease payment of £2.4M over the term.

In July the group acquired Roxy Palace Casino for total consideration of £8.4M comprising £2M in cash and the issuance of 10,000,000 new shares with £1M of the cash consideration deferred into 2016. No goodwill was generated but there were £8.4M of intangible assets acquired and during the year, Roxy contributed NGR of £5.2M. The business has 230,000 registered players and was founded in 2002.

The group is somewhat susceptible to exchange rate changes with a 15% strengthening of Sterling against all other currencies giving rise to a loss of £337K over the year.

Trading so far in 2016 has been very strong across the portfolio with like for like NGR for the first nine weeks of the year up 35%, and up 66% including the contribution from Roxy Palace.

The board remains committed to delivering strong growth, both organically and via acquisitions, and as the landscape continues to evolve, they remain encouraged by regulatory developments in new European markets. They are confident that 2016 will be another year of strong organic growth as they continue to increase marketing investment in both 32Red and Roxy Palace brands.

At the current share price the share trade on a massive PE ratio of 132 but this falls to a much more reasonable 13.3 on next year’s consensus forecast. After the announcement of the special dividend and a 17% increase in the underlying dividend, the shares are currently yielding 3.8% which is predicted to fall to 2.8% on next year’s forecast.

Overall then, this was a bit of a mixed set of results with a very strong underlying performance offset with the effects of the point of consumption tax. Profit declined due to the tax and a higher level of amortisation following the acquisition – underlying profit was up. Net assets grew year on year and operating cash flow improved which generated copious amounts of free cash – this was due to an increase in payables, however, and cash profits declined year on year.

The Italian business showed a loss due to a step-up in investment but the Roxy Palace acquisition contributed well. The new year has started strongly and the forward PE is forecast to be 13.3 with a 2.8% dividend yield. The shares are not obviously cheap and the point of consumption tax is obviously having an effect. This is a rapidly growing company, however, and this year’s comparison will include the tax. I sold out just before the results to conserve the big profits made here but I am tempted to jump back in again for the ride.

On the 18th March the group announced that Operations Director Patrick Harrison sold 296,125 shares at a value of £444K. Following the disposal he owns 550,000 shares so this is quite a hefty sale.

On the 13th May the group announced a three year sponsorship agreement with Leeds United but more importantly they stated that trading remained very strong. Like for like net gaming revenues for the first nineteen months of the year were up 39% on the same period of the prior year and increased by 71% including the contribution from Roxy Palace. The board remain confident of delivering their expectations for the year as a whole.

On the 29th July the group released a trading update covering the first half of the year. NGR was up 63% to £30.4M, driven by a combination of strong organic growth (up 32%) reflecting the growing market investment, and an increasing contribution from the Roxy Palace business.

Casino NGR was up 24% to £21.2M and other products were up 223% to £2.3M. Roxy Palace contributed NGR of £5.8M which was in line with management expectations and the Italian NGR were up 33% to £1.1M, again in line with board expectations as the company continues to examine ways to broaden its product offering in this competitive market.

Strong trading momentum has continued since the period-end with the number of like for like active users in July up 21%. Like for like wagering levels are up by 33% but an unusually weak casino gross win margin resulted in NGR being slightly behind, down 2% on a strong July 2015 comparative. Trading as a whole remains in line with full year expectations.