Havelock Europa has now released its prelim results for the year ended 2015.

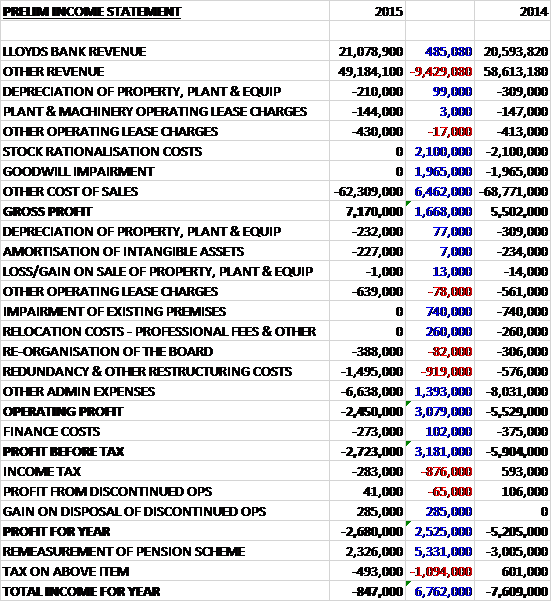

Overall revenues declined by £9M when compared to last year, mostly as a result of reduced UK retail activity (M&S?) and delayed public sector contracts, but underlying cost of sales fell by £6.5M and there was no stock rationalisation cost which was £2.1M last year and no goodwill impairment which accounted for £2M which meant that the gross profit increased by £1.7M. A decline in depreciation was offset by an increase in operating lease charges and a £919K growth in restructuring costs along with an £82K increase in the board reorganisation costs was offset by the lack of premises impairments and relocation costs that occurred last year. Other admin expenses were down £1.4M, however, so the operating loss fell by £3.1M when compared to 2014. Finance costs declined but tax costs increased by £876K as the group stopped recognising further deferred tax losses incurred during the year, and despite a £285K gain from the disposal of the discontinued operation, the loss for the year came in at £2.7M, an improvement of £2.5M year on year.

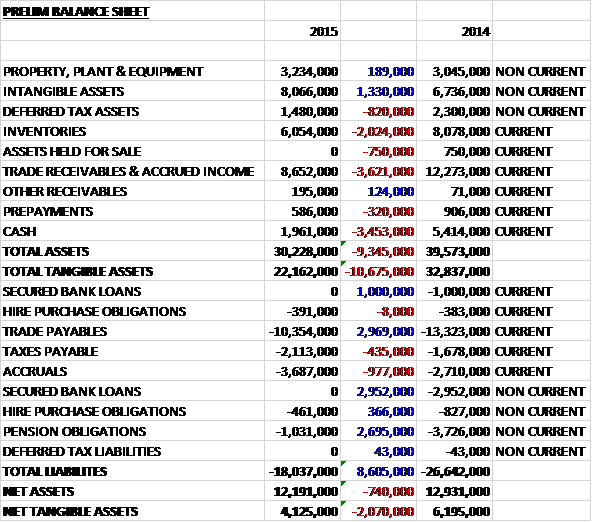

When compared to the end point of last year, total assets declined by £9.3M driven by a £3.5M fall in cash, a £3.6M decrease in trade receivables and a £2M decline in inventories, partially offset by a £1.3M growth in intangible assets. Total liabilities also declined during the year due to a £3M fall in trade payables, a £4M decrease in bank loans and a £2.7M decline in pension obligations due to an increase in corporate bond rates. The end result is a net tangible asset level of £4.1M, a decline of £2.1M year on year.

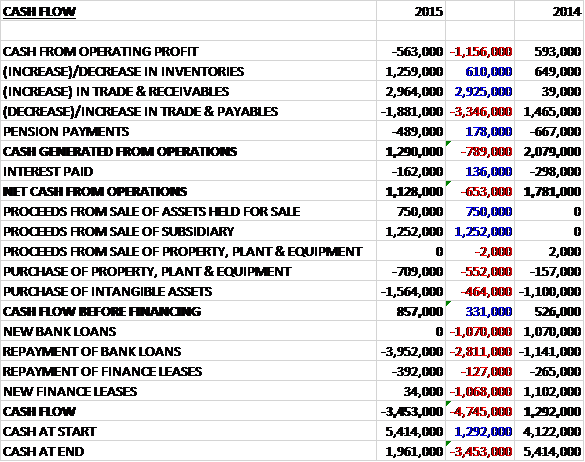

Before movements in working capital, the group swung by £1.2M to a cash loss of £563K. There was a cash inflow from working capital, mainly as a result of a decrease in receivables and inventories and after interest costs fell by £136K there was a net cash inflow from operations of £1.1M, a decline of £653K year on year. This did not cover the £1.6M spent on intangibles relating to the new ERP system, but there was a net £41K cash inflow from asset sales as the group sold its Dalgety Bay site, and an income of £1.3M from the sale of the subsidiary so before financing there was a cash inflow of £857K. Of this, £392K was spent on finance lease payments and £4M of loans were paid back to give a cash outflow of the year of £3.5M and a cash level of £2M at the year-end.

In September the group announced the simplification of the business model and the rightsizing of the business which led to a 10% reduction in staff numbers. The announcement by Lloyds in November that they will reduce activity in 2016 led to an intensification of this process which was completed by the end of the year. The business is now organised into three divisions – Retail and Lifestyle; Corporate Services, which comprises mainly the financial services sector; and Public Sector which includes education and healthcare.

Within Retail and Lifestyle the group is having some success in winning new clients and whilst current volumes are low, the full benefits of these new customers will accrue as the relationships begin to mature. Corporate Services is currently the smallest of the segments but the group are developing a number of opportunities and expect to make progress during the year. Public Sector is currently the largest segment and includes healthcare, education and student accommodation.

During the year the group developed a number of new UK retail customers and they look to turn these relationships into significant accounts over the next few years. The impact of these customers was not enough to negate the reduction of work from M&S, however, so UK retail sales in the period were responsible for the reduction in total sales. International retail sales had a good year and now make up more than 15% of the total.

Due to a strong second half of the year, corporate services had a decent year with both sales and margin above target but this good work was undone when Lloyds announced they will be substantially reducing their spend on refurbishment for the foreseeable future. The board continue to target opportunities for both furniture and fit out sales in this market, however, and are pursuing a number of prospects.

Although public sector sales improved in the year, the scale of the increase and the margins achieved were disappointing. Action has been taken to address these issues as part of the restructuring plan and education now forms and integral element of the division. The business will be focused on securing work from those markets where the final customer is government funded.

The restructuring of the business interrupted the development and implementation of the ERP system which will result in an increased cost of delivery but the board expect to start operating aspects of the system from June. The relocation of the head office from Dalgety Bay to a new facility close to the factory in Kirkcaldy was completed in May. The move is cost neutral to the business but the facility has become a showcase for their office fit out capabilities which is a market they intend to target more intensively.

Interestingly the group mention that sales to Lloyds Bank made up 30% of revenues this year and after sales to M&S represented 14% of revenues last year, they have now disappeared. This shows quite how susceptible they are to two large clients but the board is trying hard to make sure that no one customer makes up more than 10% of sales (this is likely to come from reductions from the large clients though!)

In September the group sold Teacherboards to Sundeala for a modest profit which gave rise to a gain on disposal of £285K. Unlike the main business, Teacherboards is actually slightly profit making, with a profit of £41K this year but the disposal signals the group’s exit from the educational supplies market. I suppose the group needed the £1.3M cash injection which gave rise to a net cash position at the year-end of £1.1M, an increase from the £200K recorded at the end of last year.

David Ritchie was appointed as the new CEO in May, replacing Eric Prescott. Due to overseas commitments, Andrew Burgess, the largest shareholder, resigned from the board in June and was succeeded by Peter Dillon who lasted less than three months before resigning himself! From April, the Chairman is deferring £25K of his salary and the other non-executive directors are deferring £5K of their salaries until the company returns to profit which is a nice gesture.

The order book for current year delivery of £25M was an increase of 25% year on year and current trading is in line with market expectations, which the board believes will continue for the first half of the year. The group retains a high dependence on second half orders, however, which restricts their visibility for the full year outturn but the board are cautiously optimistic for the year as a whole.

As the group is loss making, any PE ratio comparisons for this year are meaningless but next year they are expected to turn a modest profit which would give a forward PE of 31.9 which seems rather expensive. No dividend was paid, nor is one expected in the immediate future.

Overall then, this is clearly a business that is struggling. The losses did improve but this was only due to no goodwill impairments or stock rationalisation costs that occurred last time and underlying losses deteriorated. Net assets also fell and the operating cash flow declined too. Indeed, it was only a favourable movement in working capital that gave a positive cash flow as the group incurred cash losses this year.

There are some new clients but volumes seem low and they were not enough to replace the loss of M&S and with Lloyd’s announcement they are cutting back on refurbs, the corporate services division is also struggling. The new ERP system looks really expensive and I am not sure whether the group can really afford it. Although the order book is up, the group are reliant on second half orders to hit targets and with a forward PE of 31.9 this doesn’t seem close to covering the risk so I am not interested at these levels.

On the 29th April the group announced the appointment of Hew Balfour as a non-executive director. He replaces Alastair Kerr who joined the board in 2012 and will stand down at the AGM. Hew is not new to the company, he was CEO from 1989 until 2010 and is currently chairman of Ebico Trading. This is an interesting development, although I am not sure it is a positive one.

On the 10th June the group announced a trading update. The restructuring of the business is making a positive contribution but has impacted on the development of the new ERP system which has taken longer than originally planned. Nevertheless, the group have implemented the first module of the system and now expect to complete the full implementation of the system during Q4 2016.

The board expects the first half performance to remain in line with their expectations but the business continues to have a high dependency on second half orders and whilst the public sector is performing well, visibility in the retail and leisure sector is less clear. This situation makes predictions for the second half difficult but the board currently believes that performance for the full year will also remain in line with their expectation.

In addition, the chairman has given his notice to stand down after being in the role for four years.

On the 14th June the group announced that Andrew Burgess sold 100,000 shares at a value of £13K. This may not seem like much but given he still owns 6,904,785 shares this is a significant development.