Telecom Plus has now released its final results for the year ended 2016.

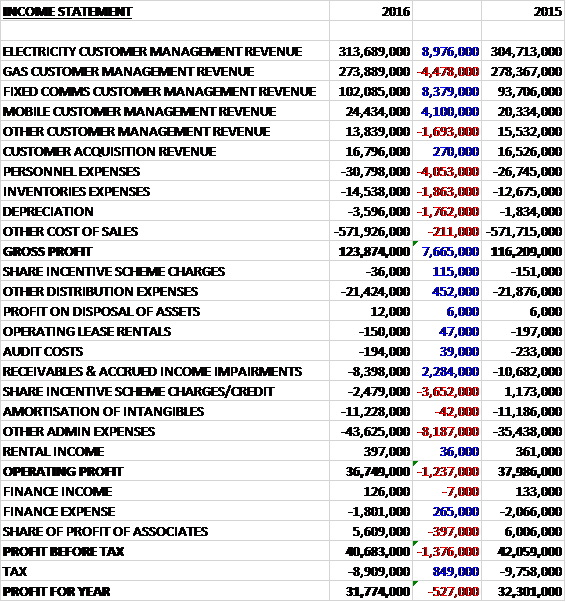

Revenues increased when compared to last year as a £4.5M decline in gas revenue and a £1.7M fall in other customer management revenue was more than offset by a £9M growth in electricity revenue, an £8.4M increase in fixed communications revenue and a £4.1M growth in mobile revenue. Personnel expenses were up £4.1M following the move into larger offices, inventory expenses increased by £1.9M and depreciation grew by £1.8M to give a gross profit £7.7M above that of 2015. Distribution expenses fell by £567K reflecting lower promotional costs associated with gathering new members and accrued income impairments were down £2.3M but there was a £3.7M negative swing on the share incentive scheme charge due to the increase in the share price, and other admin expenses were up some £8.2M, again mainly due to the move to the larger office, to give an operating profit £1.2M below that of last year. There was a small reduction in finance expenses and an £849K decline in tax costs but the share of profit from the associate was £397K lower which meant that the profit for the year came in at £31.8M, a decline of £527K year on year.

When compared to the end point of last year, total assets increased by £2.5M driven by an £11.5M growth in freehold land and buildings, a £9.2M increase in investment properties relating to the old HQ, an £18.8M increase in cash, a £1.9M growth in inventories and a £1.6M increase in fixtures & fittings, partially offset by a £22.7M decline in assets under construction as the new head office was completed, an £11.2M decrease in the energy agreement intangible asset and a £7.5M fall in accrued income. Total liabilities also grew during the year due to a £1.1M increase in borrowings and a £1.7M growth in other taxes and social security payables (although note the £21.5M of deferred consideration became current). The end result was a net tangible asset level of -£3.8M, a positive movement of £13.2M year on year.

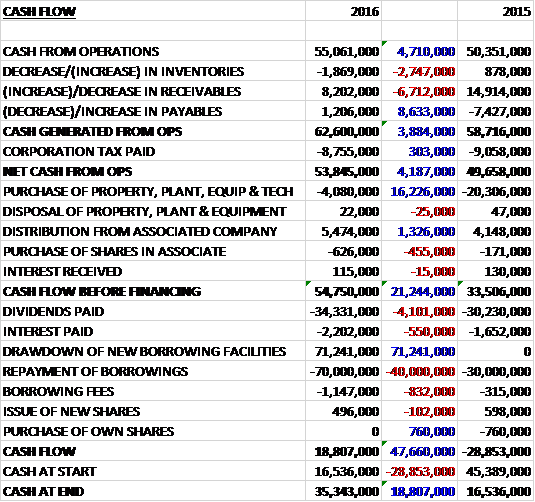

Before movements in working capital, cash profits increased by £4.7M to £55.1M. There was a cash inflow from working capital due to a fall in receivables, but this was less than last year and after tax payments fell by £303K, the net cash from operations came in at £53.8M, a growth of £4.2M year on year. The group spent £4.1M on property, plant and equipment but this was covered by the £5.5M in dividends received from the associate to give a free cash flow of £54.8M. Of this, £2.2M was spent on interest payments and £34.3M went on dividends to give a cash flow for the year of £18.8M and a cash level of £35.3M at the year-end.

During the year he group has seen a slowdown in the growth rate in service numbers that they have achieved historically. The principal factors behind this are the material fall in wholesale energy commodity prices over the last 30 months which has created a significant gap between the standard variable tariffs paid by most customers and the short-term fixed price deals offered by the group’s competitors to customers who switch, and the decision they took in March 2015 to stop offering introductory deals to new members in favour of an everyday low pricing approach.

Against this background, there has still been an increase in the number of services the group have provided, increasing by 88,000 to 2,181,704. Within this total the number of residential members now taking all five core services have increased from 58,753 to 76,765. This have been driven by the decision to re-invest the money the group were spending on introductory offers into making the “Double Gold” bundle even more attractive which the board expect to lead to lower churn and higher customer satisfaction.

Revenue growth was adversely affected by a fall in average energy consumption within the domestic membership base compared with the prior year, reflecting the impact of the energy efficiency measures that have been delivered by the industry over the last few years which was exacerbated by lower average energy prices during the year following the price reductions the group implemented in early 2015.

The group’s customer churn has risen as a result of the attractive introductory deals being offered by other suppliers, although it remains below the industry average. All core services provided saw growth with the highlight being a 17% rise in the number of mobile services which means that penetration of mobile within the services offered has now reached nearly 30%, a level of growth that should continue given the fact that management released new price plans in January of this year.

Last Autumn the group announced the nationwide rollout of Project Daffodil, their free LED light bulb replacement service which is only available to members who have switched all their utilities to Telecom Plus. This scheme is expected to reduce their electricity bills by about 11% and goes a long way towards narrowing the gap between their energy prices and the introductory tariffs available elsewhere for potential new members and has resulted in a significant improvement in the quality of new members joining as well as an increase in the number of existing members who are adding additional services in order to take advantage of the benefit. The installations started in January this year and as the cost of installation is expenses at the time it takes place, these expenses are expected to increase in the coming year.

As far as mobile is concerned, the group apparently retain a good working relationship with EE following their recent acquisition by BT, and they have recently extended their MVNO agreement with them on improved commercial terms which includes then giving the group access to their 4G network later in the year.

Earlier in the year the government announced that they are committed to deregulating the domestic water supply market before the end of the current parliament. This potentially creates a new opportunity for the group to add the supply of water to their existing range of utilities offered. The board also believe that there is an opportunity to offer a range of insurance products where the cost of the policies can be paid to them monthly alongside the other services they offer. They intend to start with home insurance later in the year with a view to expanding the range in due course to include motor, pet and travel cover.

The group have trialled a number of direct marketing campaigns to existing members to encourage them to take additional services, using the opportunity of receiving free LED bulbs to induce them to do so. They are planning to roll this out to a wider cross section of their existing membership base over the coming months, as well as targeting former members as part of a win-back campaign. They are also looking to invest in their IT system which will incur meaningful costs but in the longer term should improve efficiency.

The group’s share of profits from Opus Energy fell by £400K to £5.6M. This performance, during a year in which it achieved further significant growth in customer numbers and gained market share, was broadly in line with expectations and reflects the impact of the removal last summer of the exemption from the Climate Change Levy for business customers supplied with European power.

The group still has a good reputation with customers and was ranked second in the UK customer satisfaction index with none of the other utility and telecoms providers making it into the top 30.

The board are concerned about the high and increasing costs imposed on the industry in order to comply with government policy, much of which seems to be imposed with inadequate thought given to delivering initiatives in a way that will minimise costs, which ultimately get passed on to customers. Examples include the current faster switching initiative, the establishment of Smart Energy GB, the structure of the smart meter roll out programme, the over engineering of the specification for the DCC and the unrealistic time frames which are adopted for any industry change.

The group have appointed Beatrice Holland as a new independent non-executive director. She is a member of the board of Brown Advisory, a non-executive director of M&G and chairman at Millbank Investment Managers. Michael Paiva will be retiring at the forthcoming AGM having completed nine years as an independent non-executive director.

So far this year, the board are seeing a significant improvement in the quality of new members and are running slightly ahead of the level achieved in the previous quarter in relation to quantity. The proportion of new customers being signed up who take the Double Gold bundle is now running at around 55% compared to 34% immediately before Project Daffodil was announced.

The current adverse market conditions will not persist indefinitely and the board are confident that when the recent downward trend in wholesale commodity prices reverses, their growth rate will start returning towards the higher levels they have historically achieved. In the meantime they expect to continue to deliver further modest growth for the current year with the adjusted pre-tax profits being between £55M and £59M.

At the year-end the group had a net debt position of £56.3M compared to £74M last year and includes the £21.5M payable to N Power in December. At the current share price the shares trade on a PE ratio of 25.2 which falls to 16.5 on next year’s consensus forecast. After a 15% increase in the full year dividend the shares are trading on a yield of 4.6% which increases to 5% on next year’s forecast.

Overall then this has been a bit of a sluggish year for the group but one of progress nonetheless. Profits were down, although this was due to the higher share price giving rise to higher costs associated with the share incentive scheme and ignoring this, profits were modestly up. The net tangible asset base also improved, although it did remain negative and the operating cash flow increased with plenty of free cash being generated.

There was a slowdown in the growth rates of services provided and energy consumption declined but the introduction of the free LED scheme led to a significant increase in the number of members taking all services. The Opus associate ran into difficulty after the removal of exemption from the climate change levy for its customers but it is still profitable and growing market shares. The introduction of insurance looks interesting and the board are expecting modest growth this year.

Despite the decent 5% forward yield, the forward PE ratio of 16.5 looks as though it prices quite a bit of growth in already, however, and I am not rushing to own the shares quite yet.