International Greetings have now released their final results for the year ended 2016.

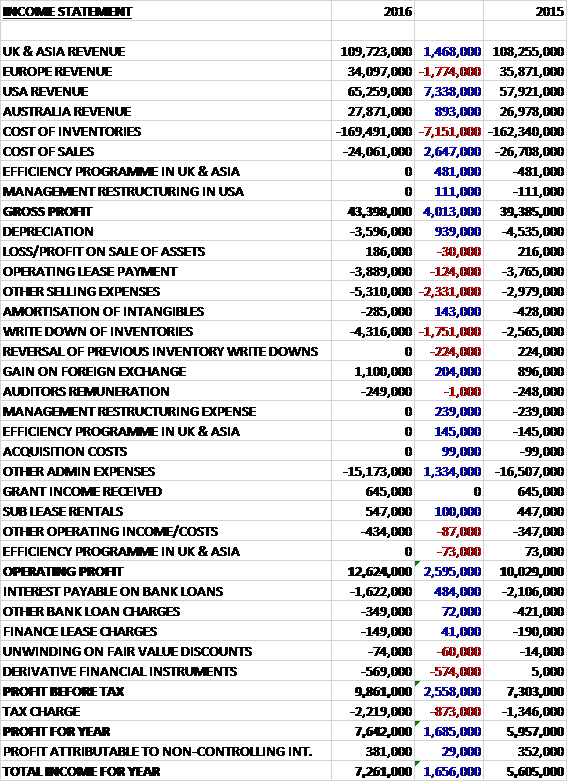

Revenue increased when compared to 2015 as a £1.8M decline in European revenue reflecting euro weakness was more than offset by a £7.3M growth in US revenue, a £1.5M increase in UK & Asian revenue and an £893K growth in Australia revenue. Cost of inventories grew by £7.2M but other cost of sales were down £2.6M and after the £592K of one-off charges weren’t repeated this year, gross profit increased by £4M. Depreciation was down £939K but other selling expenses increased by £2.3M. We then see a £1.8M increase in the write-down of inventories, the lack of a few other non-underlying costs and a £1.3M fall in other admin expenses to give an operating profit £2.6M above that of last year. The interest payable on bank loans fell by £484K but this was offset by a £574K negative swing on hedging instruments that did not qualify to be hedge accounted, mainly in Australia, and after the tax charge increased by £873K the profit for the year came in at £7.3M, a growth of £1.7M year on year.

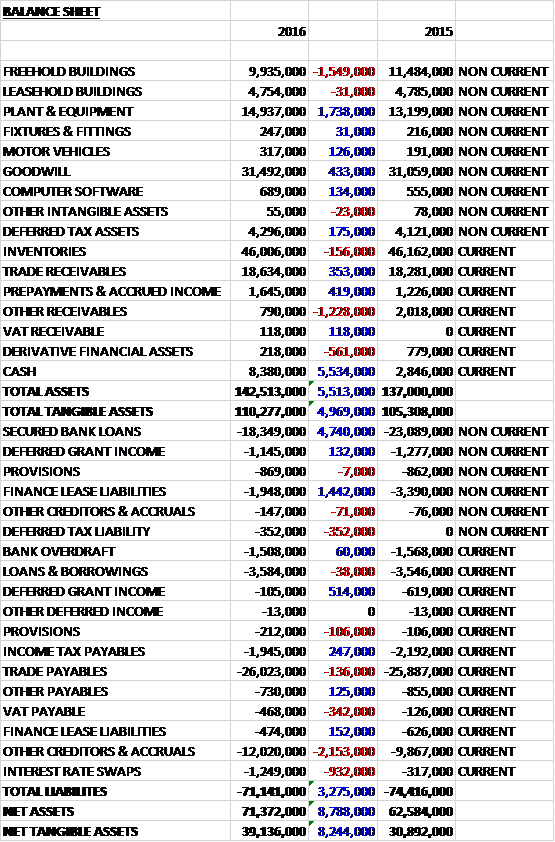

When compared to the end point of last year, total assets increased by £5.5M driven by a £5.5M growth in cash and a £1.7M increase in plant and equipment, partially offset by a £1.2M decline in other receivables and a £1.5M fall in the value of freehold buildings. Total liabilities declined during the year as a £4.7M fall in secured bank loans and a £1.5M decrease in finance lease liabilities was partially offset by a £2.2M growth in other payables and accruals. The end result is a net tangible asset level of £39.1M, an increase of £8.2M year on year.

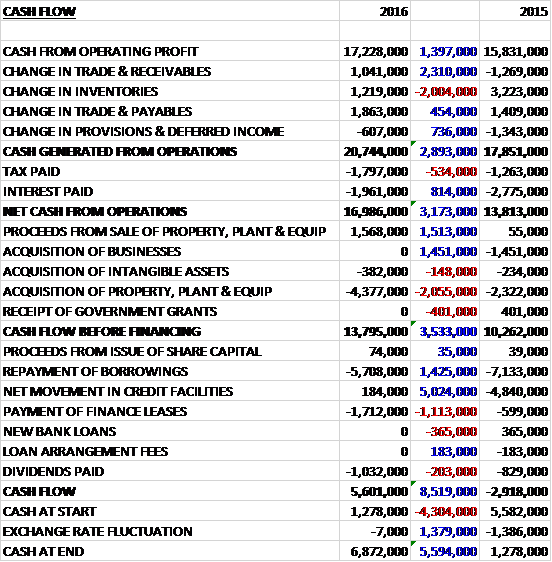

Before movements in working capital, cash profits increased by £1.4M to £17.2M. There was a cash inflow from working capital and after a higher tax payment was more than offset by a lower interest payment, the net cash from operations came in at £17M, a growth of £3.2M year on year. The group spent £4.4M on tangible fixed assets and £382K on intangibles but received £1.6M from the sale of property in Wales to give a free cash flow of £13.8M. Of this, £5.7M was used to repay borrowings, £1.7M was used in the payment of finance leases and £1M was spent on dividends which meant that the cash flow for the year was £5.6M and the cash level at the year-end was £6.9M.

The profit in the UK and Asia business was £5.7M, a growth of £1.2M year on year with the Star Wars range of gift packaging and stationary products proving highly successful. Additionally they achieved record sales of the Tom Smith branded range of gift packaging and greetings products. The group have exceeded efficiency levels targeted as a result of their major programme of investment in gift wrap manufacturing and now will enhance their capability even further with new added features to their facilities, ensuring that they remain market leading in all aspects of their operation.

The year ended with the completion of the sale of a property in Wales which they vacated having installed their new printing presses at a different plant in Ystrad Mynach. Whilst the group’s share of the UK market for gift packaging remains substantial, there is still scope for profitable growth, across this and other categories – both online and through bricks and mortar retailers such as garden centres, and card shops, as well as through a broad network of independent stores.

An enlarged customer base includes a broader presence in the discount sector and the Chinese factory saw record levels of cracker manufacturing with over 72M crackers produced on time in full. In all, Celebrations activity grew strongly but Stationary and Creative Play sales fell back.

The profit in the Europe business was £2.9M, a decline of £290K when compared to last year reflecting the headwinds of imports from China into Europe as a result of adverse forex rates during the year. The group did see sales into Poland and Slovakia grow in double digits as their Western European retail customers expanded into Eastern Europe.

The profit in the US business was £3.5M, an increase of £1.4M when compared to 2015 reflecting the completion of the new installed wrap converting facilities and an outperformance against each and every metric that was set with sales growth achieved across all channels following the appointment of a new leadership team. The business has established some significant new customers and product launches as well as activity in new territories across the broader Americas, reflected in the launch of Spanish language greeting cards to satisfy the demands of Spanish speaking citizens in the US. The business also launched “Kids Create” branded products in the region.

The profit in the Australia business was £1.5M, a growth of £402K year on year despite the slowdown of the Australian economy, reflecting a very effective outcome to the operational initiatives put in place last year. Despite an overall flat market, they achieved 17% sales growth in local currency and all product categories saw an increase in market share. Partyware sales were especially buoyant and top line growth was supported by an excellent performance in order fulfilment, the outcome being that the business returned to growth in profits after a challenging few years.

Recent years of significant investment in wrap manufacturing together with semi-automated cracker manufacturing have underpinned the group’s position as the world’s largest producers of both products. Crackers have traditionally been a Christmas focused category but everyday and special occasion crackers are now sold to over twenty countries with their strategy being for crackers to become an all year round table decoration.

In gifting, recent highlights have included the Rosie’s Pantry collection and sales of designed themed related collections have also included photo related gifts such as over 9M gift themed photo frames being sold in Europe.

Licensed products feature strongly within the Stationary and Creative Play category with stickers being hugely popular with 750 million being sold in the year. Longstanding licensor relationships include those with Disney, Marvel, Universal and Entertainment One spanning products such as Star Wars, Spiderman, Minions and Peppa Pig.

The group has been successful in maintaining or increasing margins. In Europe, the 10% operating margin was sustained; margins in the US were up 1.3% to 6.3%; Australia increased by 1.6% to 5.4% and the full year effect of the investment in Wales lifted margins in the UK by 0.6% to 6.7%. The group aims to further improve margins by increasing the balance of own brand products and non-Christmas business but efficiencies in sourcing and manufacturing are also continuing to contribute materially.

Another important dynamic to margin continues to be the level of FOB business delivered directly to major customers at ports in China. This type of business continues to grow in all territories especially in the US with the major value chains. This typically attracts lower gross margins but it is a means of retaining or winning large volumes of business in a manner that avoids other costs and risks associated with domestic delivery so winning this business can enhance net margins and return on capital even as gross margins are diluted.

Overheads have increased slightly reflecting mainly investment in the US business and other capability to allow the group to grow but costs remained largely steady as a percentage of sales.

The greatest opportunity for further investment is in the US where the group have now invested in a Casepacker and a high efficiency gift converting line. The business case for the final phase to update the printing capability in the country is now under way. Other modest but still seven figure organic capital investment opportunities are now arising, offering the opportunity to expand into new product categories and customer channels.

At the end of the year, the group completed the sale of the Aberbargoed site for £1.4M, just over book value. They are now in the fourth year of a five year period by which a company has the option to purchase part of another under-utilised site (with a net book value of £800K) for £2.4M. The building is also generating an income of £100K per annum, recognised under other operating income.

The group does seem somewhat susceptible to forex movement. The relative strength of the US dollar against other currencies can materially impact purchase prices out of China. This is most noticeable in the weakness of the euro and Australian dollar and the businesses in these regions are finding their margins are being squeezed through forex headwinds on products bought in from the Far East. Balanced against this, the renminbi weakened against the US dollar so it has been possible to negotiate lower prices to mitigate the effect in part.

Whilst it is too early to know the full long term impacts of the UK’s exit from the EU, the board feels that their diversified global portfolio mean they are well positioned to manage the effects and the outcome in itself results in no material change in outlook for the group’s near term financial results – if it happens to trigger a global recession of course things would be different. The main impact would be from forex movements. Weaker sterling against the dollar would make goods imported from China more expensive but the group are well hedged going into next year. On the other hand, earnings from the US business would be translated at more favourable rates.

At the year-end the group had a net debt position of £17.5M, a big improvement on the £29.4M at the end of last year and year-end leverage reduced to 1x this year (of course leverage is greater during the course of the year with average leverage in 2016 being 3.2x compared to a target of 2.5x). At the current share price the shares trade on a PE ratio of 13.3 which falls to 11.2 on next year’s consensus forecast. After a 150% increase in the dividend, the shares are yielding 1.6% which increases to 2.1% on next year’s forecast.

Overall then this has been a good year for the group. Profits increased when compared to last year, net assets were up, and the operating cash flow grew, generating a decent amount of free cash. The UK business saw profits grow, reflecting a strong celebrations product market; the US business performed very well following new market and investment in the machinery, and the Australian business also returned to growth despite a flat market. The only downside was the European business which suffered due to cheap Chinese imports following forex movements.

The group is a market leader in many products and is doubtless an efficient outfit with growing margins but it is hard to see where much growth will come from. I am not convinced that crackers will become ubiquitous all year round for example. The dollar strength following the Brexit vote is not good for the company but a forward PE ratio of 11.2 seems to price this in. The yield of 2.1% is decent enough and growing and I remain a holder for now.

On the 11th July the group announced the acquisition of Lang Companies Inc, a supplier of branded consumer indoor and outdoor home décor and lifestyle products bases in the US. The acquisition was satisfied by a net cash consideration of $3.6M but the business incurred a pre-tax loss of $2M last year and had net liabilities of $14.9M. The group will not acquire the historical debt structure and the business will be delivered at closing with net working capital of $8.3M. This seems unnecessarily complicated to me – why is no goodwill figure given? What will be the net asset/liability level when acquired? How much net debt is actually being acquired? I can help but think that this is purposefully opaque.

Lang’s products include giftware and calendars with licenses such as NBA and NFL. It has live trading relationships with many US-based national chains and in excess of 3,000 gift stores. Additionally it has established a direct to consumer sales channel through its own website and catalogues with over 150,000 direct customers.

On the 25th July the group announced that it had raised £5.25M by way of placing of 3M shares at a price of £1.75 per share. The proceeds will be used to satisfy working capital requirements for the recent acquisition and support a capital investment project to build the group’s capabilities in the UK to manufacture retail bags not for resale. The group’s outlook remains unchanged but the dilution from the placing offset the expected profit from the Lang acquisition so the EPS outlook remains unchanged.

The placing represented a discount of nearly 5% and the new shares represent just over 5% of the total voting rights.

The group have approved a capital project in the UK to manufacture retail bags not for resale. The project is backed by a commercial agreement with an existing partner already operating in the retail collateral domain. I must admit I am a little confused about this!

On the 28th July it was announced that non-executive director Elaine Bond purchased 15,816 shares at a value of £30K. This represents her first share purchase.

On the 30th August the group released a trading update covering Q1 when trading was in line with management expectations with growth across all regions. In the Americas, sales volumes continue to grow, through their broadening product offering ant to their extended customer base. New business includes sales to regional grocery and drug stores in the US. Exports to Mexico are on track to double and exceed $2M during the year.

Operational and commercial integration of the recently acquired Lang Companies is proceeding well with the business performing in line with management expectations. Synergy opportunities have already been identified and should be largely realised ruing 2018. The phased programme of investment in its US-based gift wrap production facilities is already benefiting the group with enhanced levels of production efficiency being achieved.

In Australia, overall the business is trading in line with expectations with growth especially strong in the party ware category. The group has won a major new contract for the supply of everyday greetings cards, with an estimated annual volume of over 10M cards. This contract is over three years and will roll out towards the end of 2016. Following its expansion into party ware, the group has been awarded new licensed categories across all Disney, Marvel and Star Wars franchises. The installation of new order picking facilities in the Melbourne distribution centre has been implemented on budget and enables the business to manage larger volumes within the Australian market.

In the UK growth has been augmented by increased volumes of party ware products, which further enhances the group’s offering. Sales of licensed stationary for the Back to School period include new licenses, such as the highly popular Paw Patrol, Secret Life of Pets and Finding Dory franchises. The continued evolution of the product mix sold to the UK market has been supported by investment in automation in China, enabling the group to further enhance its share in the gift bag and greetings card market.

In the rest of Europe, the group has achieved record sales and production levels of its core gift packaging product categories, across its existing customer base and to new customers. Through its standardisation of its gift wrap manufacturing processes and materials usage, the group is driving efficiencies and synergies through economies of scale and shared best practice. Overall, the order book is at record levels and this update looks pretty good to me. I continue to hold.