Photo-Me has now released their final results for the year ended 2016.

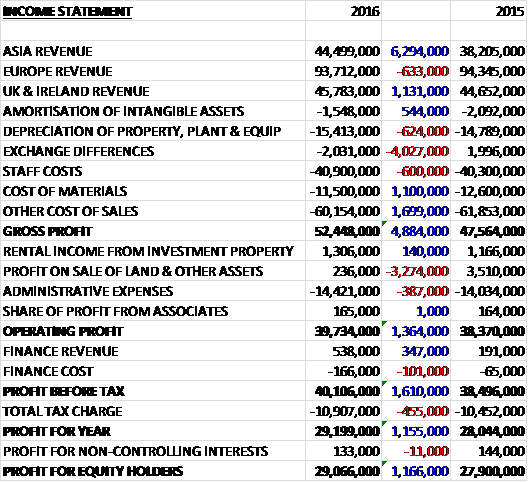

Revenues increased when compared to last year as a £633K decline in European revenue due to euro weakness was more than offset by a £6.3M growth in Asian revenue and a £1.3M increase in UK and Irish revenue. Depreciation was up £624K, staff costs increased by £600K and there was a £4M detrimental movement in exchange differences but amortisation fell by £544K, cost of materials declined by £1.1M due to the winding down of the minilab division and enhanced efficiencies in the supply chain, and other cost of sales fell by £1.7M to give a gross profit £4.9M above that of 2015. There was a £3.3M reduction in the sale of land and other assets and admin expenses were up £387K which meant that the operating profit increased by £1.4M. An increase in finance revenue was more than offset by a £455K increase in tax charges to give a profit for the year of £29.1M, a growth of £1.2M year on year.

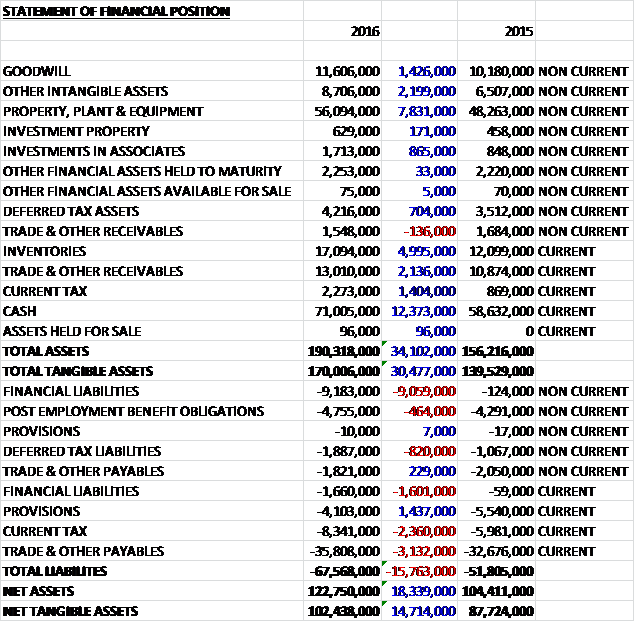

Total assets increased by £34.1M when compared to last year due to a £12.4M increase in cash, a £7.8M growth in property, plant & equipment, a £5M increase in inventories, a £2.2M growth in other intangible assets relating to development costs, a £2.1M increase in trade receivables, a £1.4M growth in current tax assets and a £1.4M increase in goodwill due to the Fowler acquisition. Total liabilities also increased during the year as a £10.7M growth in financial liabilities, a £3.1M increase in payables and a £2.4M growth in current tax liabilities was partially offset by a £1.4M decline in provisions. The end result is a net tangible asset level of £102.4M, an increase of £14.7M year on year.

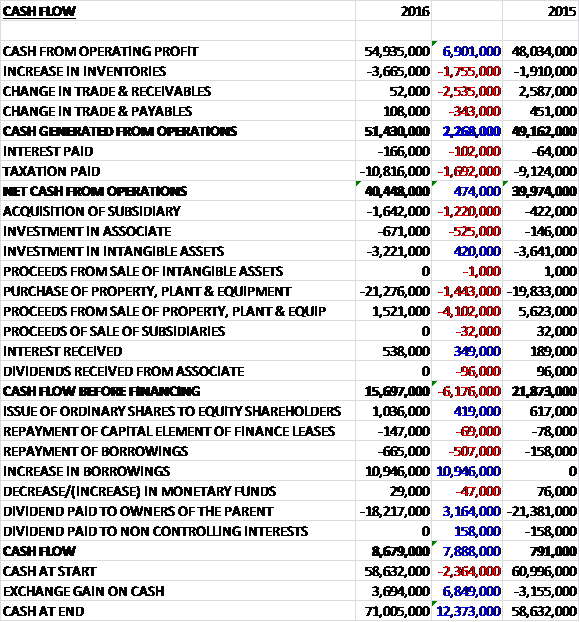

Before movements in working capital, cash profits increased by £6.9M to £54.9M. There was a modest cash outflow from working capital with a growth in inventories and after tax payments increased by £1.7M the net cash from operations came in at £40.4M, a growth of £474K year on year. The group spent £21.3M on property, plant and equipment, £3.2M on intangible assets, £1.6M on acquisitions and £671K on associates to give a free cash flow of £15.7M. We then see £18.2M spent on dividends and a bizarre £11M increase in borrowings, strange when there is so much cash here. The end result is a cash flow of £8.7M and a cash level of £71M at the year-end.

The profit from the Asian business was £10.7M, a growth of £3.7M year on year. The growth in photobooth units was 4.6%, mainly deploying machines in Japan in order to respond to the increased demand created by the roll out of a new photo ID. Performance in Japan has benefited from this ID card regulation which came into force in 2016. Under this system, all Japanese citizens may apply to be issued with their own personal 12 digit number which will in due course require an accompanying photo ID card. The system is not currently compulsory but brings a significant number of admin benefits to both the private user and the public sector and widespread adoption is expected.

Owing to technical and admin problems at local government level the implementation of this plan to date has not gone as smoothly as planned, after a strong start, but the Japanese government is committed to the programme and is increasing financial resource to ensure swifter issuance. Based on the official roadmap issued by the administration, it is expected that by March 2019, 87M cards will be issued while the scope and functionality of the card will be expanded and ultimately it will become the Japanese photo ID card. The speed of issuance will be reliant upon promotion of the scheme by the government but it is likely to lead to a substantial increase in photobooth volumes over the period. Due to the uncertainty over timing, however, the board have not included any profits relating to the card in the forecast for the current year.

In China, gradual progress continues to be made where turnover rose by 24% with a good increase in profitability.

The profit from the Continental European business was £24.2M, an increase of £2.1M when compared to 2015 although revenue was 0.6% lower due to euro weakness (on a constant currency basis it increased by 3.8%). The increase in profit was due to a reduction in siting costs and a focus on operating cost reduction. The European photobooth estate increased by 0.5% with the main areas of growth being France, Germany and Switzerland. The group continues its rollout of higher margin Starck booths and there are now 3,780 deployed across the region. They are assessing price increases and are now running trials in Switzerland and the Netherlands.

The rollout of the Revolution laundry product continues to progress well. The results from the units in operation in France, Ireland and Portugal remain encouraging with takings during the period averaging €1,282 per unit per month. For the full year the turnover of the entire laundry business was £11.8M which has more than trebled since 2014.

The group now has laundry units in twelve countries globally with the most significant coverage being in France, Belgium, Portugal and Ireland. The product has continued to perform well in Portugal and Ireland where an agreement with Tesco Ireland means that the number of operated units in that country should increase to 120 over the next year. The profit in these two countries has climbed rapidly since the units were first introduced and is expected to approach €1M in the coming year. The group continues to target 6,000 laundry units by 2020 as the business grows.

The group has been trialling a number of launderettes in towns across France and Belgium over the past three years. The majority of these have achieved the desired return on capital and the board now considers it appropriate to roll out the concept more aggressively, targeting towns where there is no large supermarket nearby and where competition is limited. The stores are expected to cost around €32K to fully equip and the group’s ambition is to develop this business rapidly.

The group have also announced the development of Revolution 2 which would only have a footprint of 5sqm compared to the 10sqm of existing units. One principal advantage of these smaller units is that they avoid planning restrictions and in addition may be attractive in markets where space is more limited. Production of these units is expected to commence fully in September.

The group continues to operate over 5,000 digital printing kiosks, primarily in France and Switzerland and is currently upgrading the estate to the latest technology to accept all models of memory cards and other media. The new range of Starck designed kiosks are gradually being introduced and good progress is being seen with the Speedlab Cube in particular. The group considers the potential worldwide to be very promising over the medium term.

The group has already introduced biometric standards into a number of its booths in Germany, Switzerland and China and the addition of 3D photo capture would represent a step forward in security. Photobooths are therefore progressively being enabled digitally and in February they announced that they had obtained the first agreement with ANTS in France to allow the delivery of a digitized e-photo and signature for the purposes of driving license application with the document being sent from the photobooths via a secure server. They have some 7,800 units in France and the entire estate will be enabled rapidly. Similarly in September the group signed a five year agreement with Moneygram under which money transfer services would be made available in its booths worldwide, starting in France.

The profit from the UK and Irish business was £8M, a decline of £490K when compared to last year despite a 2.9% growth in photobooth numbers. The market background remained difficult but turnover increased by 2.5% due to the resilience of the photographic business in the UK and the expansion of the laundry business in Ireland. The decline in profits reflected the increase in depreciation and some site costs.

In all, there was a 611 increase in the total number of photobooths and a 1,064 growth in the number of laundry units. The group is looking to enter new markets and positive progress has been made in South Korea where some 100 photobooths have been sited. Small operations have also been launched in Poland.

Over the last few years the group has generally chosen not to raise prices but going forward the increasing introduction of contactless payment across the estate should allow more price flexibility and they are trialling in two countries currently with a planned rollout of price increases over the next two years.

The addition of both smaller Revolutions and the introduction of laundrettes will add to the momentum in that business. Volumes in the photobooth estate have been boosted by the gradual rollout of the new Japanese ID card and new agreements were signed with Moneygram and ANTS which should further enhance returns in the medium term. The development and addition of 3D capability within the booths is promising feature for the medium term. While uncertainties remain, in particular in relation to currency, the board anticipates another year of good growth.

As can be seen the group raised over £10M of long term debt aimed at financing the acquisition of town centre launderettes. Even though the interest rate is low, I really don’t see the logic of having huge cash reserves on the balance sheet and paying out special dividends to shareholders whilst at the same time taking on debt – it seems like madness to me!

At the current share price the shares are trading on a PE ratio of 18.7 which falls to 17.9 on next year’s consensus forecast. Including the special dividend, the shares are yielding 6% which falls to 4.8% on next year’s forecast, which presumably doesn’t include any potential special dividends (the board have indicated that they will increase the dividend by 20% over the next two years). At the end of the year the group had a net cash position of £62.4M compared to £60.7M at the end of last year.

Overall then, this has been another good year of progress for the group. Profits were up, net assets increased and the operating cash flow grew with some decent levels of free cash being generated, although it was not enough to cover the dividends being paid. Asia performed well due to the increase in demand in Japan following the new ID card announcement, although this was lower than expected due to operational issues from the government there. In fact things are so bad, the group is now forecasting no extra profit at all from the venture in 2017.

Europe performed fairly well due to cost reductions but the performance in the UK and Ireland was below that of last year due to site cost increases. Going forward, there seems plenty to stoke growth. The laundry business continues to grow and the deal with Tesco Ireland is a positive. Additionally, the 3D printing and Biometric additions look promising as shown by the deal in France to provide driving licenses. There is very little about the car was venture this time and it seems as though perhaps the trial is not being successful.

The debt drawdown is odd given that surplus cash is being given away to shareholders but with a forward PE of 17.9 and dividend yield of 4.8%, this is looking cheaper than it has done for quite a while and although I no longer view this as the dead cert I once did, I continue to hold.

On the 23rd August the group announced that it had agreed to buy Asda’s Photo Division which is operated in Asda stores in the UK with completion of the acquisition expected to occur at the end of October. The division consists of 191 photo centres, as well as 172 self-service kiosk sites located in Asda stores. These businesses will be managed by the group under a ten year concession with the employees of the business transferring across to the group. Besides the in-store locations, they will also operate the Asda-branded online photo processing offering for a minimum of two and a half years.

The consideration for the acquisition is £3.4M and the group have agreed to buy the inventory available at each photo centre at the date of the acquisition, estimated at £2M with the total consideration being capped at £6M. Under the arrangements, the group will also pay Asda periodic commission payments based on turnover as well as business rates and costs of utilities.

Last year the business made a loss of £3.4M but the board consider that the turnover can be materially raised by having them running the business and they expect that a combination of reconfiguration of layouts, upgrading of equipment and the introduction of innovative designs into sites will add to the appeal for customers and expand the profit performance going forward.

The board expect the acquisition to be slightly dilutive to the earnings of the UK division in the current year but expect it to be earnings enhancing in the medium-term (I would hope so!). They believe that the impact of the dilution in the current year will be offset by favourable currency movements elsewhere in the group and therefore overall expectations remain unchanged.

On the 20th October the group released a trading update covering the first four months of the year. Turnover improved by 18% and pre-tax profits were 14% higher compared to the same period last year, reflecting the investment programme and favourable currency movements. Overall the photo booth and laundry businesses are performing well.

The laundry business saw turnover increase by 192% due to both the increased number of machines and revenue per machine. The group is now accelerating its expansion in the town centres through the roll-out of its new laundry shops concept, in particular France, Belgium and Spain. They also expect the acquisition of the Asda units to be completed around the end of the month.

Cash generation remains strong, trending ahead of last year’s performance and the board remains confident in the business performance for the year.

Overall this all looks very positive and I continue to hold.

Over the past few days CEO Serge Crasnianski purchased 4,827,251 shares at a value of £7.6M! This is a huge purchase and makes me think that something interesting is afoot. He now owns 84,610,701 shares, equivalent to about 22.5% of the total. I am surprised the share price has not moved by more than it has.