Malbourne House, St. George’s street, Douglas, Isle of Man, IM1 1AJ

GVC Holdings provides services to the online gaming and sports betting markets. They are headquartered in the Isle of Man and the group’s activities are licenced in Malta and the Dutch Antillies. Casino Club provides an online casino and poker targeting German speaking customers; Betboo provides sports betting, poker, casino and bingo to customers in Latin America; and the B2B business provides back office services to third party providers.

GVC Holdings have released their results for the full year ending 2012.

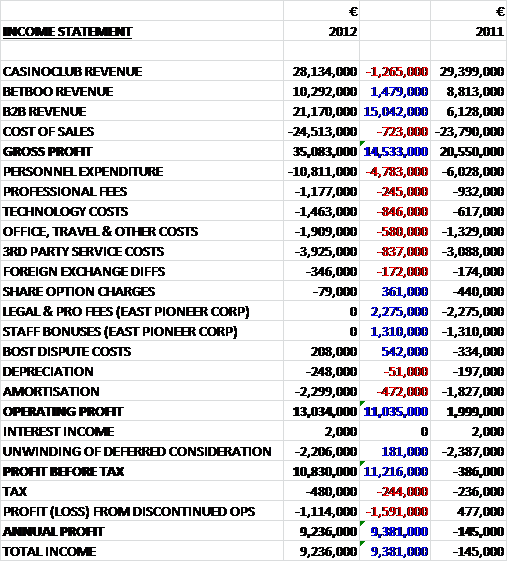

B2B income is the amount receivable for services to other gaming operators and includes the amounts due for the provision of services to East Pioneer Corp. The big change in revenues is the €15M jump in B2B revenue as the first full year of trading took effect but there was also a €1.5M increase in Betboo revenue, mitigated by a €1.3M fall in Casinoclub revenue. The cost of sales only increased marginally to leave Gross profit €14.5M up at €35.1M. The next largest expenditure, personnel, increased by nearly €5M on last year and we see various other smaller fees also growing.

This was partially mitigated by the lack of legal fees and staff bonuses relating to last year’s deal with East Pioneer. After the €2.2M unwinding of deferred consideration (related to the Betboo purchase), the profit before tax for continuing operations was €10.8M. On the subject of that deferred consideration, this seems quite a strange way to account for it as for other companies it is usually just added as part of the acquisition costs at the time of purchase but this seems to be added annually until it reaches the actual amount. A slightly higher tax rate, relating to tax paid in Israel and a €1.1M loss on discontinued operations meant that the annual profit was €9.2M compared to a €145K loss last year.

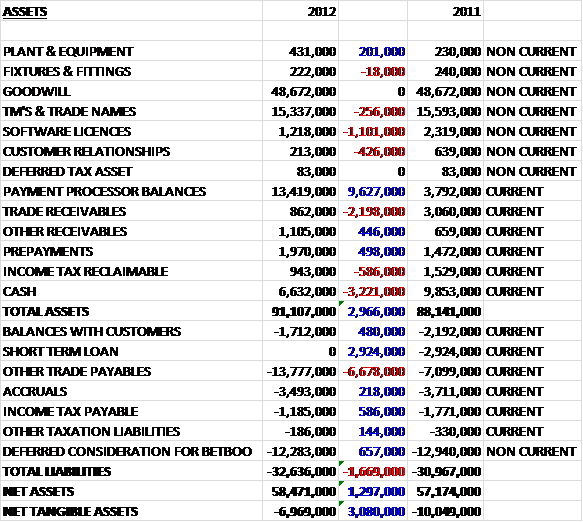

Overall, assets were up by €3M on last year. The bulk of this increase came from a €9.6M hike in payment processor balances, mitigated by lower cash reserves and lower trade receivables. The majority of assets are intangible and there is a huge £49M worth of goodwill. Software licences lost €1.1 in value during the year. Liabilities were also up, entirely due to a €6.7M increase in trade payables which was partially counteracted by falls in all other liabilities. Overall, net tangible assets were £3.1M higher than last year at a negative €7M (not that a company like GVC would be expected to have much in the way of tangible assets).

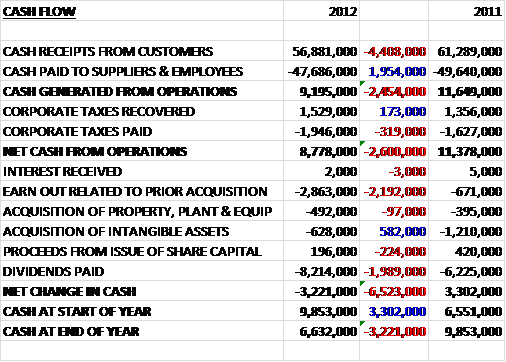

Overall we can see that the cash from operations actually fell when compared to last year as there was €4.4M less cash from customers, mainly due to the fact that more working capital was tied up in the BSB payment processing. A higher amount of tax paid meant that net cash from operations was €2.6M down at €8.8M. Most of this (€8.2M) was paid out in dividends which does not leave much for capital expenditure. The real driving force behind the negative cash flow was the €2.9M earn out related to the continued payments following the Betboo acquisition. The cash outflow was €3.2M compared to a €3.3M inflow last year. The earn out is related to the purchase of Betboo where the sellers get 36 monthly payments from mid-2011 and one extra payment each year equal to 25% of Betboo NGR earned.

Of the sectors, the most profit was earned by Casino Club, with the BSB business also doing well. The Betboo business was loss making during the period. As we have seen, the only sector to reduce revenues was Casino Club which was partially attributable to a reduction in poker revenue which is a trend that has been seen industry wide. Revenues at Betboo grew by 17% despite a lower sports hold. There were additional investments to support this growth which is the explanation given for the loss. Going forward, the group has embarked on internal restructuring to reduce costs in this area.

During the year, the group arranged to dispose of Betaland for a nominal sum. It was thought that the declining profitability meant it no longer made sense to hold on to it and during 2012 it made a loss of €1.1M compared to a profit of €477K the year before. Another issue resolved was that the group reached an amicable settlement with Boss Media regarding some legal claims which resulted in some provisions being released back into the income statement.

Jackpots won in Club Casino are taken straight from the income statement as there is no central fund to cover them. As of the end of the year, a total of €6.6M was available across 37 games.

At the end of the year, it was announced that with William Hill, the group had reached an agreement to buy Sporting Bet. William Hill will receive the Australia business and an option over the Spanish business whilst GVC obtain the other assets, minus a few freehold properties. After the acquisition, the Sportingbet group will need to be substantially restructured which will be costly and it sounds like there are substantial liabilities that were inherited as well as assets, which is possible cause for concern.

This period is one of change for GVC. Revenues were up substantially, driven by the full year contribution of the B2B business. Casino Club revenues were down slightly as online poker became less popular. Although revenues at Betboo were up, increased investment meant that it was loss making. Overall, profits were €9.3M higher at €9.2M. Net tangible assets are up slightly but are still negative and there was a cash outflow of €3.2M, but this seems to be due to more trade receivables being tied up in the new B2B business and there is easily enough cash to cover dividends and there is no debt. On the subject of dividends, at the current price the yield is a good 5.7% but I am not sure of the dividend situation next year. From November 2013, however, the group aim to pay a dividend quarterly. The P/E ratio at the time of writing is 10.9, so still good value in that regard/

Going forward, the group has made a strong start to 2013 and average PRF was 27% higher than the same period of 2012 on a like for like basis but the coming year is going to be completely overshadowed by the Sporting Bet acquisition. It sounds like the purchase comes with quite a few liabilities so I expect there to be a situation of net debt at the next update. Overall, there are some good prospects here but I would like to see how the acquisition beds in before committing myself further.

On 1st July 2013, the group released a trading update. It was mentioned that management have been able to make material reductions in the cost base of Sporting Bet, and by the end of the year costs should have reduced by 40%. Last year, Sporting Bet’s European operations lost €52M, €26.9M of which were exceptional charges. The group have now started outsourcing the IT infrastructure to lower cost jurisdictions, terminated all marketing and corporate sponsorships where return on investment was poor, improved organisational structure and paid off a lot of loans and overdue supplier payments. The cost of these improvements were less than anticipated and it is anticipated that Sporting Bet will be cash generative by the end of the calender year. Sporting Bet NGR was 8% higher than last year and 2012 was also flattered by the Euro 2012 football Championships. Revenues at Casino club increased by 10% per day, and revenues in Betboo were up 25% per day. Another positive of the take-over was the fact that the deferred consideration has been entirely eliminated.

Overall, all this means that the group are going to pay a dividend much earlier than originally thought, and quarterly dividends will take place from November. This really is an excellent update and I think I will try and buy some more of these shares. The dividend has been announced as being 9.06p per share.