Havelock Europa, Westway, Hillend Industrial Park, Dalgety Bay, Fife, KY11 9HE

Havelock Europa is a provider of Interior solutions, including the design manufacture and installation. The group’s main customers are retailers, banks, construction companies, education authorities and commercial organisations. This is where most of the revenue is earned but they also have an Educational Supplies segment that is involved in the design, manufacture and supply of teaching aids, display boards and stages for the education sector. They have undergone a difficult time of late and in 2010 left the main exchange and entered the AIM exchange.

They have now released their results for 2012.

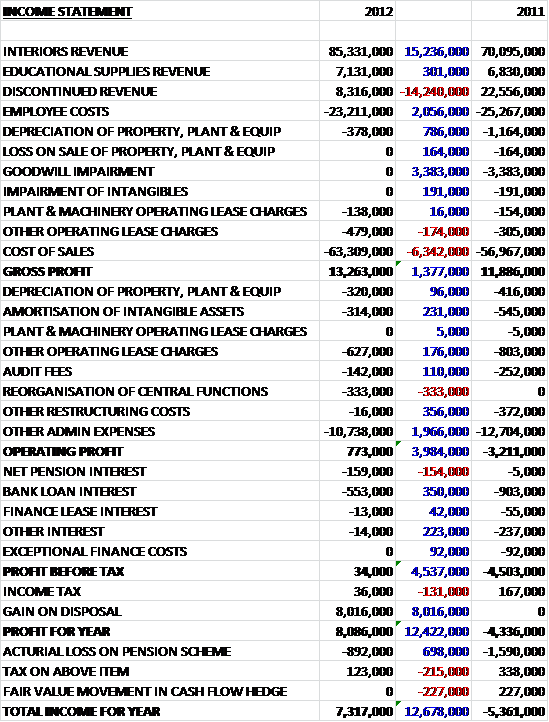

Although revenue is only marginally up on last year, if the revenue of discontinued operations is taken out, interiors revenue is up an impressive £15.2M and educational supply revenue is up by £301K. We can also see employee costs reduce and a few one-off costs that occurred last time did not repeat this year, counteracted by an increase in the rest of the cost of sales. Overall, gross profit was £1.4M up at £13.3M. A reduction in almost all admin charges (except a one-off £333K reorganisation of central functions) meant that operating profit was £4M higher at £773K. Likewise, most financing costs were lower and the profit before tax was £4.5M higher at just £34K (wiped out by the £36K of tax payable). The big news this year though is the £8M gain on disposal of a subsidiary, which caused the profit for the year to increase by £12.4M to £8.1M. Actuarial losses on the pension scheme nudge the total income for the year down a bit to £7.3M.

As far as assets are concerned, we have seen a reduction in almost all long term assets, both tangible and not, mitigated by increases in inventories and trade receivables (hopefully a sign of increased orders). The big two reductions, however, were the sale of the asset held for sale (£8.3M) and the £4.4M reduction in cash. Overall, this meant that total tangible assets were £6.1M lower at £43.9M.

Looking at the liabilities it becomes apparent where the cash received from the sale of the subsidiary has gone. Bank loans were down by a pleasing £14.8M to a manageable £5.7M. The other main reduction in liabilities was the £3.9M of liabilities held by the asset sold. Trade payables was the big increase, though, up £4.9M as the group extended average payment days with its suppliers from 36 days to 52, presumably to help the cash flow figures. Overall, net tangible assets were £7.5M higher at £10M. Much more healthy than last year.

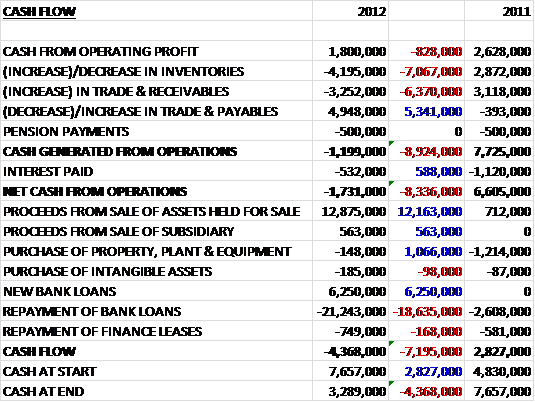

The cash taken from the operating profit is rather disappointing, down £828K from last year to just £1.8M. As we have already seen, an increase in trade and payables was more than counteracted by an increase in both inventories and receivables. The lower debt levels did see a reduced amount of interest paid but at £532K, it was still fairly substantial. Overall, there was a net cash loss from operations of £1.7M compared to a £6.6M gain last year. During the year we can see that the group made £12.9M of cash from the sale of assets relating to the subsidiary (the bulk being trade receivables and property, plant & equipment) and £563K for the subsidiary itself. Taking into account the net assets lost, the cash inflow was about £8M. This was used to pay off debt and a net £15M was returned to the bank, plus £749K in repayment of finance leases.

The overall cash flow was an outflow of £4.4M, which was pretty much meaningless given that most of the cash received was from a disposal and the group paid off a lot of debt. It will be interesting to see what happens next year as I think the cash income from operations needs to grow somewhat.

Although revenues in the interior sector are much higher than in education, the operating profit contribution from the two businesses is very similar (between £472K and £497K). Margins in the interior business were under pressure as lower prices were offered in exchange for more volume. During the period of difficult trading in the past few years, the group has not been able to make any capital investments but a new laser cutting machine has now been ordered which should increase potential volumes by up to 50%. The education business saw a recovery in direct to schools sales and has incorporated the stage systems into being a supplier for the education business.

The group is quite badly exposed to a number of large clients. Lloyds TSB made up 25% of all revenues during the year and Marks & Spencer represented 15% of revenues so if something were to happen to one of these customers, there could be problems. These customers also seem to be leveraging their position to push prices down, which is leaving Havelock little option but to try and find ever more cost savings.

The subsidiaries sold were Showcard Print business, which is what had the bulk of the effect and bought in £12.9M of cash and Clean Air Ltd, which got £563K of cash. Going back five years, the last time the group actually made a profit was in 2008 but the net debt situation in 2012 was the best it has been for some time due to the sales and now stands at a much more manageable £2.4M, down from £13.7M last year.

Going forward, the group is looking to focus on its core business of Retail and Education whilst looking to expand into areas such as Accommodation and Healthcare and has already secured the first projects in these two areas. There has been an increase in activity in the Education sector whilst retail remains uncertain and competitive. Overseas activity grew during the year and the aim is to grow this to be 10% of revenues in the medium term.

Overall then, the group still seems to be in a period of transition. The results are dominated by the sale of the two subsidiaries and the subsequent pay off of some of the bank loans. The margins in the interior business look razor thin and the group his heavily reliant on two large clients, which is cause for concern. Were it not for the sales, the cash flow would also look rather sickly as Havelock struggles to turn that revenue into cash. I am pleased that they are expanding into other areas again and hope that now they are not hamstrung with the large amount of debt they had before, the group can kick on to better things. I will hold and await developments.

At the AGM, the board released a statement that said that it has seen activity levels in the first half at lower levels than in the same period of last year but after discussions with their clients, they are confident of a busy second half of the year. The group completed the first jobs in healthcare and student accommodation, which is a little more encouraging. I don’t like the sound of this update and I wonder if I should take a small loss here and sell up?