Goodwin has now released its final results for the year ended 2016.

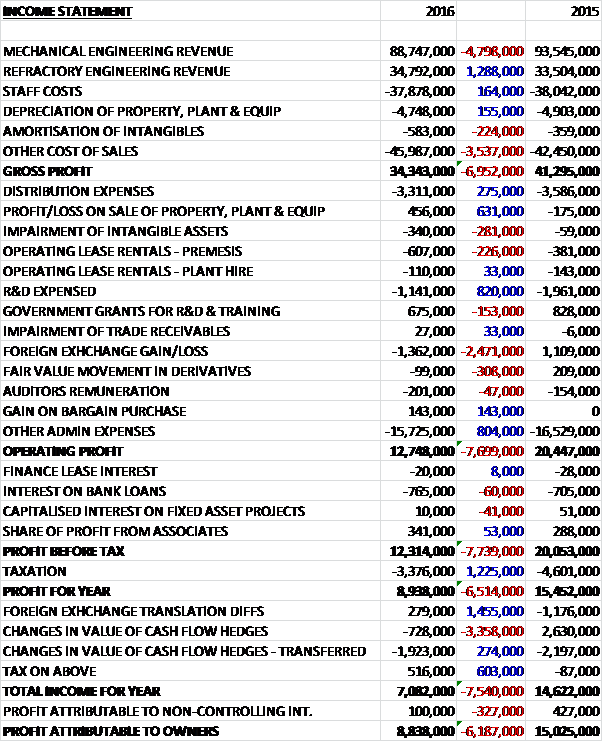

Revenues declined when compared to last year as a £1.3M growth in Refractory Engineering revenue was more than offset by a £4.8M decline in Mechanical Engineering revenue. Conversely, cost of sales increased which meant that the gross profit declined by £7M. Distribution expenses decreased by £275K, R&D expenses fell by £820K and there was a £631K positive movement to a profit from the sale of fixed assets but intangible impairments increased by £281K, operating lease costs were up nearly £200K, there was a £2.5M negative swing to a forex loss and a £308K detrimental movement in the fair value movement of derivatives before an £804K decline in other admin expenses meant the operating profit was down £7.7M. There was little in the way of movement in finance costs but tax expenses reduced by £1.2M to give a profit for the year of £8.8M, a decline of £6.2M year on year.

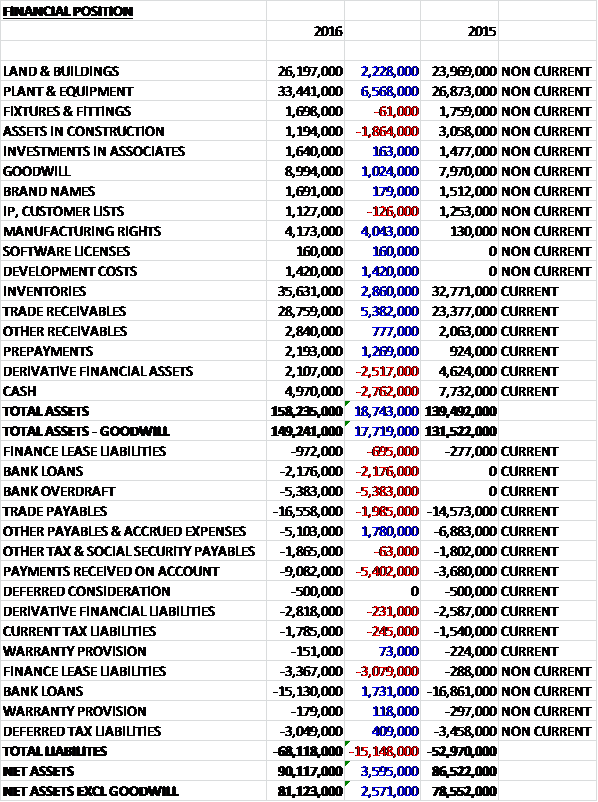

When compared to the end point of last year, total assets increased by £18.7M to £158.2M, driven by a £5.4M growth in trade receivables, a £6.6M increase in plant and equipment, a £4M increase in manufacturing rights, a £2.9M growth in inventories and a £2.2M increase in the value of land and buildings, partially offset by a £2.8M decrease in cash and a £2.5M fall in derivative financial assets. Total liabilities also increased during the year due to a £5.4M increase in payments received on account, a £5.4M growth in the bank overdraft, a £3.1M increase in finance lease liabilities and a £2M growth in trade payables. The end result was a net tangible asset level of £81.1M, a growth of £2.6M year on year.

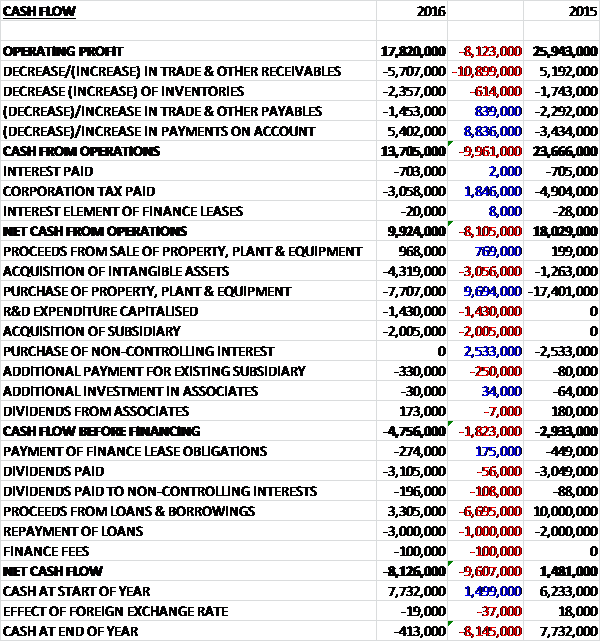

Before movements in working capital, cash profits declined by £8.1M to £17.8M. There was a cash outflow from working capital with an increase in receivables but tax payments were down £1.8M to give a net cash from operations of £9.9M, a decline of £8.1M year on year. The group spent £4.3M on intangible assets, £7.7M on tangible assets, £1.4M on R&D and £2M on acquisitions which meant that before financing there was a cash outflow of £4.8M. Despite this we see a £3.1M dividend payment which meant that there was a cash outflow of £8.1M in the year and a cash level of -£413K at the year-end.

The profit in the Mechanical Engineering division was £11M, a decline of £5.4M year on year; and the profit in the Refractory Engineering division was £4.2M, a fall of £928K when compared to last year.

The severe contraction of the oil and gas industry and mining industries presented a challenge and the resultant reduced spending levels in the jewellery markets and the slowdown in China have all been unhelpful. Easat Radar has a record work load of £12.5M, however, and Noreva has a similar order book level for its nozzle valves which resulted from a combination of winning large orders in Saudi Arabia and from the US LNG industry, and also starts the new year with a record order book.

Steps have been taken at Goodwin International over the past two years to add additional market sectors to its portfolio of products by offering machining and high integrity fabrication for other customers. This has resulted in additional order input for the new financial year but as yet not enough to compensate for the drop off of the oil and gas sector where they are still winning some orders of the few that are available. Some of this new non-valve work will be spread out over multi-year contracts, but nevertheless it has in part allowed the group to mitigate some of the major damage from such a vast contraction of the oil, gas and mining industry activity where they will be unlikely to see significant signs of regeneration for another two years.

Goodwin refractory services benefitted from the asset purchase it made last year from a complementary French casting powder company, and grew its pre-tax profits by 47% to £1.5M. Similarly in the new financial year, following intangible asset purchases in October from Westland and having spent six months of last year constructing a new perlite plant at Hoben, both Dupre Minerals and Hoben are expected to significantly improve their profitability as compared to the financial year just completed.

All the above does not alter the fact that the steel foundry and UK valve manufacturing activity have less orders and the ones they do have are on tighter margins, but at least the new areas of business are softening the unwelcome severe downturn in the core industries.

The group order work load at the year-end is 16% higher than the end of the prior year and stood at £92M. Although some of this workload has tighter margins, it provides a better start to the new year which will be difficult with world trading conditions being less than buoyant.

Goodwin International will be launching its newly developed and patented axial piston control and shut off valve at the Dusseldorf Valve World Exhibition this coming November and, similarly in Dusseldorf, Goodwin Steel Castings will be presenting a paper at the Duplex Conference in October on higher performing duplex stainless steel castings and welding electrode wire and rod.

During the year the group acquired NRPL Aero Oy for a cash consideration of £1.5M plus 20% of the share capital of Easat, a group company. The acquisition gives the group the capability to supply complete radar systems to the air traffic control and coastal surveillance market. The group also acquired Shenzhen King Top Modern Hi Tech Company in January 2016 for a cash consideration of $600K which strengthens the group’s presence in the Chinese investment powder supplies market.

There were a number of additions to intangible assets. £3.5M was added relating to manufacturing rights and customer lists relating to the acquisition of vermiculite and perlite activities from Westland in October. £1.07M of goodwill was added relating to the acquisition of NPRL Aero Oy, a Finnish transceiver business. £640K related to the acquisition of the manufacturing rights and non-compete agreements in relation to a Chinese lost wax investment powder manufacturing business. £736K was capitalised in relation to transceiver development expenditure and £594K was capitalised in relation to the development of a new check valve range.

The lead up to the Brexit vote saw delays in the release of infrastructure investments and the outcome will impose new challenges and uncertainties. The review of trading agreements and legislation is still unknown but the immediate effect has been a weakening of sterling which is a major competitive advantage in the group’s favour as 60% of exports were to countries outside the EU.

At the current share price the shares are trading on a PE of 18.4. There doesn’t seem to be any broker forecasts but this doesn’t look all that cheap to me. After the dividends were kept the same, the shares are trading on a yield of 1.9%.

Overall then this has clearly been a difficult year for the group. Profits declined and although net assets increase, the operating cash flow fell and no free cash was generated. The main issue continues to be the collapse of the oil and gas market where the group makes most of their profits. They have been diversifying recently but it is not enough to compensate. The PE ratio of 18.4 and yield of 1.9% don’t seem to be fully justified in my view so I have sold out here.

On the 14th September the group announced its Q1 results. Revenues declined by £483K to £33M and pre-tax profit fell by £754K to £3M. Sales orders shipped in the quarter reflect the continued lack of capital project release in the energy industry, oil and gas in particular. The group remains confident its products and technology will in the long term produce growth in profitability but the current workload is similar to that seen last year.

On the 5th October the group announced that the new LTIP had been agreed at the AGM (not surprising given the ownership structure). In essence, management will be given shares in the company whereby for each 10% growth in TSR, shares equal to 0.05% of the share capital may be acquired, which in my opinion is a pretty scandalous redistribution of the company from the shareholders to management given this has been devised at a low point in the cycle. This has left a rather unpalatable taste in my mouth.