Wentworth Resources has now released its interim results for the year ending 2016.

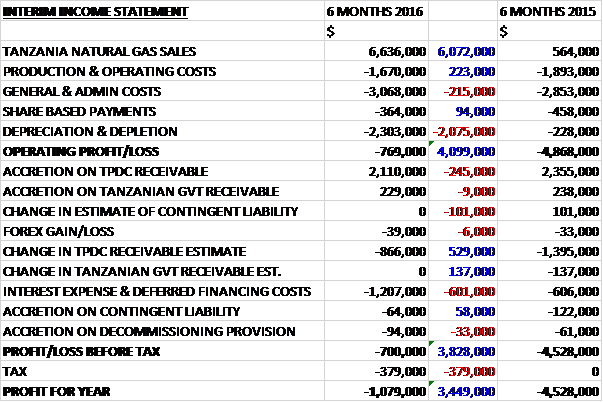

Revenues increased by $6.1M when compared to last year and a production cost decline was offset by an increase in admin costs before a $2.1M depletion charge due to the fact the group is now delivering gas to the pipeline meant that the operating loss declined by $4.1M to $769K and included a net expense of $600K relating to the estimated cost of settlement of ongoing TRA tax audits of historical years of operations. There was a $245K decrease in the RPDCC receivable accretion and a $601K increase in interest costs but the reduction in TPDC receivable estimate fell by $529K. After a maiden tax charge of $379K, the loss for the period came in at $1.1M, an improvement of $3.4M year on year.

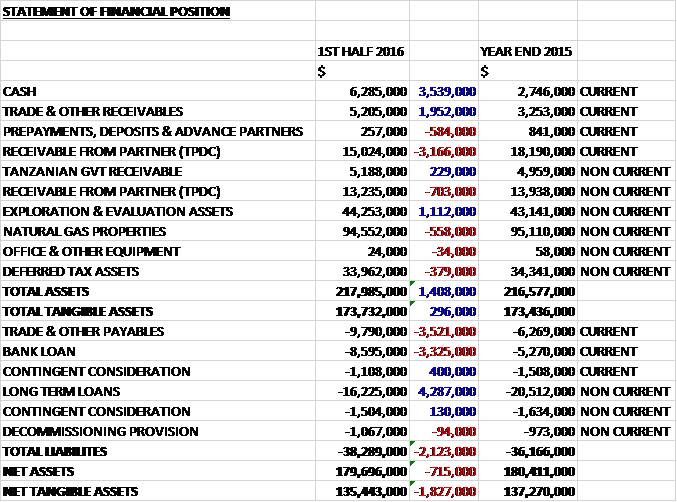

When compared to the end point of last year, total assets increased by $1.4M to $218M driven by a $3.5M growth in cash, a $2M increase in receivables and a $1.1M growth in exploration and evaluation assets, partially offset by a $3.8M fall in the TPDC receivable. Total liabilities also increased during the period due to a $3.5M growth in payables. The end result was a net tangible asset level of $135.4M, a decline of $1.8M over the past six months.

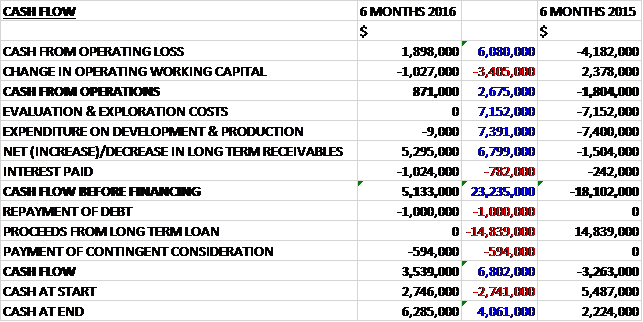

Before movements in working capital, cash profits increased by $6.1M to $1.9M. There was a cash outflow from working capital, however, so the cash inflow from operations came in at $871K, a positive movement of $2.7M year on year. The group also brought in $5.3M from a reduction in the long term receivable and paid $1M on interest payments, although there was no capex during the period. After a $1M debt repayment and a $594K contingent consideration payment, the cash flow for the half year was $3.5M and the cash level at the period-end was $6.3M.

The Tanzania operations showed a profit of $843K for the half year period compared to a loss of $2.6M during the first half of last year. The group achieved an average gross daily gas production of 51MMscf in Q2 compared to 48MMscf in Q1. In the period as a whole, gas sales to the pipeline was 2,037,502MMBtu compared to zero in H1 last year. Sales to the Mtwara power plant were 95,270MMbtu compared to 105,194MMBtu in H1 last year.

Commissioning of the four turbines at the newly built Kinyerezi-1 power station was completed during Q2. Ubungo II power generation facilities and the Mtwara power station were nearing full operational capacity at the end of June while Symbian power generation facilities were not in production at the end of the period. At full operating capacity, the Kinyerezi-1 power station is expected to utilise 25-30MMscf per day of gas, Ubungo II and Symbian power plants 45-50MMscf per day and the Mtwara power plant about 2.2MMscf per day, equating to a total average of between 70 and 80MMscf per day.

The Symbion power plant is an independent power producer and has been shut down since June due to a contractual dispute with the Tanzanian government. It is uncertain as to how long it will remain idle but as the onset of the hot season approaches, power demand is expected to increase and TANESCO is expected to require the station to be operational so hopefully the dispute will be resolved this year.

During the coming year, the remaining new field infrastructure will be completed, including the installation of two liquid separation units at the Msimbati gas processing facility which will allow Mnazi Bay gas to be delivered to the pipeline in accordance to agreed specifications. Most of the wells have already been tied into the pipeline but MB-1 is still producing just 2MMscf per day which fuels the TANESCO-owned 18MW Power Plant in Mtwara and will be tied into the pipeline infrastructure during H2.

Subject to further testing of deliverability from the existing wells and the drilling of additional development wells, as deemed necessary, the group expects gas sales into the pipeline to increase to 130MMScf per day to meet the anticipated growth in gas demand resulting from expanding gas to power generation infrastructure, primarily through the completion of Kinyerezi I expansion.

During Q2, work continued on the expansion of the joint venture owned processing facilities at Msimbatri and is expected to be completed in Q4. The board expect the cost of exploration activities in the country to be fully funded from internally generated cash flow.

The Mozambique operations incurred a loss of $384K, an increase of $167K year on year. In June the government approved an appraisal plan for the Tembo gas discovery. The plan covers a two year period with the group being approved as the operator of the Rovuma onshore block with a participation interest of 85%. State-owned ENH retained a 15% participation interest as a carried partner through the start of commercial operations. In addition, ENH has the right to acquire a further 15% participation interest in the block within 18 months from the date of submission for a development plan for consideration equal to the proportionate share of past costs incurred.

The plan includes the reprocessing and re-interpretation of existing seismic followed by further acquisition of seismic if warranted with the aim of identifying a suitable drilling location. The re-processing of existing seismic will focus on the sands encountered in the Tembo gas discovery and subject to the results of this work, additional seismic may be acquired in Q3 2017. Drilling of an appraisal well will start in 2018 subject to a suitable location being identified. It is expected that the work programme in the country will be funded through internally generated cash flow as available and through the addition of industry partners.

During the period, capital spending totalled $2.2M, primarily incurred in respect of field infrastructure and development capital activities within the Mnazi Bay gas field location. In Mozambique, exploration costs of $1.1M include the assumption of drilling materials upon assuming operatorship of the Rovuma block during Q2. There are currently no exploration capital commitments and budgeted development capital is limited to the completion of Mnazi Bay infrastructure tying field producing assets to the NNGIP. This development activity is expected to be completed in Q4 and cost about $3M. The near term obligations are expected to be funded from existing cash balances and future cash receipts from gas sales.

The Tanzanian government published a new finance bill into force in July. It introduces measures aimed at reducing tax evasion and plugging loopholes for tax avoidance. The bill introduces a number of changes to the tax regime which impacts the oil and gas sector. The group has ongoing discussions with industry participants and the Tanzania Revenue Agency to better understand how these changes will impact them. The company does not expect operations in Tanzania to be significantly impacted by the introduction of the bill but this sounds a bit ominous.

As of the period-end the group was owed $2.1M related to June gas sales to TPDC which was collected in full in July. Receivables of $1.3M from TPDC for filling and packing the pipeline in Q3 2015 were to start being paid in Q2 2016 but the partners have agreed to extend payment terms for this receivable and expect the full amount to be received within the next year. The long-term receivable from TPDC currently stands at $28.3M after $6.2M of retained gas revenue was used to offset them and the company paid another $1.1M of TPDC costs during the period. The recovery of this receivable is likely to inflate cash flow considerably over the coming year or so.

As of the period-end the partners were owed eleven months of gas sales for sales made to TANESCO, with $1.8M being owed to the group, of which $500K is expected to be collected during August. The group are engaged with TANESCO to accelerate payments of amounts past due.

The group repaid $1M if their loan debt during the period but this still leaves $24.8M outstanding, $8.6M of which needs to be paid back over the coming year.

Going forward, the board expect demand in Q3 to be constrained given the suspension by the Tanzanian government of the power purchase agreement with Symbion; the recently commenced major overhaul of one of the turbines at the Ubungo II power plant; and commissioning gas needed for the Songo Songo processing facility along the new transnational pipeline. Although gas deliveries depend on the gas demand from government organisation, production levels of 70 to 80MMscf per day are still considered achievable in 2016 if these issues are resolved – this seems like a big “if” to me.

Overall then this is a bit of a lacklustre set of results. The performance is improving but the group is still loss making at the operating level. Net assets also declined but the operating cash inflow increased and they are actually producing a decent amount of free cash flow, aided by the collection of the long-term receivable. The group seem to be generating enough cash for their immediate requirements but more will be needed at some point for the Mozambique drill. Going forward, near-term there are demand issues related to the Symbion dispute with the government so for now, I don’t think this is the right time to jump in here.