IQE has now released their interim results for the year ending 2016.

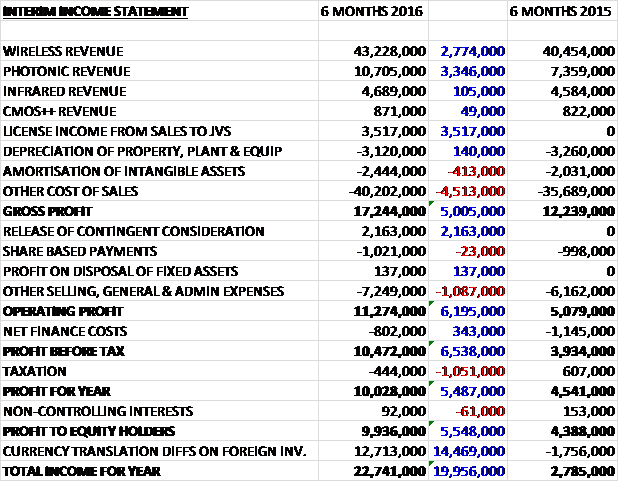

Revenues increased when compared to the first half of last year with a £3.3M growth in photonic revenue, a £2.8M increase in wireless revenue and a £3.5M maiden license income from sales to joint ventures. Depreciation was down slightly but amortisation increased by £413K and other cost of sales grew by £4.5M to give a gross profit £5M above that of last time. We then see a £2.1M income from the release of contingent consideration but a £1M growth in admin expenses and when finance costs fell by £343K and tax increased by £1.1M the profit for the period came in at £9.9M, a growth of £5.5M year on year.

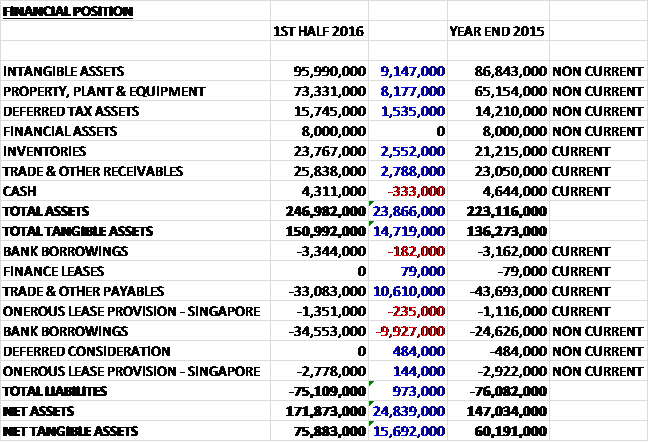

When compared to the end point of last year, total assets increased by £28.9M to £247M driven by a £9.1M increase in intangible assets, an £8.2M growth in property, plant & equipment, a £2.8M increase in receivables, a £2.6M growth in inventories and a £1.5M increase in deferred tax assets. Total liabilities declined during the year as a £10.1M increase in bank borrowings was offset by a £10.6M growth in payables. The end result was a net tangible asset level of £75.9M, a growth of 15.7M over the past six months, mostly as a result of favourable forex movements.

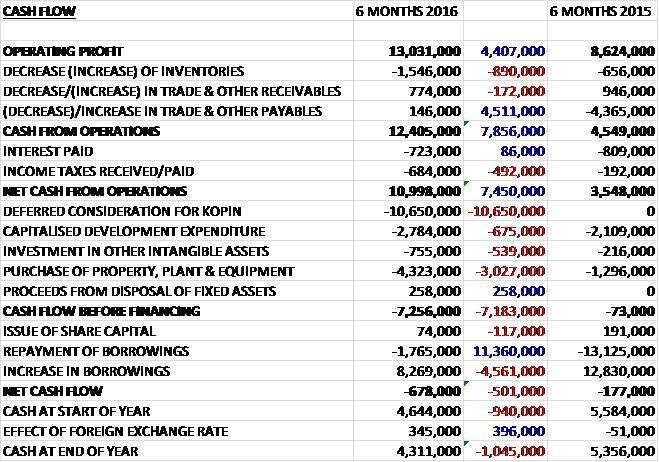

Before movements in working capital, cash profits increased by £4.4M to £13M. There was a modest outflow of cash from working capital but this was much less than last year and after tax payments increased by £492K the net cash from operations came in at £11M, a growth of £7.5M year on year. The group spent £4.3M on property, plant & equipment and £2.8M on development costs with another £755K going on other intangible assets. The group also paid £10.7M on deferred consideration for Kopin which gave a cash outflow of £7.3M before financing. The group then took out a net £6.5M of new borrowings which meant there was a cash outflow of £678K and a cash level of £4.3M at the period-end.

The operating profit in the wireless division was £5.1M, broadly flat year on year. The market has been more subdued over the past few years reflecting a lull in mobile handset innovation. As a result the group estimate that the materials market is currently growing at about 5% per annum. The supply chain has also been characterised by inventory corrections. The board expect the growth rate of the market to increase over the next few years, however as innovation in handset technology accelerates replacement cycles, along with some other factors such as the emergence of 5G communication.

The operating profit in the photonics business was £2.7M, a growth of £1.1M when compared to the first half of last year. The photonics market is being driven by a diverse range of applications, and it is at an early stage in the growth cycle and the board expect this business to continue to grow strongly for the foreseeable future. Their growth ambitions are underpinned by a pipeline of programmes with blue chip customers for high volume applications.

The operating profit in the infra-red division was £830K, a growth of £175K when compared to the first half of 2015. Sales are currently concentrated in defence related applications but through engagement in programmes in consumer, medical and industrial imaging, the group expect this segment to increasingly transition into new markets over the coming years. The operating loss in the CMOS++ business was £1.4M, an increase of £734K year on year.

There is currently little in the way of income from the power market but the size and scale of the markets are many times larger than the group’s existing markets so represent transformational opportunities for them. At present the power switching chips are made using silicon, which has performance limitations.

Likewise, there is currently little in the way of solar revenues. Due to the decline in energy prices, the group has switched its primary focus to penetrating the space market, where their technology is already embedded. The current pipeline of activities suggests that the group can expect to see good commercial progress in the next two to three years.

The group made a profit of £3.5M from license income from sales to joint ventures which was the first contribution from this income stream. The group recognised revenue of £800K and made purchases of £4.2M from its joint venture in Singapore. They recognised revenue of £2.8M, made purchases of £2M and recharged costs of £200K with their joint venture in the UK. For the year as a whole, revenue is expected to be lower than the £8M received last year and 2017 levels are expected to be similar to this year.

The group has developed a broad portfolio of IP for advance semiconductor materials. In addition to the £3.5M of license income generated in the first half, this IP portfolio is creating a platform for continuing growth across the current and emerging markets. They have a pipeline of new products and customer qualifications which underpin their growth ambitions with programmes expected to ramp up through 2017 and 2018. This includes new photonic applications, wireless base stations, advanced solar and power switching applications.

As usual, a number of “one-off” costs were incurred during the period with £800K of acquisition costs and £1M of share based payments – I don’t actually agree these are one-off! They also generated a non-cash profit of £2.2M arising from a reduction in the estimated remaining deferred consideration in respect of a previous acquisition.

The Kopin deferred consideration balance of £10.7M was settled in full in January and the remaining balance of deferred consideration of about £1.8M will be settled in full by the end of September.

Trading in the second half of the year started well, and with the benefit of a strong pipeline and increasing revenue diversification the board remains confident that the group is on track to deliver full year earnings in line with expectations.

At the current share price the shares are trading on a PE ratio of 13.1 but this reduces to 11.6 on Edison’s full year forecast. At the period-end the group has net debt of £33.6M compared to £23.2M at the start of the year, reflecting the deferred consideration payment made during the period. Including the deferred consideration, the leverage was £35.4M compared to £49M at this point of last year. There are no dividends on offer here.

Overall then this has been a good period for the group. Profits were up; net assets increased, albeit as a result of forex movements; and the operating cash flow improved. Once again no free cash was generated but this was due to the deferred consideration paid and should improve going forward. The wireless market was flat but still very profitable but the Photonics division is where the big improvement was made, with growth expected to continue. The group is also benefiting from license income and the IR division saw profits increase modestly.

The CMOSS division is still loss making and in fact, losses widened but the power market is expected to be potentially transformational going forward. Trading in the second half has started well and a forward PE of 11.6 still looks good value to me, I continue to hold.

On the 25th October the group announced that Chairman Godfrey Ainsworth sold 119,958 shares at a value of £36.5K. Following this transaction, he holds 3,154,197 shares.

On the 14th December the group released a trading update. Since the interim announcement, trading has continued to be strong across multiple markets, especially in the photonics business. As a consequence, the group announced that it is on track to deliver 2016 revenue and adjusted operating profit ahead of expectations. It is expected that revenues will reflect a double digit rate of growth year on year and that H2 revenues will be up on H1.

The wireless business has largely performed as expected and remains on track for year on year growth. Photonics continues to be the fastest growing segment, enjoying a strong double digit growth year on year. Good progress with customer qualifications in photonics during the year provides a solid platform for continuing strong growth for this business. In response to this opportunity, the group has increased its capital investment in the second half. Infra-Red has performed in line with expectations, and license income has reduced from the front loaded income enjoyed last year.

Revenues also benefited from the devaluation of Sterling but the impact on profitability is largely presentational as the majority of the group’s costs are denominated in dollars. Furthermore, although the group has deleveraged its balance sheet during the year, in underlying dollar terms, the presentation of this is expected to be distorted adversely in sterling.

Overall pretty good, although debt looks to have increased and capex is up so not sure there will be a positive cash flow. Anyway, I continue to hold.