Safestyle have now released their interim results for the year ending 2016.

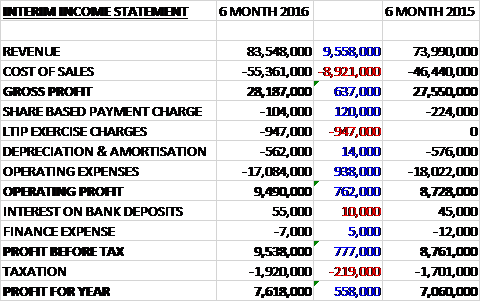

Revenues increased by £9.6M when compared to the first half of last year and after cost of sales saw a more modest growth, the gross profit increased by £637K. There was a £947K LTIP exercise charge in the period mainly relating to national insurance contribution charges that did not occur last year but other operating expenses declined which meant that the operating profit grew by £762K. After finance costs were broadly flat and tax increased by £219K, the profit for the period came in at £7.6M, a growth of £558K year on year.

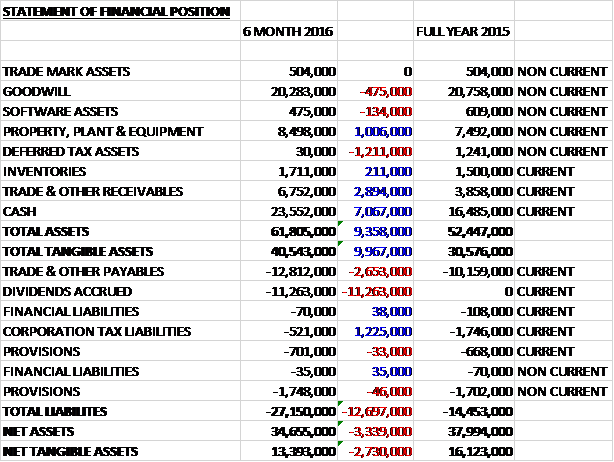

When compared to the end point of last year, total assets increased by £9.4M to £61.8M. This was driven by a £7.1M increase in cash, a £2.9M growth in receivables and a £1M increase in property, plant and equipment, partially offset by a £1.2M decline in deferred tax assets. Total liabilities also grew during the period, mainly as a result of the £11.3M of exceptional dividends accrued along with a £2.7M growth in payables, partially offset by a £1.2M decline in corporation tax liabilities. The end result was a net tangible asset level of £13.4M, a decline of £2.7M over the past six months.

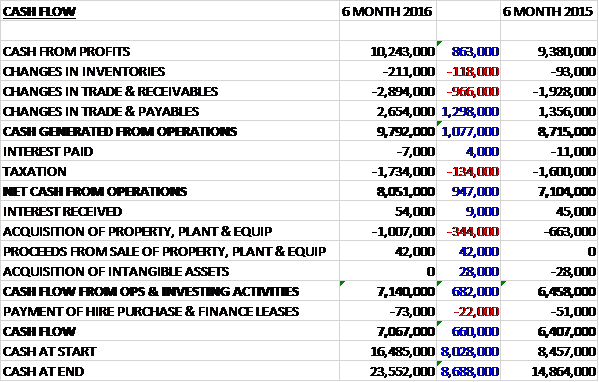

Before movements in working capital, cash profits increased by £863K to £10.2M. There was a modest cash outflow from working cap but this was less than last year and after tax payments increased by £134K the net cash from operations came in at £8.1M, a growth of £947K year on year. The group spent £1M on property, plant and equipment which was the only capex so the free cash flow was £7.1M to give a cash flow for the period of £7.1M and a cash level of £23.6M at the period-end, although of course the dividends have got to come off that.

The growth in revenue was due to both an increase in volume and price with a 5.7% growth in the volume of frames installed and a 6.9% growth in the average unit price. The price list increase implemented at the start of the year counterbalanced the additional costs of the new consumer finance products and unit prices have been further boosted by the sale and installation of 208 conservatory upgrades. Average sales prices increased steadily through the period as the pre-increase order book was installed, which suggests that gross margin will continue to improve in the second half of the year.

The market in which the group operates contracted by 2.2% by volume in the period, albeit with some recovery in Q2 which the board expect to continue into Q3. The group has continued to grow its market share, increasing from 9.5% to 10%. The second half of the year has started on plan, with the three new frame colours introduced at the start of June being well received and current order intake shows growth in line with board expectations. They remain encouraged by the demand for their conservatory refurbishment programme which remains on target.

Investment in the new factory extension at Wombwell has started and is currently on time and budget with the facility being scheduled to be operational in the summer of 2017. The group continued to invest in buildings its brand profile and spent an additional £600K in TV advertising and in addition, salary costs increased by £600K as a result of the annual pay award and continued investment in new staff. They have opened new offices in Guildford and Norwich.

So far in the second half they have seen no change in demand which might be attributed to the Brexit vote as order intake increased on the previous year, albeit at a lower rate than in the first half due to more challenging comparatives.

Going forward, the board expect the market will show some modest volume growth for the rest of the year. They expect to continue to gain market share, reflecting the strong order book at the period-end and their continued sales performance. In all they expect to deliver full year results in line with expectations.

At the current share price the shares trade on a PE ratio of 16.2 which reduces to 14.2 on the full year forecast. After a 10.3% increase in the interim dividend, the shares are yielding 6.2% which falls to 4% on the full year forecast assuming no further special dividends.

Overall then this has been another strong period for the group. Profit increased and operating cash flow improved with loads of free cash being generated. The net assets did decline but this was due to the special dividend. Both volumes and prices increased but the latter was just enough to cover the introduction of new consumer finance products to improve the former! Having said that, margin is expected to grow in G2. So far Brexit has had no effect on the company and this is one I’m glad I own. With a forward PE of 14.2 and yield of 4% this is no longer the bargain it once was. Still, happy to hold though.

On the 27th September the group announced that CEO Steve Birmingham purchased 17,500 shares at a value of £49.1K which seems to be a good sign.

On the 21st November the group announced that CEO Steve Birmingham purchased 50,000 shares at a value of £124.5K which is a good sign as far as I’m concerned – tempted to pick up a few more here.

On the 23rd January the group released a trading update covering the whole year. They have continued to trade well, with revenue for the year increasing 9.8% to £163.5M. In addition, pre-tax profit has shown good progress and is in line with board expectations. As expected, however, the second half showed slower growth than in H1 due to more challenging comparatives.

They have continued to take market share and the number of frames manufactured increased by 3.2% with the number of installations up 4.7%. Price increases implemented at the start of the year helped them deliver improved operating margins, offsetting consumer finance subsidy costs, which have become an established feature of the cost base.

Cash flow has continued to be strong and they ended the year with cash of £13.5M despite incurring £4.6M of expenditure on the new factory extension which continues to be on time and on budget. 2017 will see increases in the raw material costs primarily due to sterling weakness but they plan to offset such increases by improving the price they obtain for their products. Despite the uncertain macroeconomic outlook, they remain cautiously optimistic and believe they are well positioned to continue growing the business.

Overall then performance has been good this year but the concern is the increased raw material prices. The board state they will offset this by increasing prices but having already done this in response to the consumer finance costs, I am not sure there is much space for this. I continue to hold but this is not quite a solid as it was.

On the 13th February the group announced that Giles Richell will join the board in the newly created role of COO with immediate effect. He was most recently MD at Eminox, part of the Hexadex group.