International Greetings has now released its interim results for the year ending 2017.

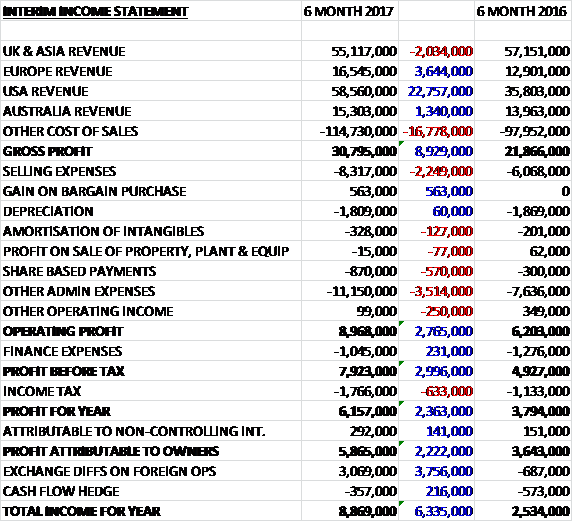

Revenues increased when compared to the first half of last year as a £2M decline in UK revenue due to scheduling of certain customer deliveries into the second half of the year, was more than offset by a £22.8M growth in US revenue, a £3.6M increase in European revenue and a £1.3M growth in Australian revenue due to favourable currency movements. Cost of sales also increased to give a gross profit £8.9M above that of last time. Selling expenses grew by £2.2M, share based payments were up £570K and other admin expenses increased by £3.5M, which will be higher in the second half, but the group benefited from a £563K gain on a bargain acquisition so that the operating profit grew by £2.8M. Finance expenses were down £231K but tax charges were up £633K which meant that the profit in the period was £5.9M, a growth of £2.2M year on year.

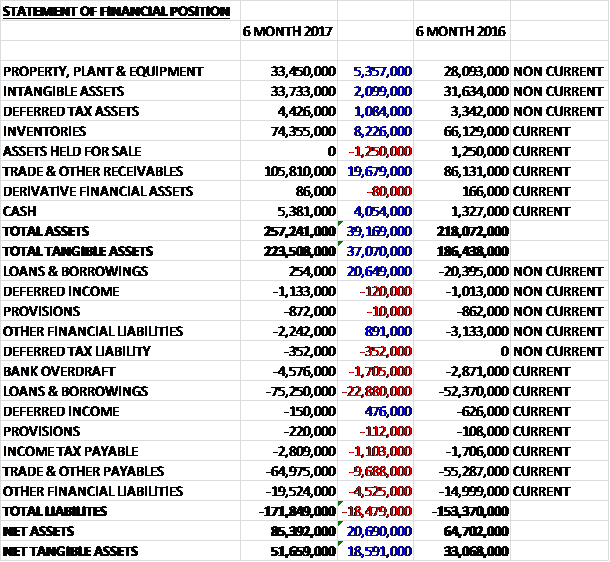

When compared to the end point of last year, total assets increased by £39.2M to £257.2M driven by a £19.7M growth in receivables, an £8.2M increase in inventories, a £5.4M growth in in property, plant & equipment and a £4.1M increase in cash. Total liabilities also increased during the period due to a £9.7M growth in payables, a £4.5M increase in other financial liabilities and a £2.1M growth in borrowings. The end result is a net tangible asset level of £51.7M, a growth of £18.6M over the past six months.

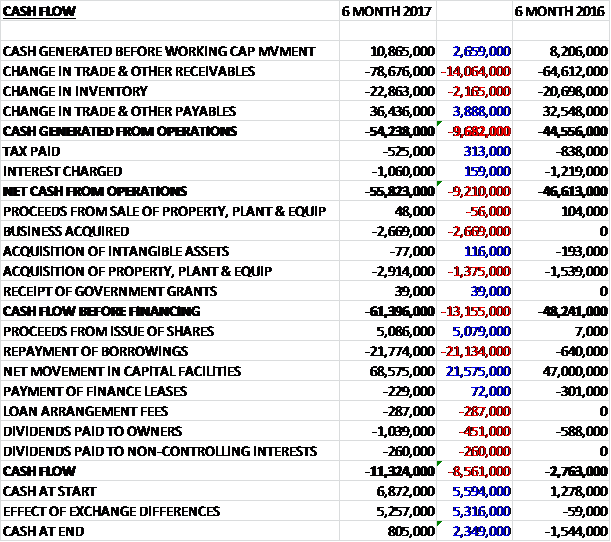

Before movements in working capital, cash profits grew by £2.7M to £10.9M. As usual there was a large outflow of cash from working capital but this was greater than last time and the net cash outflow from operations was £55.8M, an increase of £9.2M year on year. The group then spent £2.9M on property, plant and equipment along with a third of that going on updating the warehouse management system in Australia, with £2.7M on acquisition so that before financing there was a cash outflow of £61.4M. The group made £5.1M from new share issues and a net £47M from new loans so that after £1.3M was spent on dividends, there was a cash outflow of £11.3M in the period and a cash level of £805K at the end of the half year.

The profit in the UK and Asian business was £4M, a growth of £442K year on year despite the scheduling of certain customer deliveries into the second half of the year resulting in sales being 3.6% lower. The manufacturing facility in China has provided increased volumes of products to the UK business with record levels of bags and cards being produced. The profit in the European business was £1.3M, an increase of £423K when compared to the first half of last year with a strong order book in place for the balance of the year.

Excluding exceptional items, the profit in the US business was £3.8M, a growth of £2M when compared to the first half of 2016 with organic sales up 36%. There has been sales growth across all channels and product categories. They have begun to deliver fast payback from the investment programme in their US wrap manufacturing facilities and have identified further opportunities both in the US and through leveraging their capability across the group to accelerate growth across the Americas. The board are pleased with the smooth integration of the recently acquired Lang Group and are optimistic with prospects for commercial, operational and purchasing synergies to deliver enhanced profitability.

The profit in the Australian business was £1M, an increase of £511K year on year despite the timing of some customer delivery requirements impacting on sales revenues, which declined on a constant currency basis. The positive outcome is as a result of improved product mix and operational efficiency.

It is worth noting that the group expect by the year-end that all US tax losses will have been recognised with just £400K of tax loss effect unrecognised in the UK. This means that the effective tax rate will rise quickly in future periods especially if growth is heavily fuelled by the US business, which is the expectation. Cash tax is increasingly payable in most of the geographic regions of operations as historical losses are fully utilised.

In July the group acquired Lang Companies for a cash consideration of £2.7M. The business is a supplier of branded consumer home décor and lifestyle products based in the US. In the period since acquisition, it has contributed £761K of profit, with £563K of that relating to the bargain purchase as the group’s assets held more value than the consideration paid. The business is expected to be marginally earnings enhancing in the current year and more materially accretive in 2018.

Going forward the board is confident that the current rate of sales and gross margin will continue into the second half of the year, resulting in the annual financial performance of the group now expected to be above current market forecasts. While the timing of overheads and the acquisition of Lang part way through the year (excluding loss making months) has slightly flattered first half results, they are confident that the full year outlook for profit and EPS will continue to outperform.

The net debt position at the period-end was £76.4M compared to £78M at this point of last year despite forex movements adding an additional £7M to debt. At the current share price the shares are trading on a PE ratio of 22.9 but this falls to 17.3 on the full year consensus forecast. After an increase in the interim dividend the shares are yielding 1.2% which increases to 1.5% on the full year forecast.

Overall then this has been a positive period for the group. Profits were up and net assets increased. The cash flow is a bit of a concern as the operating cash outflow grew when compared to last year, apparently due to investment into the acquisition.

All regions saw performance improve with the US enjoying particularly strong growth, although it should be kept in mind that the tax losses from the region will have been used up by the end of the year. The performance for the full year is expected to be above forecasts but the shares no longer look cheap with a forward PE of 17.3 and yield of 1.5%. I think then that the valuation probably takes into account the outperformance.

On the 5th January the group released a trading update covering Q3, including the important Christmas trading period. Trading continued to be strong over the quarter and results remain in line with the upgraded expectations announced in November. The board remains confident in the full year outlook of the group.

On the 24th March the group released a trading update covering 2017. Group revenues are now expected to exceed £300M and profitability is expected to be ahead of market expectations. Cash generation is well ahead of previously expected levels. All regions continue to trade profitably. The group’s trading profit coupled with lower interest costs from a strong cash flow are expected to yield a profit outcome for the year that is significantly ahead of market expectations.

Profit growth in the Americas has been particularly strong due to the development of their product offering and customer base alongside significant advances in operational efficiency. The integration of Lang has progressed well with the realisation of synergies in line with those expected at this stage and more to come next year. Momentum in the region remains strong with numerous opportunities for further growth.

Markets in Australia were more challenging. The business has invested to reposition itself in less commoditised product categories, including the costs to win and then deliver on a three-year contract for the supply of cards to the country’ s largest discount retailer. This will supress performance for 2017 but provides good growth opportunities for 2018 and beyond. Scope remains to drive efficiency and focus on higher margin categories whilst leveraging group wide initiatives in product development and design.

The currency headwinds faced by the UK businesses were largely neutralised by a robust performance in the Celebrations product categories. A reorganisation and further integration of the three UK businesses is already in progress.

In continental Europe the group was able to grow revenue and profit during the period due to an excellent operational performance coupled with the strategy of focussing on growth retailers in the region. As well as expanding business within core markets in Western Europe, sales to Poland and Slovakia have also growth, yielding further incremental profitability.

All this sounds pretty good to me but the shares of run off a bit ahead of themselves now in my opinion.

On the 18th April the group released a trading update covering the year ended 2018. The group’s trading accelerated in the second half of the year with all regions delivering strong revenue growth and increased profits. As a result the board anticipates a full year of overall progress and performance in line with management expectations.

In the US the business has delivered significant overall profit growth during the year driven by increased revenues and margins resulting from improvements in the mix of product categories and customer channels. The project to upgrade IT systems to drive further efficiencies and provide a platform for significant further growth has progressed on time and on budget.

In Australia, organic sales and profits have advanced driven by growth from existing and new customers. The acquisition of Biscay Greetings in January has been integrated into the region’s operations with all anticipated synergies on track to be delivered in 2019.

In the UK the group benefited from the combining of its three businesses under one leadership team, delivering increased revenue and profits for the year. Production of a new product category (paper bags for the fashion and cosmetics industry) started in September. This operation offers incremental opportunities whilst leveraging many of the group’s existing capabilities. The UK is now well placed for future sales and profits growth.

In Continental Europe, a record overall performance was achieved as a result of stronger sales and improved efficiencies. Furthermore during the year a new high-speed printing press was installed which became operational in March which enhances both capacity and capability within the business.

This all seems fine and I continue to hold.