Murgitroyd has now released its final results for the year ended 2016.

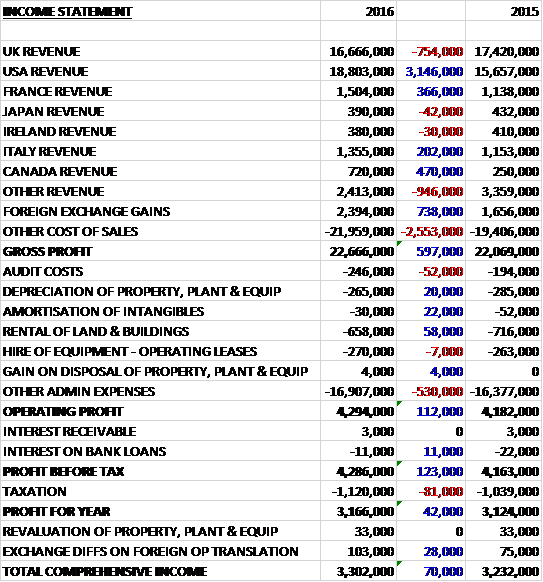

Revenues increased when compared to last year due to a £3.1M growth in US revenue, a £470K increase in Canadian revenue and a £366K growth in French revenue, partially offset by a £754K decline in UK revenue and a £946K reduction in other revenue. The group benefited from a £738K increase in forex gains but cost of sales increased by £2.6M to give a gross profit £597K above that of last time. Admin expenses also increased due to a greater investment in marketing and sales, and tax charges were up £81K which meant that the profit for the year was £3.2M, broadly flat year on year with a £42K increase.

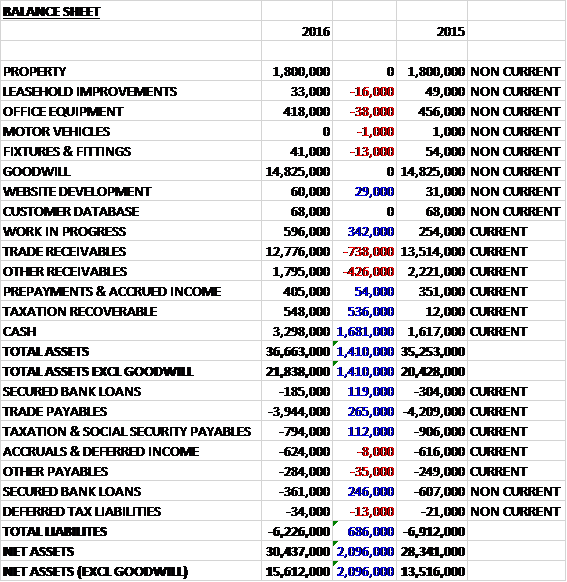

When compared to the end point of last year, total assets increased by £1.4M to £36.7M driven by a £1.7M increase in cash and a £536K growth in taxation recoverable, partially offset by a £738K decline in trade receivables and a £426K reduction in other receivables. Total liabilities declined during the period due to a £265K fall in trade payables and a £365K decline in secured bank loans. The end result was a net tangible asset level of £15.6M, a growth of £2.1M year on year.

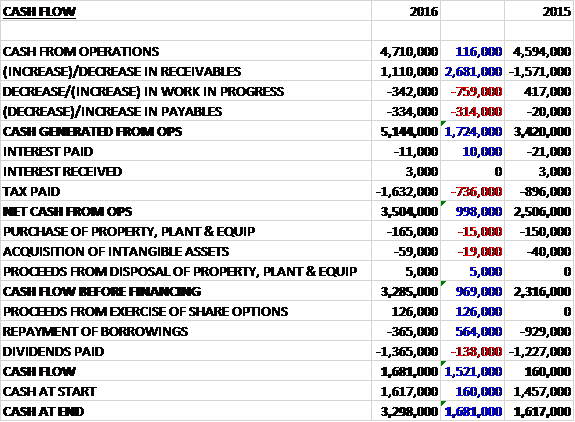

Before movements in working capital cash profits increased by £116K to £4.7M. There was a cash inflow from working capital due to a fall in receivables but tax payments increased by £736K and the net cash from operations came in at £3.5M, a growth of £998K year on year. The group spent £165K on property, plant and equipment along with £59K on intangible assets so there was free cash flow of £3.3M. Of this, £365K was used to pay back loans and £1.4M was spent on dividends to give a cash flow for the year of £1.7M and a cash level of £3.3M at the year-end.

The group continue to see good growth in the US which remains the main focus of business development activity and the growing presence there offsets continuing weaker European demand, including in the UK.

Of the total increase in revenue, nearly 32% was generated by the global support services group. Client wins in this area have resulted in a £3.4M increase in revenue over the past three years and the division now represents nearly a third of the total with further growth in this area anticipated. The rest of the increase was produced by the Attorney Practice Groups with last year’s productivity gains in this area having continued into this year.

It is apparently too early to say with certainty what the long term consequences of the Brexit vote will be on the business and the European IP market but management is confident that the geographic spread of their activities and customer base puts them in a strong market position. The stats show that there was an increase in CTM applications during the year, setting a new record. The EPO stats show a 1.6% increase in patent filings with some 24% of the total originating in the US.

Since the year-end, the group completed the acquisition of certain trade and assets from Dallas-based MDB Capital group and Managua-registered Patentvest for a consideration of $2.4M which is expected to be broadly earnings neutral in its first year.

During the year, Dr Christopher Masters and John Reid were appointed as non-executive directors. The board was further enhanced by the appointment of Gordon Stark as COO. It has also been confirmed that executive Chairman Ian Murgitroyd will move to a non-executive position at the AGM.

The new financial year has seen the group absorb one-off transaction and integration costs from the acquisition completed in June which will affect the interim results. Notwithstanding the uncertainty from the Brexit vote, including the volatility seen in forex markets, and continuing macro-economic challenges to be addressed across Europe, the board remain encouraged by their ability to win new business, particularly in the UK, and are committed to the delivery of sustainable higher earnings as well as increased revenue over the longer term.

At the current share price the shares are trading on a PE ratio of 15.4 which falls to 14.6 on next year’s consensus forecast. After an 8.5% increase in the total dividend the shares are yielding 3% which increases to 3.2% on next year’s forecast. The net cash position at the year-end was £2.75M compared to £706K at the end of last year.

Overall then this has been a solid year for the group. Profits were basically flat but net assets improved, as did the operating cash flow with a decent amount of free cash being generated. The market in general for the Murgitroyd seems rather subdued with growth in North America offsetting declines in the UK, and the Brexit vote may yet affect trading. With a forward PE of 14.6 and yield of 3.2% this is not a value play, nor necessarily a growth one but the group has net cash, generates free cash and seems like a safe place for the moment.