Real Good Food has now released its interim results for the year ending 2017.

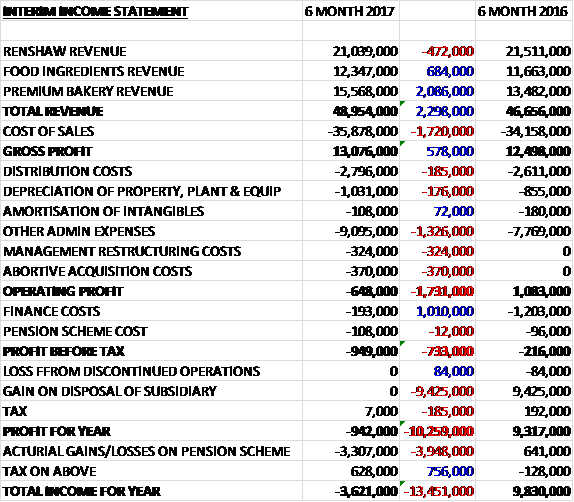

Revenues grew when compared to the first half of last year as a £472K decline in Renshaw revenue was more than offset by a £684K increase in food ingredients revenue and a £2.1M growth in premium bakery revenue. Cost of sales increased by £1.7M to give a gross profit £578K above that of last time. Distribution costs increased by £185K, depreciation was up £176K and other underlying admin costs grew by £1.3M. We also see £370K in abortive acquisition expense and £324K in management restructuring costs to give an operating loss of £648K, a detrimental movement of £1.7M. Finance costs were down £1M but tax income declined by £185K to give a loss for the period of £942K, an increase of £918K year on year.

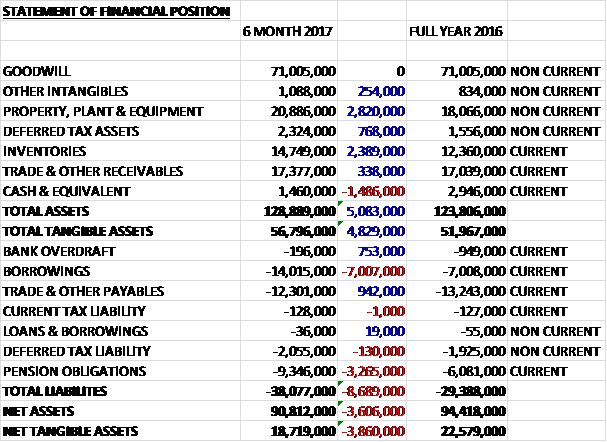

When compared to the end point of last year, total assets increased by £5.1M driven by a £2.8M growth in property, plant and equipment, a £2.4M increase in inventories and a £768K growth in deferred tax assets partially offset by a £1.5M decline in cash. Total liabilities also increased during the period as a £7M growth in borrowings and a £3.3M increase in pension obligations was partially offset by a £942K decline in payables. The end result was a net tangible asset level of £18.7M, a decline of £3.9M over the past six months.

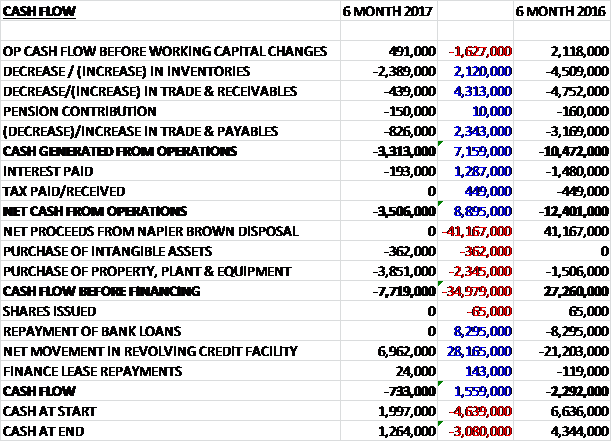

Before movements in working capital, cash profits declined by £1.6M to £491K. There was a cash outflow from working capital but this was less than last time and after interest payments reduced by £1.3M and tax charges declined by £449K there was a net cash outflow of £3.5M from operations, an improvement of £8.9M year on year. The group spent £3.9M on tangible fixed assets along with £362K on intangible assets to give a cash outflow of £7.7M before financing. The group took out £7M of new loans which meant that there was a cash outflow of £733K in the half and a cash level of £1.3M at the period-end.

The profit for the period declined due to increased expensed investment costs across the group, primarily in the development centre and in the US, which will drive future growth and operating efficiencies. It was also impacted by the performance of the food ingredients division which suffered volatile commodity pricings.

The operating profit of the Cake Decoration division was £2.8M. While the market was not as buoyant during the summer as in recent years, sales trends improved towards the autumn particularly with the return of the Great British Bake Off. The first half saw significant investment in the product ranges with the re-launch of the UK Renshaw Professional range and a new product, Renshaw Extra, targeted at the European market. Rainbow Dust Colours also re-launched its market leading edible colouring, Progel, for the European market. Significant investment was made in opening a new warehouse in New Jersey, as the base of the new Renshaw Americas business.

The operating loss of the Food Ingredients division was £684K. Difficult conditions continued in both of Garrett’s main commodity markets and this was followed by short term difficulties caused by the weakening of Sterling in September. Sugar supplies have become critically short which will constrain volumes, though markedly higher prices should improve margins. The dairy market has also seen upward price movement and it is likely to be six months before it stabilises. The price rises is both these markets will, in due course, provide the business with a number of opportunities, through its sourcing expertise. R&W Scott has performed solidly, increasing its delivered margin over last year while operationally it performed well.

The operating profit of the Premium Bakery business was £94K. Sales have performed well with Haydens strongly ahead of last year with good sales through Waitrose and new business gained at Marks and Spencer. Growth at Chantilly has been constrained by the delay in moving to new premises which is now timed for early 2017. While the outlook on sales remains positive, EBITDA will be more challenging in the second half as recent significant raw material inflation (butter and cream prices have doubled recently as a result of a sudden drop in milk production across the EU and the effect in the UK has been exacerbated by the weakness of sterling) is unlikely to be fully offset by price recovery until the New Year.

To date the key Q3 trading period is in line with expectations and the board anticipate significant growth in EBITDA in the second half. They face some challenges, however, due to the recent weakening of Sterling and increases raw material prices and the timing of price recovery. This, as well as the uncertainty in commodity pricing means that while they expect their year-end EBITDA to be ahead of last year, there is a risk that it could fall short of current market expectations.

At the current share price the shares trade on a PE ratio of 23.2 which falls to 12.8 on the full year consensus forecast. After a tiny maiden 0.04p interim dividend was announced, the shares are yielding 0.1% which increases to 0.4% on the full year forecast.

Overall then this has been a poor period for the group. The loss widened and net assets declined, not helped by increasing pension liabilities. The operating cash outflow was an improvement but this was entirely due to working capital movements and cash profits declined considerably. The poor performance is apparently due to increased investment costs and commodity price problems in the food ingredients business. Indeed, the cake decorating business is the only one that actually makes any profit and going forward the group is likely to be affected by increasing raw material prices, not helped by the reduction in the value of sterling. I don’t think a forward PE of 12.8 and yield of 0.4% adequately account for this risk and I am not investing in this company yet.

On the 2nd February the group released a trading update covering Q3. The overall trading environment for food manufactures remains difficult with the biggest factors affecting the group being the short term impact of high commodity prices, especially butter, sugar and oils, and a weakening of sterling following the Brexit vote. The cost of butter in particular has more than doubled in price. The timing of these factors was unfortunate as it coincided with the busy Q3 period but notwithstanding this margin pressure, the group remains confident that it will be reporting EBITDA in line with expectations.

Overall sales continue to grow, up 8% in Q3 and they have now implemented targeted price increased and expect margins to be largely restored by the start of the next financial year. This sounds like a short-term issue but conditions are certainly tough at the moment.

On the 5th April the group announced that it is acquiring an 84% interest in Brighter Foods for a total consideration of £9M to be paid in two equal instalments based upon its 2018 accounts. The consideration will be satisfied from the group’s existing debt facilities and is expected to be immediately earnings enhancing.

Brighter Foods creates and manufactures snack bars for the healthy snacking market which are target at areas such as diet control, gluten free, lactose free, no added sugar, sports nutrition, organic and fair trade. They manufacture both partner branded products and their own brands such as Wild Trail which is stocked in major retailers and health stores.

On the 29th June the group released a trading update and the raising of some more capital. It has raised a total of £15.5M of expansion capital from a new investor and two exiting investors by way of debt finance and new equity. The injection of capital will be raised by way of the issue of a secured loan note of up to £8.75M, redeemable after three years. In addition to subscribing for the loan notes, Downing has committed to subscribe to shares equivalent to 10% of the total capital for £2.75M at 35p per share. In addition they have taken out two £2M secured one year term loans from Napier Brown and Omnicane, two current shareholders.

In order to achieve the 2018 budget and take advantage of growth opportunities the group has decided to embark on an expansion plan at Renshaw and Haydens. The two main areas of investment are at Renshaw’s Crown Street site in Liverpool and Haydens in Devizes. Both of these businesses are seeing significant increases in forward demand, driven by international expansion and the launch of a mainstream retail brand at Renshaw and the acquisition of two major new retail customers at Haydens.

At Renshaw the group will invest about £7M in expanding capacity by over 50% as well as the installation of new soft icings sand discs production lines which support the strategy to broaden the offering to mainstream users.

At Haydens the acquisition of two new major customers has put short term pressure on operational capacity and the group will invest about £8M in order to reconfigure site operations including blast freezing capability and the installation of a new automated Yum Yum line. This is expected to take site capacity from £30M revenues to over £50M of revenues. Both of these investments, as well as increasing capacity, bring benefit in efficiency and mitigating the impact of the living wage increases.

The majority of the expansion is expected to be completed by the end of September 2017 at a cost of £15M with the additional capacity expected to start delivering significant returns in 2018. The loan notes carry an interest rate of 6.5% and Downing have been granted the right to appoint a new non-executive director with Judith Mackenzie joining with immediate effect.

This year the group expects to report revenues of £109M and EBITDA of between £5M and £5.4M following the impact on the food ingredients division of the volatile commodity markets and currency fluctuations as a result of the Brexit vote. Net debt at the period-end was £16.2M, partly due to some pre-payments relating to the expansion plan. In the first nine weeks of the new financial year the group has experienced strong growth in revenues across all three divisions.

Sales were up 15% in cake decoration, 9% in premium bakery and 87% in food ingredients following the Brighter Foods acquisition. (like for like sales were up 17%). EBITDA for the same period was 56% ahead.

Overall then, it is a shame that the group has had to raise further equity in order to hit budgets but this should stand them in good stead going forward.

On the 1st August the group announced that during the audit process, two substantial anticipated claims regarding their sugar purchase arrangements have not yet materialised with the effect that it will not meet its previously forecasted profit figures. In addition, the board have concluded that certain development costs, which had previously been capitalised in 2017, should have been expenses. They expect that the total of these adjustments will reduce EBITDA by around £2M in 2017.

As the injection of expansion capital was agreed about three months later than expected, this has resulted in some delay in the implementation of these projects, particularly at Renshaw. This, combined with slightly softer trading conditions in Q1, had adversely affected the board’s expectations for 2018 with EBITDA now expected to be about £2.3M lower than expected.

The board further announces that it has realised that certain payments made to some directors for consultancy services have not been separately disclosed in the related party transaction notes, including £1.2M to Pieter Totte in 2016 (that is quite some consultancy fee!). This has no impact on profit, however.

The group also announced that they had accepted the resignation of non-executive Peter Salter who will step down with immediate effect. Oh dear, what a catalogue of errors. I would suggest that this company shouldn’t be touched with a bargepole until it can sort itself out!

On the 29th August the group released a further update. A review has been undertaken by the new finance director which is expected to lead to additional audit adjustments relating to inter-company trading and consolidation. As a result, the board now expects EBITDA to be in the region of just £1M. They are in discussions with their bankers to vary certain conditions of their banking covenants, which sounds concerning but at least the major shareholders have indicated that they can provide further funds (no doubt diluting other current shareholders) should the need arise. I would not be touching this with a bargepole at the moment.