Vertu Motors has now released its interim results for the year ending 2017.

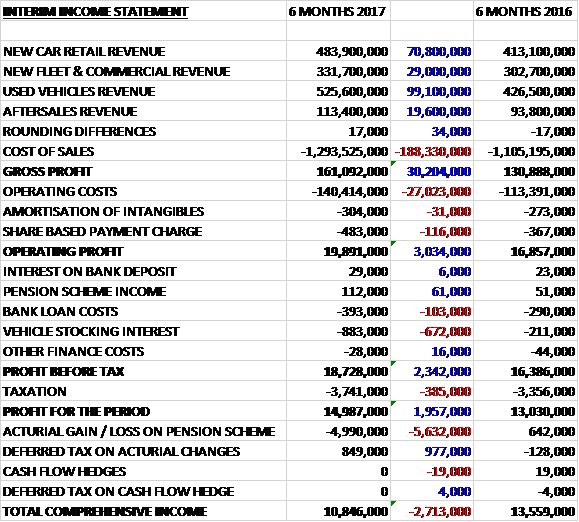

Revenues increased when compared to the first half of last year due to a £99.1M growth in used vehicle revenue, a £70.8M increase in new car retail revenue, a £29M growth in new fleet & commercial revenue and a £19.6M increase in aftersales revenue. Cost of sales also increased to give a gross profit £30.2M higher than last time. Operating costs increased by £27.1M which meant that the operating profit was £3M higher. Bank loan costs were up £103K, vehicle stocking interest increased by £672K due to higher pipeline stocks as new vehicle sales slowed along with the higher number of premium franchise operations which operate with higher vehicle stocking costs, and tax charges grew by £385K, all of which meant that the profit for the period was £15M, a growth of £2M year on year.

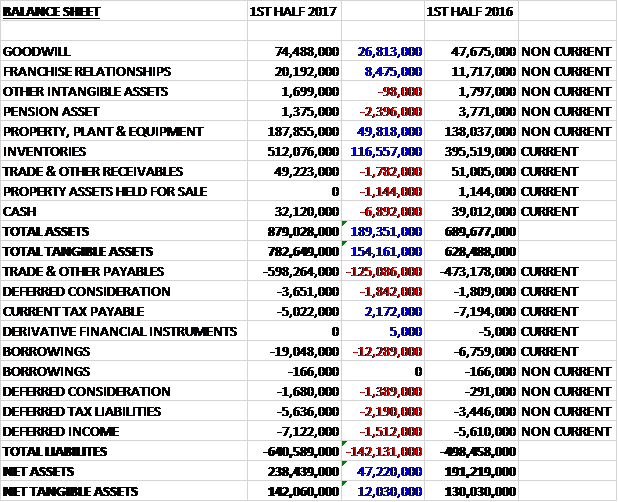

When compared to the same point of last year, total assets increased by £189.4M driven by a £116.6M growth in inventories, a £49.8M increase in property, plant and equipment, a £26.8M increase in goodwill and an £8.5M increase in the value of franchise relationships, partially offset by a £6.9M decline in cash. Total liabilities also increased due to a £125.1M growth in payables and a £12.3M increase in borrowings. The end result was a net tangible asset level of £142.1M, a growth of £12M year on year.

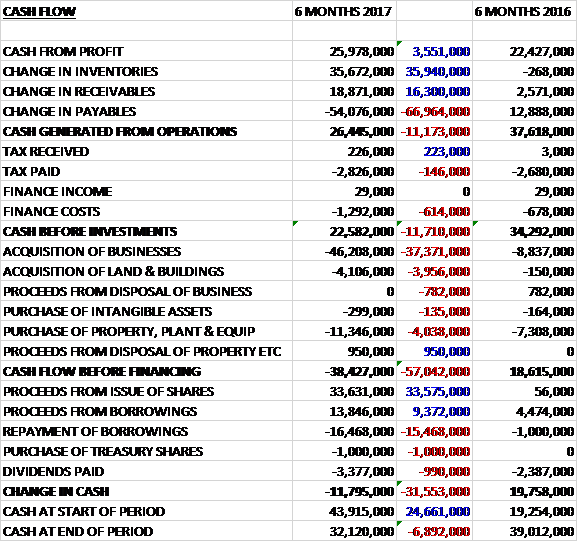

Before movements in working capital, cash profits increased by £3.6M to £26M. There was a small cash inflow from working capital but this was less than last year and after finance costs increased by £614K the net cash from operations was £22.6M, a decline of £11.7M year on year. This covered the £12.3M spent on property, plant & equipment and the £4.1M spent on land and buildings but not the £46.2M forked out on acquisitions so before financing there was a cash outflow of £38.4M. The group spent £3.4M on dividends and paid back a net £2.6M of borrowings so had to issue shares to receive £33.6M. This resulted in a cash outflow of £11.8M for the period and a cash level of £32.1M at the period-end.

After four years of growth, the UK private new retail market softened during the period, recording slight declines in registrations from April onwards which meant that there was a reduction of 0.8% for the period.

The gross profit in the aftersales business was £63.4M, a growth of £12.7M year on year with an increase of 6.8% on a like for like basis. A growing UK vehicle parc and the group’s retention initiatives, particularly the sale of service plans to both used and new car customers, have continued to contribute to these favourable trends. The group now has 97,427 customers paying monthly for their service and MOT through their own service plan products compared to 80,902 last year. In vehicle servicing, like for like service revenues grew by 6.6% with margins increasing as the group achieved higher levels of workshop efficiency as volumes increased.

The gross profit in the used car business was £52.3M, an increase of £10.3M when compared to the first half of last year with a like for like volume growth of 8.5%. This growth was driven in part by the increasing focus on effective marketing, particularly via the promotion of the group’s Bristol Street and Macklin Motors websites, through increasing marketing spend directly online and through TV ads.

In addition to the substantial volume growth the group delivered further used vehicle margin improvements with like for like gross profit per unit up 6.3%. This improvement reflecting strong pricing disciplines, a structured sales process underpinned by training and underlying balance of supply and demand in the wider used vehicle wholesale markets.

The gross profit in the new car business was £35M, a growth of £4.7M when compared to the first half of 2016. This growth was driven by acquisitions with like for like revenues and gross margins stable. UK private new vehicle registrations fell by 0.8% and the group’s like for like new vehicle volumes declined by 4.2%. Increasingly it became evident that as a result of the softening in the new car market, the market was becoming characterised by higher levels of self-registration by retailers with these vehicles registered as retail. These cars are then sold into the retail market as used cars.

The gross profit in the fleet and commercial business was £10.4M, an increase of £2.5M year on year with like for like gross profit up 13.2% and gross profit per unit increasing from £423 to £491. Overall UK registrations in the fleet car channel rose 6.1% whilst group like for like registrations fell 10.6%. This decline in market share reflected fewer deliveries in the low margin supply of vehicles to daily rental companies. This trend reflected the increasing management of used vehicle residual values by the group’s manufacturing partners through reducing overall supply volumes in this low margin channel including seeking to extend daily rental replacement cycles.

The group’s total commercial vehicle sales volume have grown by 13.4% and by 11.6% on a like for like basis. This strength reflects the group’s strong market position in new van supply and the excellent economic conditions in the UK in the period for business. During the period the UK light commercial vehicle registrations grew by 3.9% so the group’s market share has risen.

In March the group acquired Sigma Holdings which operates three Mercedes outlets in Reading, Ascot and Slough. The total consideration amounted to £21.7M including an initial consideration of £8.2M, a £10M bank facility repayable in November 2016 and a further £3.5M deferred over twelve months. This acquisition generated goodwill of £12M and in the prior year the business made a pre-tax profit of £1.2M. The board is pleased with the progress made to date to integrate and improve the performance of the business and they have traded in line with the performance targets put in place at the time of the acquisition.

In May the group acquired Leeds Jaguar from Inchape for £592K settled in cash which generated goodwill of £500K. Last year the business was at breakeven but the Jaguar franchise is currently witnessing a significant turnaround in profitability on the back of new products such as the F-PACE. This business, together with the existing Leeds Land Rover business will shortly be relocated to a freehold dealership in the centre of the city. The property has undergone major redevelopment to house these two businesses and to meet the latest manufacturer standards.

In June they acquired Gordon Lamb which operates the Toyota, Land Rover, Skoda and Nissan outlets in Chesterfield along with the Skoda outlet in Derby. The consideration amounted to £18.8M and generated goodwill of £5.8M with the business generating a pre-tax profit of £2.7M in the prior year. The integration of these businesses has gone well. Derby Skoda is currently in a short-term leasehold property outside of the city and it is planned to relocate this outlet to an existing group location in the centre of Derby in Q1 2017 which will significantly enhance the trading potential of the business and reduce ongoing operating costs.

Also in June the group acquired the freehold and long leasehold interests from Honda in two dealerships operated by the group in Derby and Nottingham for £3.2M. In August they opened the Morpeth Honda outlet alongside an existing Ford outlet. This is the group’s 13th Honda dealership, consolidating their position as Honda’s largest partner in Europe and completing full coverage of the NE market area from Tweed to the Tees.

A further development is nearing completion, the building of a new Nissan dealership in the centre of Glasgow. The group was awarded the whole of Glasgow as a market area for Nissan in April 2015 and the completion of this dealership will see the relocation of the business from a temporary North Glasgow site.

Investment continues to be made in the “Ford Store” concept which sell the full range of Ford product. The group is now reaping the rewards of the investment made in its Birmingham and Orpington Ford store operations. The group’s Gloucester Ford outlet is currently undergoing redevelopment into a Ford store and work will start shortly on a significant Ford store development in Bolton. Further investment has been made in expanding the aftersales capacity of the Ford division with new offsite aftersales facilities now in place at West Brom, Shirley and Orpington.

After the period-end, the group disposed of the Fiat dealership in Newcastle which comprised three sales outlets. In addition, Fiat sales will cease at the group’s sales outlets in Cheltenham and Derby at the end of December 2016 which will leave them with a single Fiat and Alfa Romeo sales outlet in Worcester and no Jeep representation.

The group undertook a £35M equity placing in March to finance further acquisitions and the majority of these funds were deployed during the period.

The group, in common with all sector participants, is in the process of a major programme of capital investment; developing new dealerships, increasing capacity in existing dealerships and responding to manufacturer partner led refurbishments of the existing dealership portfolio. In particular, substantial sums are being invested in increasing capacity and enhancing the retail environment of the JLR dealerships. The group spent £10.2M on this investment during the period with £17.8M expected to be spent in the second half. Next year, the spend is expected to be around £31M with £15.5M expected in 2019. The board is confident that the significant decline in future capital spend in 2019 will drive enhanced free cash flow at that point – up to then it looks like it will be constrained, however.

Following the EU referendum, the result has not materially impacted consumer confidence and the group has not yet experienced any significant change in consumer behaviour. The board believes that the main risks associated with the Brexit vote are significant changes in consumer behaviour and the impact of exchange rates on manufacturer volume strategies and vehicle pricing.

The board are confident regarding the sustainability of their performance in the aftersales and used vehicle market. The latest SMMT forecast for 2016 new vehicle registrations stands at 2.64M compared to 2.63M last year. The market is starting to see vehicle price increases reflecting the manufacturers’ reaction to declining Sterling rates. Lower margin channels such as fleet car supply and motability are likely to see more impact than higher margin channels. In 2017, there is expected to be a decline in registrations of around 6% which would equate to a new car market of around 2.5M units.

Profit in September was ahead of prior year levels on a like for like basis and recent acquisitions further bolstered the result. The service and used car performance continued to demonstrate strong underlying growth trends in September but like for like new car private volumes were down 1.7%, in line with the SMMT registration data. The group’s performance in the key September plate change month was strong and the board expects that full year results will be in line with market expectations.

At the current share price the shares trade on a PE ratio of 8.2 which falls to 7 on the full year consensus forecast. At the period-end the group had a net cash position of £12.9M compared to £23.1M at the start of the period. After the interim dividend was increased by 11%, the shares are yielding 3.1% which increases to 3.2% on the full year forecast.

Overall then this has been a period of progress for the group. Profits were up, net assets increased and although the operating cash flow declined, this was due to reducing payables and cash profits increased. After acquisitions, there was no free cash flow and I am not sure there is going to be enough for the big increase in capex over the next year or so – perhaps that is why the group approached the market for more money.

Aftersales were strong as the group signed up more customers to their service plans, used car sales performed well due to a concentration on more marketing and commercial sales saw a good performance due to the strength of the market in the country. The issue is the new car sales where like for like profits were stagnant. Indeed, since the period-end the market has declined further and is expected to further deterioration going forward. This is likely to be, at least in part, due to Brexit and the depreciation of Sterling.

The shares do seem good value with a forward PE of 7 and yield of 3.2% but the investment hinges on how bad one thinks the UK car market is going to get. I also don’t tend to like companies that have to go to the market for more cash by issuing more equity, I would rather they grow using internally generated cash flows. Overall I think it prudent to wait for some more clarity on the direction of the UK car market.

On the 1st March the group released a trading update ahead of the final results. The board expects trading to be in line with current market expectations with growth in revenues and profits. In the first five months of the year, like for like revenues were up 4.8% with service revenues up 6%. Sales volumes were mixed with a 7.8% increase in used car volumes and a 6.1% growth in new fleet cars being offset by a 9.3% reduction in new car sales, a 10.7% fall in new commercial vehicles and a 4.5% decline in motability vehicles.

In the period, the group’s aftersales focus continued to be on improving customer retention in the vehicle servicing departments through selling service plans to customers buying vehicles. This resulted in continued like for like growth of 6% in vehicle servicing revenues with like for like gross profits up 6.9%.

During the period the SMMT private new vehicle registrations fell by 1.1%. Amongst the group’s manufacturing partners there have been mixed responses to the post-Brexit currency conditions. Some manufacturers maintained prices, supported customer offers and grew market share whilst others have sought to increase prices and reduce consumer offers, losing share as a result. Overall new car prices are reported to have risen by 5.2% in the seven months following the referendum.

Some vehicles registered as retail as measured by the SMMT registration data are then sold to customers as used cars. In these circumstances the group’s new car sales volumes tend to lag the official registration data. Their total new retail vehicle volumes grew by 1.5% but like for like volumes fell by 9.3%. This was partially offset by higher like for like grows margins and like for like profit per unit increased by 6.5% to £1,324, more than offsetting the impact of higher sales prices on margins.

The used car market continued to demonstrate growth, augmented by higher levels of retailer self-registration sales, and continued price stability during the period. The group has continued to invest in increased marketing, as well as maintaining a focus on inventory management and pricing disciplines. As a consequence, like for like used vehicle volumes have increased in the period by 7.8% combined with stronger gross margins at 10.1%. This combination resulted in significantly higher profits generated from used vehicles.

The group’s fleet car business has returned to growth during the period with like for like sales volumes increasing by 6.1%, ahead of the UK market growth of 4.1%. As new car retail volumes have softened, so fleet sales have grown in importance to manufacturers as a distribution channel in the UK.

The UK light commercial van market declined by 1.4% during the period. One of the key drivers of this was the change in diesel engine specification in June to Euro 6. These models are more expensive so many fleet operators accelerated purchases prior to the change so benefiting from advantageous pricing on the run out of Euro 5 models. The group’s like for like van sales fell by 10.7% during the period. The changing mix between car and van sales resulted in a reduction in like for like fleet and commercial margins from 3.3% to 3.1%.

In common with most UK retailers there are several cost pressures facing the group. The main drivers of cost growth during the period have been employment and property related coasts. While they have maintained the ratio of operating expenses to revenue in the period at 9.7%, these pressures will continue with the forthcoming introduction of further taxes such as the apprenticeship levy, increases in the minimum wage rates and well documented rises in business rates. The group is maintaining strong cost control disciplines and a focus on productivity improvement in all areas to seek to mitigate these effects.

Going forward, the SMMT has forecast a fall in 2017 registrations of 5%, taking account of the post-referendum fall in Sterling and the impact on manufacturers who export to the UK. It should be noted that March registrations are expected to be strong. Changes in Vehicle Excise Duty will come into force at the start of April which increase the VED costs over the lifetime of many vehicles so customers may seek to purchase new vehicles before this happens, resulting in a pull forward of registrations into March and weakness in the immediate months afterwards.

The market for aftersales remains strong as the UK vehicle parc has continued to grow following several years of strong new vehicle markets. The board believe that the used car market provides an opportunity to continue to grow profits underpinned by strong consumer demand and pricing stability. The board is therefore confident of the prospects for the group as a whole but are more cautious about the new vehicle market.

Overall then, this is an interesting period for the group. There is no doubt that the new car market is under pressure but this is being offset by strength elsewhere. The cost price pressure are a concern too, and I am not sure how long the group can continue to mitigate this. Tricky one, I am tempted to buy but not sure if we are looking at the start of a Brexit-related downturn in the industry.