Tower Resources has now released its interim results for the year ending 2016.

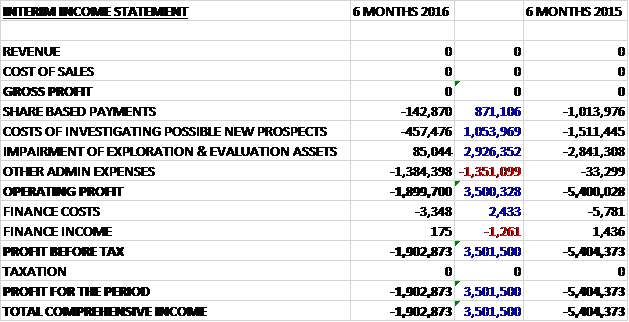

There were no revenues or therefore cost of sales. Share based payments reduced by $871K, costs of investigating possible new prospects declined by $1.1M and there was a small impairment reversal compared to a $2.8M impairment last time. Other admin expenses did increase by $1.4M, however, to give an operating loss $3.5M better than last time. There were no real finance costs or tax charges to speak of so the loss for the period was $1.9M, an improvement of $3.5M year on year.

When compared to the end point of last year, total assets declined by $1.4M driven by a $2.7M decrease in cash, partially offset by a $1.3M increase in the value of exploration and evaluation assets. Total liabilities increased during the period due to a $283K growth in payables and a $54K increase in accruals. The end result was a net tangible asset level of $1.1M, a decline of $3.1M over the past six months.

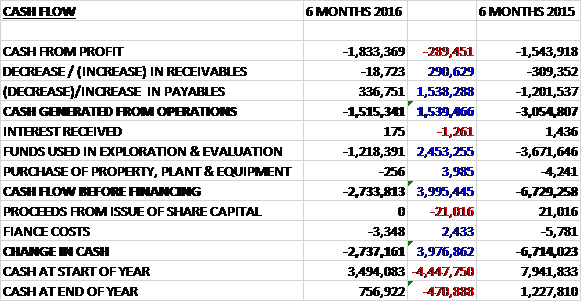

Before movements in working capital cash losses increased by $289K to $1.8M. There was a cash inflow from working capital due to an increase in payables which meant that the cash lost from operations was $1.5M, an improvement of $3.1M year on year. The group spent $1.2M on evaluation and exploration, the vast majority being in Cameroon, but not much else to give a cash outflow of $2.7M before financing. There was little in the way of finance costs so there was a cash outflow of $2.7M in the period and a cash level of $757K at the period-end.

Included in receivables is $1M of VAT due to the company from HMRC. HMRC have withheld VAT repayments pending the completion of an ongoing review. Whilst this review process remains ongoing, HMRC have since issued further assessments totalling £843K in respect of which the group continues to take professional advice.

Following a review, the group have identified that certain suppliers have incorrectly charged UK VAT on their fees totalling £903K. The suppliers concerned have filed letters disclosing this error with HMRC and are seeking reimbursement from HMRC. Settlement of these reclaims in full would mean that the group would be owed a net sum over and above the value of the VAT repayments being withheld, although there can be no certainty of the quantum of the repayment resulting from these reclaims until this part of the consultation has been concluded.

Peter Blackey, non-executive director, retired from the board following the AGM. He was a founder of Tower in 2005.

At the period-end, the group had a cash balance of $757K. Their operations are currently being financed by funds raised from private and public placings of shares and the directors recognise that they will need to raise additional funds within the next few months sufficient to meet their committed capex, although they are confident in their ability to do this.

The group is intending to raise $1.35M through a subscription of about 45.9M new shares at a placing price of 2.25p per share. They intend to make an open offer to raise a further $730K at the placing price. The group are reducing their cost base further but require a modest amount of further working capital to extend cash reserves into Q1 2017as the proceed with the farm out process of the Thali block. The placing represents a very heavy discount of 59% and is very dilutive, representing more than 60% of the enlarged share capital.

In Cameroon the next key step is the acquisition of modern 3D seismic to significantly improve subsurface imaging and resolution as the existing seismic data is 25 years old. A small in-country office has been established in Douala and is currently preparing to acquire a minimum of 100km2 of 3D seismic. To this end they have completed the lengthy ESIA and been granted a certificate of environmental conformity. The group is seeking a partner to cover these costs and the timing of operations will reflect these factors.

In South Africa uncertainty about the new mining legislation and its impact on the oil exploration sector has reduced industry activity to minor levels and it is hoped that this process will be brought to a conclusion in the next few months and provide greater certainty. The prospectivity evaluation is in progress and due to be completed before the end of the year. The group will seek a partner for the next programme of operational activity.

In February the group announced that they had agreed not to proceed with an application to convert the deep water frontier SW Orange Basin TCP into an exploration right. Consequently they were reimbursed by their partner $500K which was paid as part of the original farm in agreement which was also terminated. This allows the group to focus their efforts in South Africa on the Algoa-Gamtoos exploration right which offers greater near term potential.

In Zambia, future work commitments over the next two years potentially include airborne gravity data acquisition and a 2D seismic programme. The licenses can be relinquished at the end of each year if results are discouraging.

The government is working towards a new petroleum code which will give greater clarity. The group will engage with the appropriate ministries once a new cabinet is formed following the recent elections. They will also actively seek a partner for Blocks 40 and 41 so it is carried into the more expensive parts of the work programme and to re-coup an appropriate part of its investment.

On the 24th January the group announced the completion of the sale of Comet Petroleum for a cash consideration of £1, future contingent payments and an over-riding royalty interest of 10% over future production revenue from their assets in the SADR. The group have also completed an amendment agreement to eliminate the previously announced contingent payments due to the original vendors of Comet (former directors of Tower!) who will now share part of the above consideration, leaving an ORRI of between 5% and 10% depending on the asset. The carrying value of the assets in the latest accounts was $484K.

Overall then, the Cameroon assets offer some interest here but given that the group will definitely have to raise more capital and there doesn’t seem to be a queue of other companies looking to farm in to these assets, I don’t think this is any more than a real gamble right now.

On the 12th May the group announced that it had suspended trading on AIM pending clarification of its financial circumstances. They had been in advanced discussions with a potential partner in relation to the Thali asset but a final deadline for signature of a heads of agreement that would have triggered a deposit to the group has been missed. The financial condition and prospects of the company have therefore deteriorated leading to significant uncertainty and current employees have been provided with notice of termination of their employment. The board are now considering alternatives for the group, one of which may be the appointment of administrators. Oh dear, what a sorry tale.