Tristel has now released their interim results for the year ending 2017.

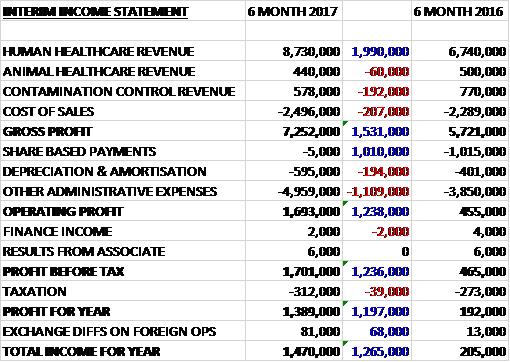

Revenues increased when compared to the first half of last year as a £2M growth in human healthcare revenue was only partially offset by a £60K decline in animal healthcare revenue and a £192K fall in contamination control revenue. Cost of sales grew by £207K which meant that the gross profit was up £1.5M. There was a welcome £1M reduction compared to last year’s vastly inflated share based payment charge but depreciation/amortisation was up £194K and other admin expenses increased by £1.1M (£200K of which related to the proposed entry into North America) which meant that the operating profit grew by £1.2M. Finance income was broadly flat but tax charges increased by £39K to give a profit for the half year of £1.4M, a growth of £1.2M year on year.

When compared to the end point of last year, total assets declined by £1.1M driven by a £1.9M fall in cash and a £122K decrease in inventories partially offset by an £835K growth in intangible assets. Total liabilities also declined during the period was a £217K growth in current tax liabilities was more than offset by a £673K fall in payables. The end result was a net tangible asset level of £7.4M, a decline of £1.5M over the past six months.

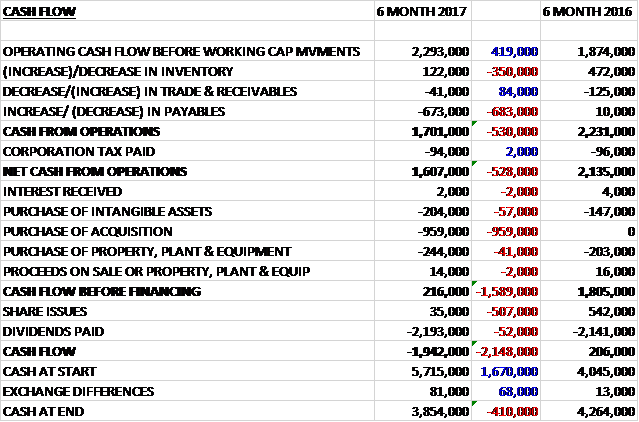

Before movements in working capital, cash profits increased by £419K to £2.3M. There was a cash outflow from working capital, however, with a decline in payables and after tax payments were flat, the net cash from operations was £1.6M, a decline of £528K year on year. The group spent £204K on intangible assets, £244K on property, plant and equipment and £959K on acquiring the Australian subsidiary to give a free cash flow of £216K. This didn’t cover the dividends, however so there was a cash outflow of £1.9M in the period and a cash level of £3.9M at the period-end.

Overall the results came in ahead of management expectations and have benefited from the weakness in Sterling. Sales in the UK picked up the pace of growth with an overall rise of 9%. This performance was flattered by a bulk purchase from the NHS, however, which enabled the substitution of a discontinued pack size and contributed about £150K in sales. Overseas sales were up 45% with nearly 40% of this increase due to the acquisition of the Australian subsidiary (the rest came from China, Germany and New Zealand).

The gross profit in the Human Healthcare division was £6.6M, a growth of £1.6M year on year. Revenues were up nearly £2M with a £732K growth in German revenue, a £584K increase in UK revenue and a £674K growth in ROW revenue.

The gross profit in the Animal Healthcare division was £322K, a decline of £12K when compared to the first half of last year. Revenues declined by £60K, almost entirely due to a fall in UK revenue with ROW remaining flat. The gross profit in the Contamination Control business was £358K, a fall of £41K when compared to the first half of 2016. Revenues fell by £192K with declines in sales to both the UK and ROW.

The group have spent about £200K so far on their North American market entry plan. They have held two meetings with the FDA and one with the EPA, they have attended a number of clinical conferences and trade exhibitions during the period and are in the process of piecing together their market entry plan. The board are satisfied that they are progressing well towards their objective of entering the market in 2019. In August the group acquired Ashmed for a total cash consideration of £1.1M with £959K of this being represented by intangible assets.

At the current share price the shares are trading on a PE ratio of 35.4 which falls to 17.9 on the full year consensus forecast. After a special dividend and a 23% increase in the interim dividend the shares are yielding 3.9% which normalises to 2.1% on the full year forecast.

Overall then this has been a decent period for the group. Although net assets declined and the operating cash flow decreased, the latter was due to movements in working capital and cash profits increased, although not much in the way of free cash flow was generated. Profits certainly increased though, aided by the lack of any share based payments, favourable currency movements and a big one-off order from the NHS. Overseas orders continue to grow, however, and this is a company that may have an exciting future.

In the immediate future, however, with the North American entry still some way off and quite a bit of costs still to come from that and some strong numbers this time that it will be tricky to beat, I think the forward PE of 17.9 is on the high-side. I continue to hold but may reassess if the share price momentum looks to slow down.

On the 7th April the group announced that several directors were selling a lot of shares. Francisco Soler sold 2.5M shares at a value of £4.4M, CEO Paul Swinney sold 689,371 shares at a value of £1.2M and Paul Barnes sold 140,000 shares at a value of £245K. Following the sales, they own 8,413,843; 483,129; and 590,180 shares respectively. This is not a massive vote of confidence… I do rather agree with the directors and think this is getting rather expensive now.

On the 3rd July the group announced that it had made a $750K investment in Mobile ODT, an Israeli company that is combining smartphone technology with hand held devices to make diagnostics available at the point of care. This investment means the group is taking a 3.27% equity stake and several directors are also making personal investments with Tristel also having a seat on the board of directors.

The business has developed the propriety EVA system, a smart phone based medical devise which enables any healthcare provider to examine patients for indications of cervical cancer using a technology known as colposcopy. The product was approved by the US FDA in 2016 and is significantly less expensive than the traditional examination device. The group’s Duo disinfectant foam is intended to be combined with EVA in an integrated offer to healthcare providers.

Also the group has established its presence in the US by incorporating a subsidiary in Delaware. At the end of June they made a submission for regulatory clearance by the EPA of the Duo disinfectant foam. They expect to receive approval in the second half of the year. Following EPA approval they will then need to secure state by state approval before they can start selling Duo.

In addition they continue to develop two submissions to be made to the FDA which will permit Duo to claim high level disinfection of medical instruments. They expect to complete and make these submissions during the first half of 2018. The group continues to develop a further four additional submissions to be made to the EPA during the coming year for other products.

On the 19th July the group released a trading update for the whole year. They will record a record turnover of more than £20M, and pre-tax profits of £4M compared to £17.1M and £3.3M respectively last year, which is ahead of market expectations. In the second half, revenue from overseas markets contributed half of the group total compared to 43% in the first half. The group has continued to generate significant levels of cash and at the year-end, cash balances were £5.1M with not debt. The Australian acquisition announced last year has made a significant contribution to this growth.

On the 17th August the group announced that Finance Director Liz Dixon sold 10,000 shares at a value of £27.3K. This is a bit of a shame, she retains ownership of 45,000 shares.