Character has now released their interim results for the year ending 2017.

Revenues declined by £3.7M when compared to the first half of last year and after amortisation fell by £371K and other cost of sales decreased by £366K the gross profit was down £3M. There was a £659K detrimental movement in the hedging instruments but other admin expenses were down £1.5M which meant that the operating profit fell by £2.2M. Tax charges declined by £513K to give a profit for the period of £5.3M, a decline of £1.7M year on year.

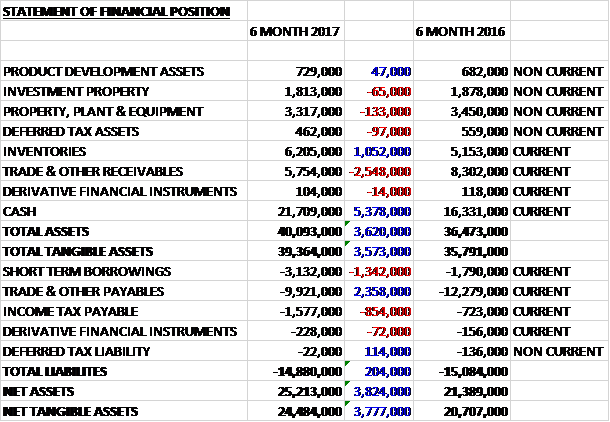

When compared to the end point of last year, total assets increased by £3.6M driven by a £5.4M growth in cash and a £1.1M increase in inventories, partially offset by a £2.5M decline in receivables. Total liabilities decreased during the period as a £1.3M growth in borrowings and an £854K increase in income tax payables were more than offset by a £2.4M fall in trade and other payables. The end result was a net tangible asset level of £24.5M, a growth of £3.8M year on year.

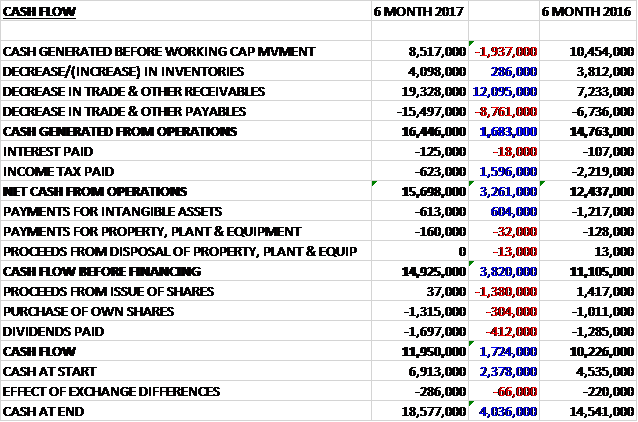

Before movements in working capital, cash profits declined by £1.9M to £8.5M. There was a cash inflow from working capital, however, mainly due to a large decrease in receivables and after tax payments declined by £1.6M the net cash from operations was £15.7M, a growth of £3.3M year on year. The group spent just £160K on property, plant and equipment along with £613K on intangible assets to give a free cash flow of £14.9M. The group then spent £1.3M on their own shares and £1.7M in dividends which left a cash flow of £12M and a cash level of £18.6M at the period-end.

During the period a number of macro-economic factors, particularly the weakness of sterling, have worked against the group as a significant proportion of purchases are made in US dollars. The board have instigated several specific measures to improve operational efficiency to mitigate the adverse effect of increased stock purchase costs arising as a result of the weakness of sterling. Apparently good progress has been made on these initiatives and material cost savings are now coming through.

The top performing brands in the period were Peppa Pig, Little Live Pets, Teletubbies, Mashems, Minecraft, Scooby Doo, Stretch and Fireman Sam. Peppa is consistently the top performing brand with Little Live Pets and Teletubbies rounding out the top three. The recently launched stretch range has already established itself as one of the group’s top brands in the UK and internationally.

As already communicated, the sales levels leading up to the Christmas period were marginally down compared to the same period in the prior year. The group adopted a cautious approach to purchasing stocks in the lead up to Christmas and their sales could have been marginally higher if they had not adopted this approach. Sales in the US were down compared to the first half of last year but the effect on profit was minimal as the margin in US sales is lower than other territories.

A number of new products are currently in development for launch this year across the core ranges – Peppa, Little Live Pets, Teletubbies, Stretch, Mashems and Minecraft. In particular there are a number of exciting developments on the Stretch range which the board believe will create a strong level of sales later this year and beyond. The second half of the year has started in line with budget and the board believe the group is on target to achieve current market expectations for the full year. Although it should be noted that the second half does have to see a considerable improvement to hit these targets.

After a 29% increase in the interim dividend the shares are yielding 3.2% which increases to 3.6% on the full year forecast. At the current share price the shares are trading on a PE ratio of 11.2 which falls to 10.3 on the full year forecast. At the period-end the group had a net cash position of £18.6M compared to £14.5M at the same point of last year.

On the 27th April the group announced that Finance Director Mark Dowding purchased 8,000 shares at a value of £37.6K to give him a total of 108,000 shares. Also, group marketing director Jeremiah Healy purchased 5,000 shares at a value of £23.5K top give him a total of 41,000 shares. Finally the group purchased 75,000 of its own shares for cancellation at a value of £352.5K.

Overall then this was a bit of a disappointing period for the group as profits declined year on year. Net assists did approve, however, and the operating cash flow increased with loads of free cash being generated. This was flattered by working capital movements, however, and the cash profit declined. The group is being affected by the Sterling depreciation as most of the purchases are made in dollars but the group have apparently taken steps to address this. Perhaps more concerning was the slightly lower Xmas sales and the reduction in revenue from the US, the reasons for which are not forthcoming.

Still, the group remains very cash generative and has a big cash pile so the forward PE of 10.3 and dividend yield of 3.6% still looks decent value. I remain a holder but am now more cautious.

On the 14th July the group announced that they have extended their master toy licence for Teletubbies for a further three years. The deal, which runs to 2020, is for worldwide manufacturing rights with UK distribution and will see the group adding further plush and plastic toys to the range. New lines such as Tiddlytubbies will be inspired by new elements from season two which launched earlier in 2017.

On the 6th September the group announced that it had been appointed the master toy distributor in the UK and Ireland for Pokemon. The agreement will see action figures, playsets, plus, role play and other toys based on the series joint their portfolio from summer 2018.

On the 15th September it was announced that, due to a loss of confidence in him by the senior executive team, Mark Dowding’s contract as Finance Director has been terminated and he ceased to be a director with immediate effect. Consequently, the joint MD Kiran Shah will assume the responsibility of Finance Director. This is all a little strange, there is not that much to go on as to whether this is serious or not.

On the 19th September the group announced that it had a solid finish to the year and pre-tax profits are expected to meet current market expectations. Conditions in the wider market remain challenging at the consumer level and one of the group’s major customers, Toys R Us has filed for Chapter 11 bankruptcy protection in North America. At this early stage they do not know the extent to which this will impact trading with them both in the UK and internationally so they don’t have reliable visibility on the important Christmas trading period, which is a real concern. I am not sure if I should look to sell some of these to be on the safe side.

On the 11th October the group announced that their international sales had been adversely affected by a combination of factors, not least the bankruptcy of Toys R Us, and the conservative approach taken by the international customers.

At this early stage in the group’s new financial year, the board considers that group performance for 2018 is now expected to be significantly below current market estimates. The directors consider this to be a temporary downturn and that they anticipate returning to growth during the second half of the year with an improved financial performance in 2019 as they are introducing new products which they believe to be very strong. Even in these tough trading conditions, they expect their cash flow to remain positive.

This is clearly disappointing but not altogether unexpected. I have sold around half my holding given the ongoing uncertainty.