Portmeirion has now released their final results for the year ended 2016.

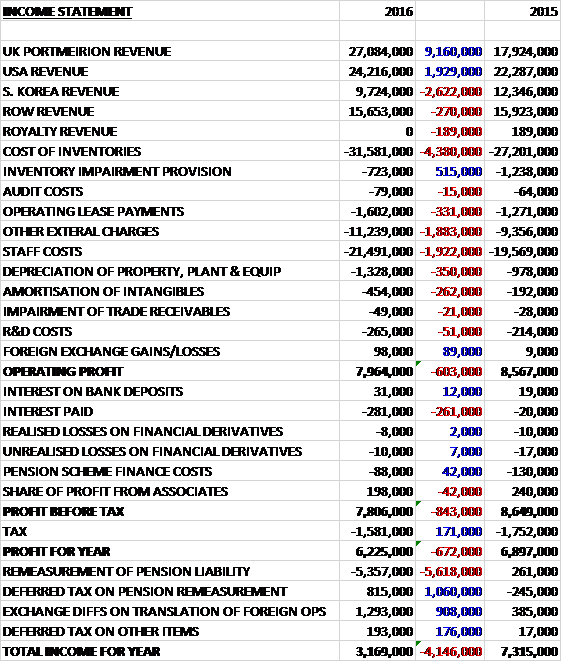

Revenues increased when compared to last year driven by the acquisition and favourable forex movements as a £2.6M decline in South Korean revenues, a £270K fall in ROW revenue and a £189K decrease in royalty revenue was more than offset by a £1.9M increase in US revenue and a £9.2M growth in UK revenue following the Wax Lyrical acquisition. Cost of inventories increased by £4.4M, however, staff costs were up £1.9M and other external charges grew by £1.9M to give an operating profit £603K lower than in 2015. Interest payments increased by £261K but tax charges were down £171K to give a profit for the year of £6.2M, a decline of £672K year on year.

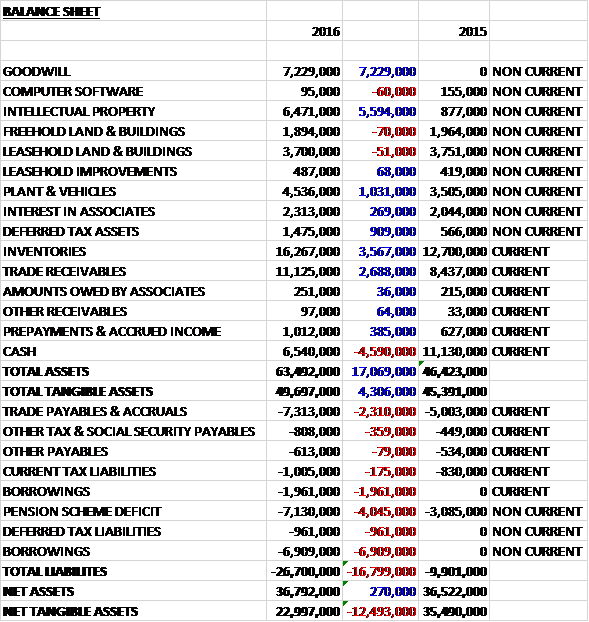

When compared to the end point of last year, total assets increased by £17.1M driven by a £7.2M growth in goodwill, a £5.6M increase in IP, a £3.6M growth in inventories, a £2.7M increase in trade receivables and a £1M increase in the value of plant and vehicles, partially offset by a £4.6M decrease in cash. Total liabilities also increased during the year due to an £8.9M increase in borrowings, a £4M growth in the pension liabilities and a £2.3M increase in trade payables and accruals. The end result was a net tangible asset level of £23M, a decline of £12.5M year on year.

Before movements in working capital, cash profits increased by £124K to £10.1M. There was a broadly neutral working capital position but the group paid out £463K more in contributions to the pension scheme. After tax payments fell by £425K the net cash from operations came in at £6.9M, a decline of £3.8M year on year. The group spent £744K on property, plant and equipment and after £16.7M was spent on the acquisition, before financing there was a cash outflow of £10.5M. The group also spent £3.2M on dividends so took out £8.8M of new borrowings to give a cash outflow of £4.7M and a cash level of £6.5M at the year-end.

The Brexit vote and the US presidential elections were major uncertainties in the two largest markets and South Korea continued to suffer economic problems which resulted in reduced demand for luxury products. Following a big sales increase in India last year, the region did not perform as well this year and returning sales in the country to the higher level will take time.

Like for like sales in the UK increased by just over 2% and the board remain cautious over the effect of Brexit. On a constant currency basis, sales in the US decreased by 3.7% but there are hopeful signs that the economy remains on the upswing despite some doubts remaining over how government policy will affect importers. Own internet sales in the UK and US increased by 31.8% to £3.3M during the year.

Sales into South Korea fell by a further 21% meaning that over the past two years sales have collapsed by £5.4M to £9.7M. The group are working closely with their distributor to try and rebuild sales. Sales in India were just £1.1M, a disastrous year on year fall of £4.7M with the performance of the Indian distributor being very disappointing. The group have therefore changed their distribution arrangements in the country. There were some increases into Europe and some Asian markets such as Hong Kong and Taiwan, however.

In May the group acquired Wax Lyrical for a total cash consideration of £17.5M. The business is the UK’s largest manufacturer of home fragrances and their products include scented candles and reed diffusers. In the prior year the business generated a pre-tax profit of £2.1M and the acquisition generated goodwill of £7.2M. Significant growth opportunities for Wax Lyrical’s products are envisaged within the group’s existing markets and they particularly expect to growth their sales through their existing UK customers, websites and retail outlets. During the period since the acquisition the business contributed £1.5M to profits.

The group have been working on production development. Last year saw new patterns released, of which Strawberry Thief, licensed from Morris and Co, is a good example. In the current year to date, Choices and Sara Miller have been well received amongst a number of new patterns, Wrendale continued to expand and they are pulling home fragrance products into their established ceramic ranges as they tie in more closely to Wax Lyrical.

The new kiln came on line just a few weeks before the board saw the reality of falling demand from India and South Korea. It has helped relieve a bottleneck, however, with the existing glost kiln, it is more efficient than the existing tunnel kilns and significantly more fuel efficient than the four intermittent kilns that they have had to use during high throughput periods. Average weekly production has been 130,000 and clearly putting more volumes through the factory would be a marginal cost benefit with a great effect on profits.

Trading in the first two months of 2017 was marginally ahead of the prior period on a like for like basis and 20% ahead including Wax Lyrical with the outlook positive and the issues experienced being overcome by proactive management.

At the current share price the shares are trading on a PE ratio of 14.7 which falls to 13.1 on next year’s consensus forecast. After a 7.5% increase in the total dividend the shares are yielding 3.7% which increases to 3.8% on next year’s forecast. At the end of the year the group had a net debt position of £2.3M compared to a net cash position of £11.1M at the end of last year.

Overall then this has been a difficult year for the group. Profits declined despite the additional contribution from Wax Lyrical, net assets decreased and the operating cash flow fell, although excluding the acquisition, the group remained fairly cash generative. The UK held up fairly well but the other main markets fared less well. South Korea and India in particular suffered particularly bad times. Hopefully the change in the distribution network will help the latter but there doesn’t seem to be much evidence of ideas in turning South Korea around.

The new year has started a bit better but until some real evidence of a turnaround in the core business has cropped up, I find it hard to buy back in here. The forward PE of 13.1 and 3.8% both look OK, however, and I have confidence that at some point this will look like good value.

On the 25th May the group released an AGM statement. Total group sales are up 26% in the first four months of the year and excluding Wax Lyrical on a translated currency basis total group sales are comfortably ahead of last year but on a constant currency basis they are flat. The board continue to expect pre-tax profit to be in line with market expectations for the full year.

On the 7th July the group released a trading update covering the first half of the year. Total group sales were up 16% but excluding Wax Lyrical sales, and at constant currency, they declined by 2%. Profit is still expected to be in line with market expectations, however.