Orosur has now released their Q3 results for the year ending 2017.

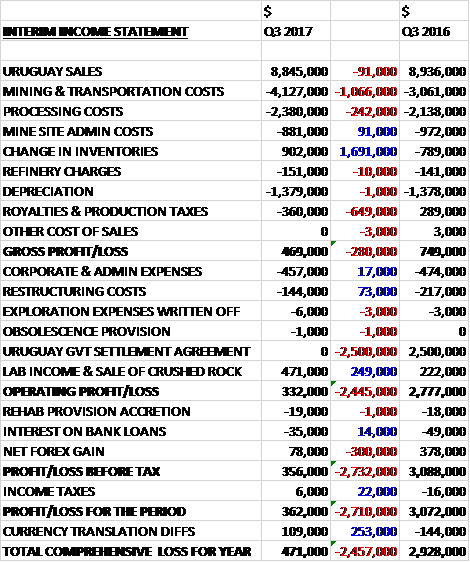

Revenues were broadly flat when compared to Q3 last year as a small increase in the price achieved was offset by a reduction in the quantity of gold sold but a $1.7M favourable movement in inventories was more than offset by a $1.1M increase in mining and transportation costs, a $649K growth in royalty taxes and a $242K increase in processing costs which meant that the gross profit declined by $280K. There was a $249K growth in lab income and other income, including the sale of a drill rig, and restricting costs fell by $73K but there was no Uruguay government settlement agreement which brought in $2.5M last time so the operating profit was down $2.4M. The net forex gain decreased by $300K which gave a profit for the period of $362K, a decline of $2.7M year on year.

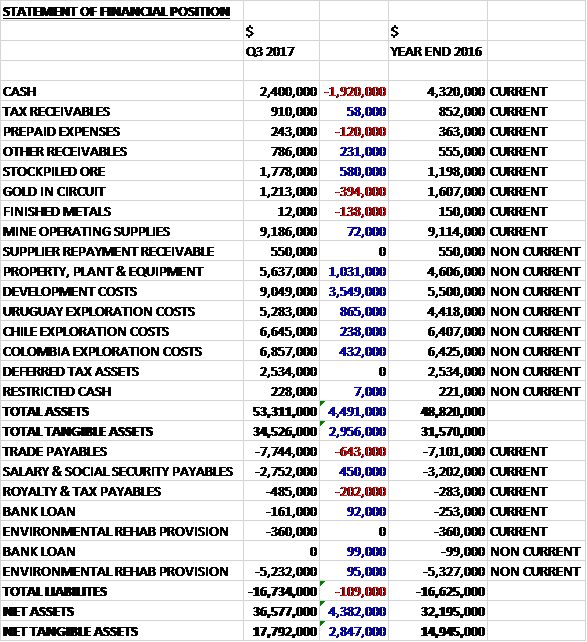

When compared to the end point of last year, total assets increased by $4.5M driven by a $3.5M growth in development costs, a $1M increase in property, plant and equipment and a $1.5M growth in exploration costs capitalised, partially offset by a $1.9M reduction in cash. Total liabilities increased modestly as a $450K decline in salary payables was more than offset by a $643K growth in trade payables. The end result was a net tangible asset level of $17.8M, a growth of $2.8M over the past nine months.

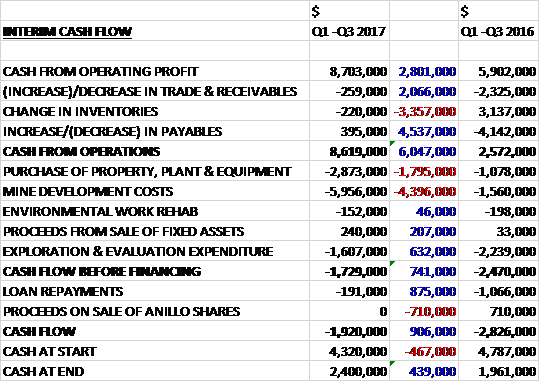

Before movements in working capital, cash profits increased by $2.8M to $8.7M. There was a modest cash outflow from working capital but this was much less than last time so the cash from operations came in at $8.6M, a growth of $6M year on year. The group then spent $2.9M on property, plant and equipment; $6M on mine development costs; and $1.6M on exploration and evaluation expenditure to give a cash outflow of $1.7M before financing. The group repaid $191K of loans to give a cash outflow of $1.9M for the nine month period and a cash level of $2.4M at the period-end.

This quarter has seen the commissioning of the SGW UG new mine. Availability of services such as water, power, access and ventilation have been implemented with about 60% of gold production for the quarter coming from the mine in its first quarter of production. Typically ore production and operational efficiencies are lower at the start of any new mine due to the low operational flexibility given the lack of available production stopes. As the mine development advances, efficiency is expected to improve and the company expects to see improvements as early as Q4.

Production for the quarter was 7,820 ounces of gold compared to 7,274 ounces in Q3 2016 as the lower grade ore processed during the quarter was offset by additional tonnes of ore being processed. The year to date production of 24,623 ounces is in line with expectations to reach the lower end of the group’s 35,000 to 40,000 ounce production guidance for the year. Some 226,193 tonnes of ore was processed at a grade of 1.15g/t compared to 194,352 tonnes at 1.24g/t in Q3 last year.

The average gold price realised for the quarter was $1,198 per ounce compared to $1,143 last time. The average operating cash cost was $858 per ounce compared to $803 last with the increase primarily due to higher mining and processing costs relating to additional tonnes transported and processed at lower grades. As a result of the additional capex associated with the SGW underground mine, including ramp, access and ventilation shaft work, all in sustaining costs increased from $978 per ounce to $1,289 per ounce, although this is lower than the $1,345 per ounce peak in Q2 2017.

The company’s forecast production guidance for the year remains between 35,000 ounces to 40,000 ounces at operating cash costs of between $800 to $900 per ounce. As previously announced, the group incurred higher unit costs during the transition and start of operations in the San Gregorio underground mine which are expected to decrease in Q4 given progress in the mine’s development.

During the quarter the group continued with investment related to the construction of the ramp, access and ventilation shaft at San Gregorio. In addition, they completed construction of phase 4A of the tailings dam.

Exploration drilling in and around the San Gregorio UG area has yielded positive results, intersecting gold mineralisation in every hole, which is expected to significantly enhance mine economics and increase reserves in the short and medium term. Further drilling is underway and ongoing. In Colombia the group finalised a geological model of its high grade Anza gold project to determine the exploratory potential. The project includes a gypsum mine which has environmental and mining permits granted by the Colombian authorities. As previously announced the group has taken over ownership of the mine. The gypsum permits can be readily expanded for additional tonnage, providing the ability for the group to fast track permitting for future gold mining operations.

In December Gladiator publicly announced that it had executed a binding agreement with a third party to dispose of its interest in the project in Uruguay and in February, without Orosur’s consent, they completed the sale of the interest to Metamila, a Belize-based company. The group considers this a breach of contract and intends to take all steps necessary to remedy the situation.

As of the period-end the group had $2.4M of cash with a $1.5M committed and undrawn line of credit with Santander also available. The group remains committed to developing SG UG without any external funding.

There was a loss last year but this year’s consensus forecast is showing that the shares are trading on a forward PE ratio of 2.5.

Overall then this has been a period of change for the group as the new mine was commissioned and started producing. Profits were down marginally even when last year’s Uruguayan government settlement was excluded but net assets increased along with the operating cash flow (although this was for Q1 to Q3 as no Q3 figure was included which makes me think it probably fell). No free cash was produced during this period.

The $1,198 per ounce price achieved is better than last year but doesn’t count the $1,289 AISC. This will come down going forward, however, as the mine starts to get into its groove. The lower grade is a bit concerning and is something that should be watched going forward. The forward PE of 2.5 seems to price in a lot of uncertainty, however, so these shares could be a risky value play I think.

On the 20th June the group released an update covering the year ended 2017. They have produced 35,371 ounces of gold with production in Q4 in line with expectations(initial guidance 35-40K ounces so at the below end of the guidance). The operating cash cost guidance of $800 to $900 per ounce guidance has been confirmed and the net cash at the year-end was $2.9M.

As far as exploration is concerned, in Uruguay the group is extended its mine life with a focus on the Central and East areas of SG UH. A consultant has been engaged to prepare a scoping study covering an expanded project which will include the neighbouring deposits of Veta Sur, Ombu and Veta A.

The deadline for Asset Chile to make its decision to finance Phase 2 in Anillo has been extended to December 2017. They are expected to cover the corporate and ongoing costs until then, estimated at $150K. Under the extension agreement, the group is now able to have open discussions with alternative partners to progress Anillo in the event Asset Chile do not elect to fund phase 2. The group plan to start a 15Km-30Km drilling campaign in Colombia.