AG Barr has now released their final results for the year ended 2017.

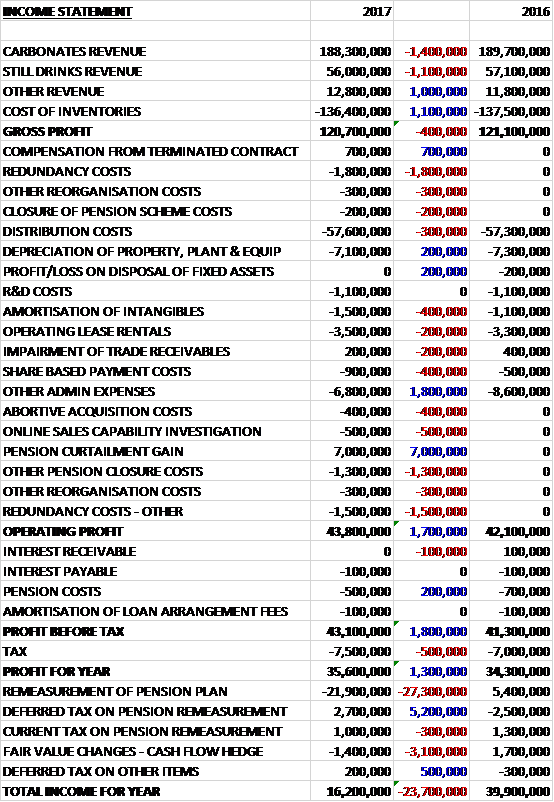

Revenues declined when compared to last year due to the extra week in 2016, with a £1.4M fall in carbonates revenue and a £1.1M decline in still drinks revenue, partially offset by a £1M growth in other revenue. Cost of sales also fell during the year to give a gross profit £400K below that of 2016. The group did get £700K in compensation from a terminated contract but suffered £1.8M of redundancy costs and fairly modest growth in distribution costs, amortisation, operating lease costs and share based payments, counteracted by a small fall in depreciation and a £1.8M decline in other admin expenses. We then see a £7M gain from the curtailment of the pension scheme offset by a £400K abortive acquisition cost, a £500K online sales capability investigation, £1.3M of other pension closure costs and £1.5M in other redundancy costs which meant that the operating profit grew by £1.7M. Finance costs fell somewhat, but tax charges increased by £500K to give a profit for the year of £35.6M, a growth of £1.3M year on year.

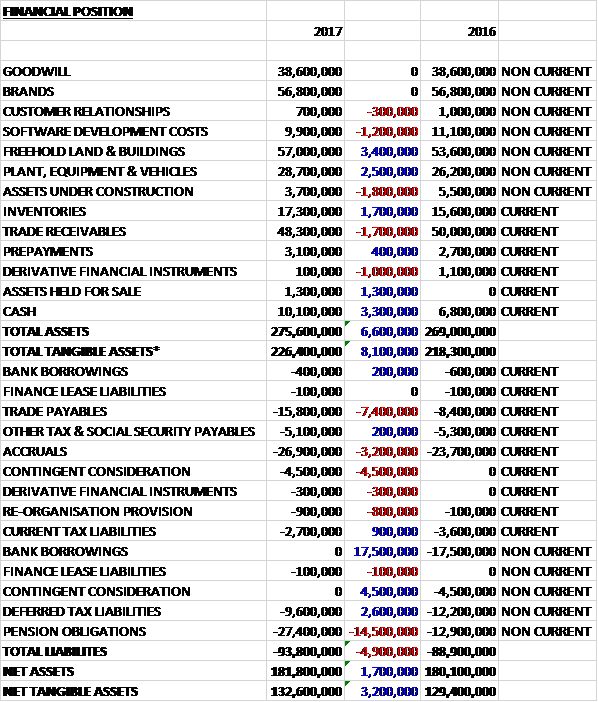

When compared to the end point of last year, total assets increased by £6.6M driven by a £3.4M growth in freehold land and buildings, a £3.3M increase in cash, a £2.5M growth in plant, equipment and vehicles, a £1.7M increase in inventories due to advance purchasing of mangos following a good harvest, and a £1.3M growth in assets held for sale, partially offset by a £1.8M decrease in the value of assets under construction, a £1.7M decline in trade receivables, a £1.2M fall in the software asset and a £1M decrease in the value of derivative financial instruments. Total liabilities also increased during the year as a £17.7M decline in bank borrowings, and a £2.6M fall in deferred tax liabilities were more than offset by a £14.5M increase in pension obligations, a £7.4M growth in trade payables due to the timing of the year-end, and a £3.2M increase in accruals. The end result was a net tangible asset level of £132.6M, a growth of £3.2M year on year.

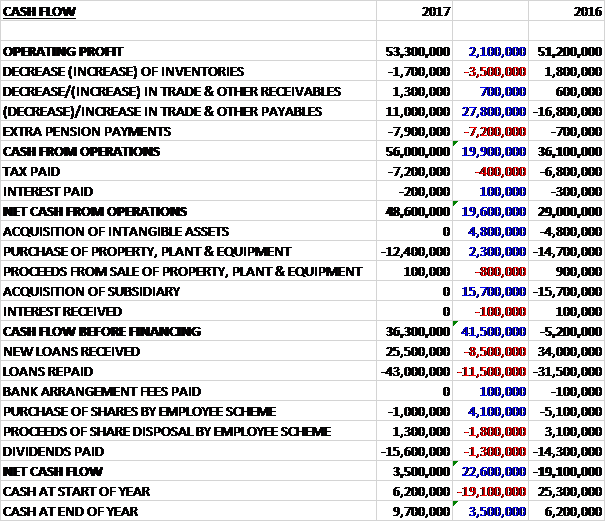

Before movements in working capital, cash profits increased by £2.1M to £53.3M. There was a cash inflow from working capital due to the increase in payables and even after £7.2M of extra pension payments the net cash from operations came in at £48.6M, a growth of £19.6M year on year. The group spent £12.4M on property, plant and equipment which meant that the free cash flow was £36.3M. Of this, £15.6M was spent on dividends and there was a net £17.5M repayment of loans to give a cash flow for the year of £3.5M and a cash level of £9.7M at the year-end.

The announcement of a soft drinks sugar tax and the devaluation of Sterling following the Brexit vote added additional headwinds in a soft drinks market already impacted by price deflation. The group maintained their market share across the period and the launches of IRN-BRU XTRA and Rubicon spring in particular, both no added sugar products, have proved successful.

The UK soft drinks market performed robustly over the past year with growth of 1.2% in value and 1.6% in volume. This total market position masks a higher degree of volatility than in prior years, however. Deflation has eased across the latter part of the year but the continued growth of the lower value water category has continued to impact the total market. Stills experienced volume growth of 3% and value growth of 1%, with water growth continuing to be the driving force. In contrast, the carbonates sector experienced modest inflation, growing value by just over 1% verses a flat volume position.

The gross profit in the Carbonates division was £97.3M, a decline of £1.3M year on year. The core business performed well, with both the IRN-BRU and Rubicon brands growing through a combination of innovation and distribution gains. The portfolio carbonates such as Barr, Tizer and KA have been impacted by retailer range reduction activity, however. The Rockstar brand delivered lower revenues due to competitor discounting and distribution reductions in several supermarkets. The second year of the Snapple partnership has seen success both in the UK and internationally with the new branding and reduced sugar offerings being well received by customers.

The gross profit in the still drinks division was £17M, a decline of just £100K when compared to last year with the new Rubicon light and fruity range performing well. There were, however, continued market-wide challenges in fruit juices and fruit drinks, however, with water remaining a very price competitive subcategory. The international business delivered double digit revenue growth through brand development in the established core markets, new distributor arrangements in existing markets and the opening up of new markets.

The gross profit in the Other division which includes Funkin cocktail and ice creams was £6.4M, a growth of £800K when compared to 2016. The Funkin business performed strongly with sales growth of 27%. The key on-trade business has grown in each of its product segments and the brand is on track to launch its first consumer retail product in Spring 2017. On the basis of the results and the achievement of agreed performance targets, there will be an associated cash earn out payment in 2018 which has been fully provided for.

In September the group signed a further exclusive extension with Rockstar for a further seven territories, including Russia. The Snapple brand has enjoyed growth of over 20% across the year with significant product innovation, packaging changes and further distribution growth in the UK and internationally.

The group have continued to invest in their asset base, including the installation of a new glass filling line at Cumbernauld, and are in the process of adding new PET capability at the Milton Keynes facility. The disposal of the Walthamstow site was completed in February after the year-end. The site sold for £3.8M, generating a gain on sale of £2.5M. The group have entered into a short term lease of the premises as they finalise their long-term plans for direct customer deliveries in the area.

A company-wide reorganisation took place during the period with the employee base reducing by around 100 at a one-off costs of £3.3M. This will generate ongoing savings of around £3M per annum. The majority of the redundancies have taken place and an element of the savings has been delivered this year.

The board has decided to return up to £30M to shareholders via an on-market share repurchase programme with his expected to start in spring 2017 and complete within two years.

There were a large number of “one-off” costs this year. There was £400K of acquisition fees incurred in relation to an unsuccessful acquisition; £500K of advisory costs have been incurred as part of a strategic review of the market threats posed by new and emerging digital trading models (this is stretching the term one-off in my opinion); £600K of redundancy costs were incurred, arising from a reorganisation of direct sales routes and a further £2.7M of redundancy costs were incurred following the announcement of a company restructuring,. Offsetting this was a £7M curtailment gain following the closure of the pension scheme to future accrual, itself partially offset by £1.5M of costs incurred in relation to the closure, including £1.3M of past service costs for one year’s additional service negotiated with the active members of the scheme.

At the current share price the shares are trading on a PE ratio of 25.3 which falls to 21.6 on next year’s consensus forecast. After an increase in the dividend the shares are yielding 2.2% which increases to 2.3% on next year’s forecast. At the year-end the group had a net cash position of £9.7M compared to a net debt position of £11.3M at the end of last year.

On the 3rd April the group announced that commercial director Jonathan Kemp sold 4,000 shares at a value of £23.3K.

Overall then this has been a mixed year for the group. Profits did rise but this seems to be as a result of the pension curtailment gain and underlying profits declined. Net assets did rise, however, as did the operating cash flow with oodles of free cash being generated. The overall market for soft drinks has been OK but the sugar tax and depreciation of Sterling have both been unhelpful. The carbonates division suffered from customers trimming their ranges which meant less sales for some of the more niche drinks the group produces.

The stills division was broadly flat but Funkin still saw some good growth. The board have signalled that they will return some £30M to shareholders which should support the share price, and this is still a quality, cash generative business – just the type of share I like to own. The valuation looks a bit steep to me though with a forward PE of 21.6 and yield of 2.3% not looking that good.

On the 24th July the group announced that non-executive director Pamela Powell purchased 5,000 shares at a value of £30K.

On the 25th July the group announced that Chairman John Nicolson purchased 6,000 shares at a value of £36K.

On the 2nd August the group released a trading update covering the first half of the year. A strong first half sales performance was supported by last year’s new product launches. Revenues is expected to increase by 8% against a market backdrop that saw an increase of 3.5%. They increased their investment in support of brand growth. This, combined with slightly later than expected phasing of price increases and higher operating costs, including the effect of the weakening sterling, had a moderate impact on margins during the period.

While the wider economic environment continues to be uncertain, the board remain confident they will deliver a full year performance in line with expectations.