Telford Homes have now released their final results for the year ended 2017.

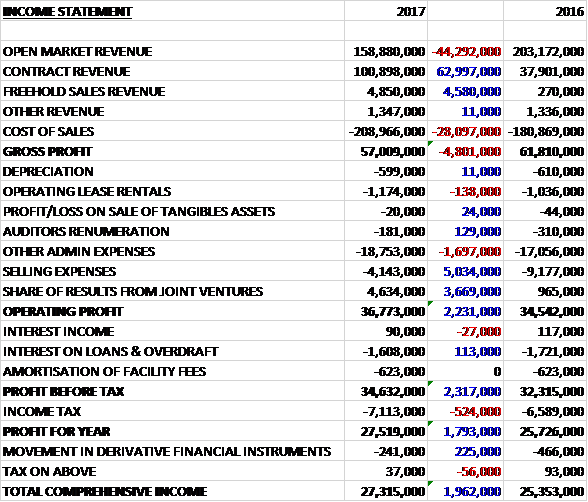

Revenues increased when compared to last year as a £44.3M decline in open market revenue was more than offset by a £63M growth in contract revenue and a £4.6M increase in freehold sales revenue. Cost of sales also increased, however, and gross profit declined by £4.8M. Admin expenses increased by £1.7M, mainly due to higher employee costs, but selling expenses fell by £5M due to the move towards build to rent contracts and less open market sales, and the share of profits from joint ventures increased by £3.7M to give an operating profit £2.2M higher. Loan interest declined by £113K but tax charges grew by £524K to give a profit for the year of £27.5M, a growth of £1.8M year on year.

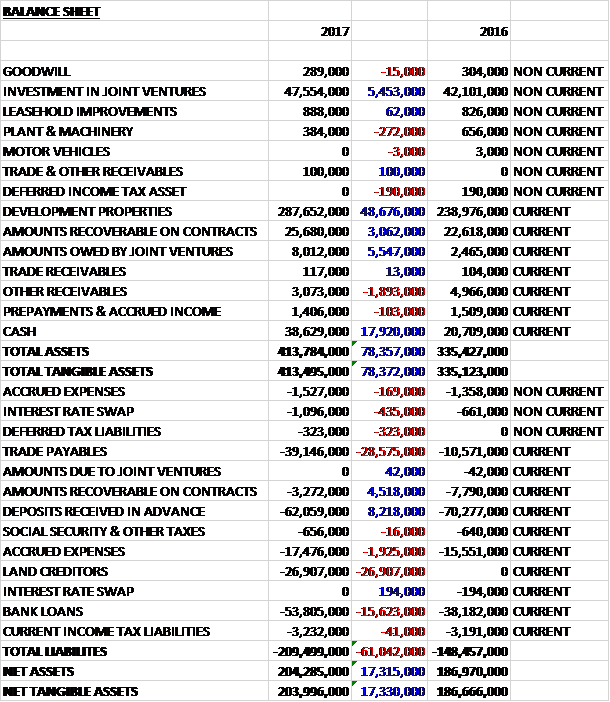

When compared to the end point of last year, total assets increased by £78.4M driven by a £48.7M growth in development properties, a £17.9M increase in cash, a £5.4M growth in investments in joint ventures, a £5.5M increase in amounts owed by joint ventures and a £3.1M growth in amounts recoverable on contracts, partially offset by a £1.9M decline in other payables. Total liabilities also increased during the year as a £28.6M increase in trade payables, a £26.9M growth in land creditors relating to a development site where the group has exchange contracts with completion due on vacant possession of the site expected in the next few months, and a £15.6M increase in bank loans was partially offset by an £8.2M decline in deposits received in advance and a £4.5M fall in amounts recoverable on contracts. The end result was a net tangible asset level of £204M, a growth of £17.3M year on year.

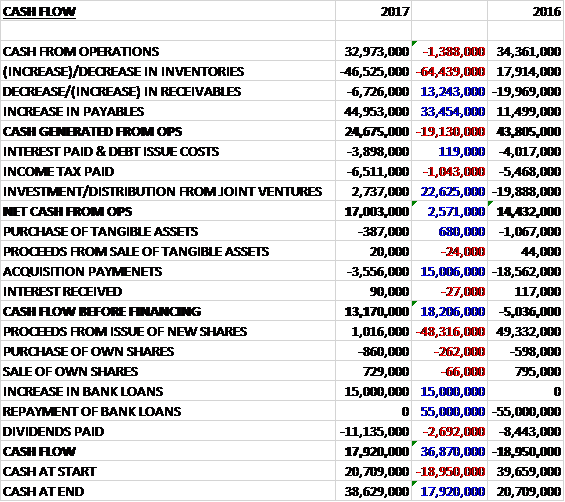

Before movements in working capital, cash profits declined by £1.4M to £33M. There was a cash outflow from working capital, mainly due to a big increase in inventories and after tax payments increased by £1M and there was a £22.6M positive swing to a cash distribution from joint ventures, the net cash from operations came in at £17M, a growth of £2.6M year on year. The group spent £387K on tangible assets and £3.6M on acquisition payments to give a free cash flow of £13.2M. There was a £15M increase in bank loans which helped pay for the £11.1M of dividends which meant that there was a cash flow of £17.9M and a cash level at the year-end of £38.6M.

Despite uncertainty in relation to the outcome of the EU referendum and tax changes impacting primarily UK based individual investors, the underlying market has remained resilient. Any potential dampening effect of these factors has been outweighed by the structural imbalance between supply and the need for new homes in London. Although the Brexit result created a degree of uncertainty, this has not to date been a significant cause for concern for the group. They chose to defer launches for a short period but demand remained buoyant and neither have they seen significant pressure on labour availability or materials due to the result. They will continue to monitor the negotiations with the EU, looking for assurances as soon as possible on the rights of EU workers to remain in the UK.

Sales to overseas investors remained robust. They have seen particular success over the last three years in selling to investors based in China. This is despite any tempering of demand in relation to leaving the EU or the additional 3% stamp duty, both of which have been offset by favourable movements in exchange rates. They have, however, seen a reduction in the number of UK based investors, who have been deterred by the increase in stamp duty and the reducing ability to benefit from tax relief on mortgage interest. The board believe that the attractive yields brining institutional investors into the market should also encourage individuals to invest again once their confidence returns.

The group’s customer mix has moved significantly towards institutional build to rent investors, with this sector representing 77% off sales generated compared to 24% last year. Individual investors accounted for 20% with owner-occupiers at just 3%. In total the group exchanged contracts for the sale of 501 open market properties. Unless they are cash buyers, owner-occupiers are typically unable to purchase more than six months ahead of completion but over the last few weeks the group have launched the residual availability at Bermondsey Works, leading to 22 owner-occupier reservations, most of which were purchased under the government’s help to buy scheme.

The group have seen robust demand from individual investors underpinned by a thriving rental market, including a number of repeat purchases. The last significant launch to individual investors was the second phase of City North in Finsbury Park in November 2016 which secured 73 new sales for a combined value of over £43M. Subsequent to this, developments that could have been more widely launched for sale have instead been sold to build to rent investors as part of the new strategic focus.

The number of open market residential completions was lower than the prior year at 289 (482) but the average selling price was higher at £531K (£417K). The reduction in completions is down to availability of finished stock with fewer units available. The increase in average price is a function of the mix of developments completing in each year in terms of product and their location with relatively modest price inflation.

The reduction in open market completions was more than offset by an increase in both subsidised affordable housing revenue and build to rent revenue recognised in the year. They exchanged contracts to deliver 400 affordable homes (87) and entered into three new build to rent contracts to deliver 387 build to rent homes (156) over the next few years.

During the year the group sold one small undeveloped site for £5M as a result of a change in strategic direction where smaller sites have become less attractive to build out and the group is able to leverage its greater size to focus on larger scale developments. The group has also continued its programme of disposing of older freehold assets generating revenue of £4.9M.

The decrease in gross profit margin was as expected. The margin achieved on open market completions fell from 27.3% to 25.4% but remained above the target of 24% when appraising new sites. The margin is expected to trend down towards the target margin over time as older developments which benefitted from more significant sales price inflation and minimal build cost inflation are replaced with sites appraised more recently.

Also, a greater proportion of the revenue this year is generated from build to rent contracts which attract a lower gross margin to compensate for the advantages of being forward funded. The group expects build to rent transactions to achieve a gross margin of around 12.5% which represents the 24% target margin less savings in selling expenses and interest costs of around 8% for a net difference of 4% offset by an improved return on capital. The margin achieved on the build to rent revenue this year was well ahead of the target at 16% due to some land being purchased at more advantageous rates prior to becoming part of the build to rent portfolio. Future margins are expected to be closer to the target.

The group increased their presence in the London build to rent sector over the last year. Since February 2016 they have entered into four build to rent transactions comprising nearly 500 homes, together worth over £230M. In December they exchanged contracts for the sale of the Forge to M&G Real Estate. The sale consisted of the freehold interest in the land and construction of 125 homes for £48.6M. This was the third build to rent transaction, and the second with M&G. At the end of March, their joint venture, Chobham Farm North, exchange contracts on their fourth significant build to rent transaction. Contracts were exchanged for the sale of 112 of the 297 open market homes at New Garden Quarter for a consideration of £53.7M. The sale to Notting Hill Housing, was for the first phase of open market homes at this development and removed the need for debt finance.

As well as the focus on increasing their presence in build to rent, the group are expanding their geographical reach beyond their historical heartland of boroughs in the East of London. An example of this is the South Kilburn site in partnership with Brent, a borough in which they have not previously developed.

In 2015 the group acquired the regeneration business of United House Developments. Completion of one of the developments, Gallions Quarter, was conditional on the business securing a legal interest in the site. In July 2016 those conditions were met and the group completed the acquisition of Gallions Quarter for a consideration at that time of £3.6M. Revenue and profit recognised since the acquisition are minimal and not significant to the group.

In February 2017 the group added to the pipeline with the acquisition of a sizeable development site, the former London Electricity Board building, for £30.2M. The anticipated gross development value of the site is about £95M. Subject to planning permission, the group expect to start work on site in 2018 to finish in 2021. After the year-end they have exchanged contracts to acquire Stone Studios in Hackney Wick for 120 homes plus commercial space, and been selected as the preferred partner of Brent to develop 236 homes in South Kilburn. Both sites have full planning consent and they expect to start on the site later this year.

Going forward, the board expect that over the next few years build to rent could represent as much as half of their total revenue pipeline. They are comfortable with the development pipeline and have avoided acquiring land at inflated prices. Prospects spanning a variety of locations are being evaluated on an ongoing basis and in greater numbers than last year. Over 80% of the expected gross profit for 2018 has been secured and they are on track to deliver over £40M of pre-tax profit.

The group start the new financial year with an order book of future sales £33M lower than last year at £546M. Following some recent land acquisitions, the development pipeline stands at £1.5BN of future revenue and the average anticipated price of the open market homes in the pipeline is £527K, up from £513K. The board expects 2018 to show significant growth in pre-tax profits with more growth the following year.

At the current share price the shares are trading on a PE ratio of 10.8 which falls to 8.4 on next year’s consensus forecast. After a 10% increase in the total dividend the shares are yielding 4% which increases to 4.3% on next year’s forecast. At the year-end, net debt stood at £14.3M compared to £17.3M at the end of last year. Gearing is expected to increase to enable the growth expected over the next few years.

On the 5th June the group announced that it has signed a pre-construction development agreement with Greystar, a global real estate company, to deliver 894 build to rent homes, together with extensive facilities at Nine Elms in Battersea. The pre-construction development agreement means that the group will assist Greystar in pursuing a detailed planning consent for the site. Once consent has been secured, the pre-construction development agreement will lead to Telford Homes entering a full design and build contract with Greystar to deliver the development for a fixed price.

On the 8th June the group announced that Planning and Design Director David Durant sold 375,000 shares at a value of £1.5M. This is quite a hefty sale!

On the 13th July the group released an AGM trading statement. Since they reported their final results, they have achieved further momentum in the build to rent sector and they are assessing a number of new development opportunities to add to the pipeline. They are still on track to achieve £40M of pre-tax profit in 2018 and £50M in 2019. They expect less than a quarter of the forecast open market handovers for the year to occur in the first half, however, and as a result full year profits will be significantly weighted to the second half. Whilst there is some political and economic uncertainty, the group is hopeful of greater stability in the months ahead.

Overall then this has been a decent year despite the turmoil surrounding the Brexit vote. Profits were up, net assets increased and the operating cash flow grew with dividends being covered by free cash flow. Investor demand remains robust from overseas despite the headwinds from stamp duty increases etc and the decline in open market completions was offset by increases in affordable homes and build to rent.

Margins are declining but the group is on track to increase profits this year and next. I am a bit concerned about the AGM comment surrounding the current uncertainty, and indeed there is uncertainty in the market but a forward PE of 8.4 and yield of 4.3% seems to compensate for this. I remain a holder.

On the 11th October the group released a trading update covering the first half of the year. Despite the underlying need the homes for sale market in London has been somewhat subdued by economic and political uncertainty around Brexit negotiations and the election outcome. This has mainly affected demand at higher price points and tax changes affecting buy to let investment have also reduced the number of UK based investors that are active in the market.

The group has experienced limited impact from the market uncertainty to date due to the lower average price point and sales to build to rent investors. They have a development pipeline of over 4,000 homes to be delivered across London and the average expected price of the open market homes in that pipeline is £530K.

As expected, there have been no significant sales launches in the last nine months due to developments that would have launched being sold to institutional build to rent investors. They have residual availability at a number of forward sold schemes, however, and have recently opened furnished show homes at both Bermondsey Works and Manhattan Plaza. This has generated increased interest in both developments and the group continues to make regular sales across a limited unsold portfolio. Despite the subdued market at higher prices, the group has achieved success with its limited number of penthouse apartments, securing the sales off-plan at Stratford Central.

Whilst the build to rent sector is a strategic focus for the group, they will still be developing homes for open market sale and there are two development launches planned for Q1 2018. The second phase of New Garden Quarter in Stratford is expected to be marketed to investors starting in the UK and then internationally where demand remains high. In addition, Bow Garden Square will be marketed from an on-site sales centre predominantly to owner-occupiers. The expected average price at New Garden Quarter is £550K and at Bow Garden Square it is less than £500K.

The group is considering numerous opportunities to add to its development pipeline both for build to rent and open market sales. Since April they have acquired Stone studios in E9 which will deliver 120 new homes and over 50,000 square feet of commercial space, and has been selected as the preferred partner at South Kilburn, a redevelopment in partnership with Brent which will deliver 236 new homes. At South Kilburn they expect to take a full legal interest very soon and work is already underway on the site.

The group’s reported profits in any given period are driven by the number of open market completions and there were far fewer of these in the first half of the year than expected in the second half. This is due to development timings which are all on track and in accordance with the original programmes but do not fall equally across the year.

As a result of the imbalance of completions across the year, pre-tax profits for H1 2018 will be significantly lower than in the second half and also lower than in H1 last year, but entirely in line with expectations. The group is on track to deliver full year pre-tax profit of £40M in accordance with market expectations and the board’s longer term outlook is unchanged.