Games Workshop has now released their final results for the year ended 2017.

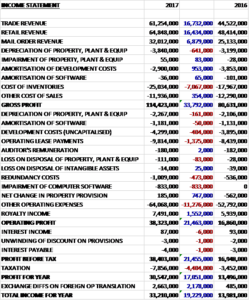

Revenues increased when compared to last year due to a £16.7M growth in trade revenue, a £16.4M increase in retail revenue and a £6.9M growth in mail order revenue. Depreciation was up £641K and cost of inventories increased by £7.1M but amortisation declined by £953K and other cost of sales fell by £354K to give a gross profit £33.8M higher. Operating lease payments grew by £1.4M and there was an £833K impairment of computer software, relating to the replacement of the ERP system, along with an £11.3M increase in other operating expenses but there was a £747K positive shift in property provision changes and royalty income was up £1.6M which meant that the operating profit grew by £21.5M with £7M of that due to favourable forex movements. Finance costs were broadly flat but tax charges grew by £4.4M to give a profit for the year of £30.5M, a growth of £17.1M year on year.

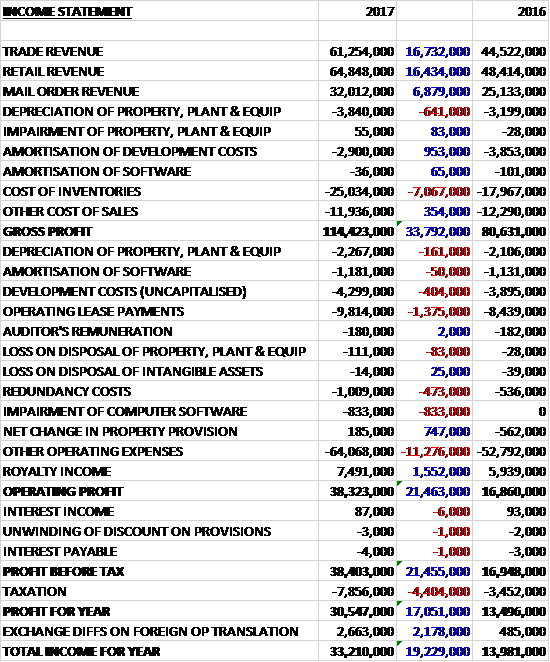

When compared to the end point of last year, total assets increased by £17M driven by a £9.1M growth in cash, a £3.9M increase in inventories, a £2.8M growth in development costs, a £2.2M increase in deferred tax assets and a £1.9M loan to company shareholders. Total liabilities also increased during the period due to a £3.9M growth in current tax liabilities, a £1.2M increase in deferred income a £1.1M growth in trade payables and a £1.1M increase in other payables. The end result was a net tangible asset level of £48.5M, a growth of £7.3M year on year.

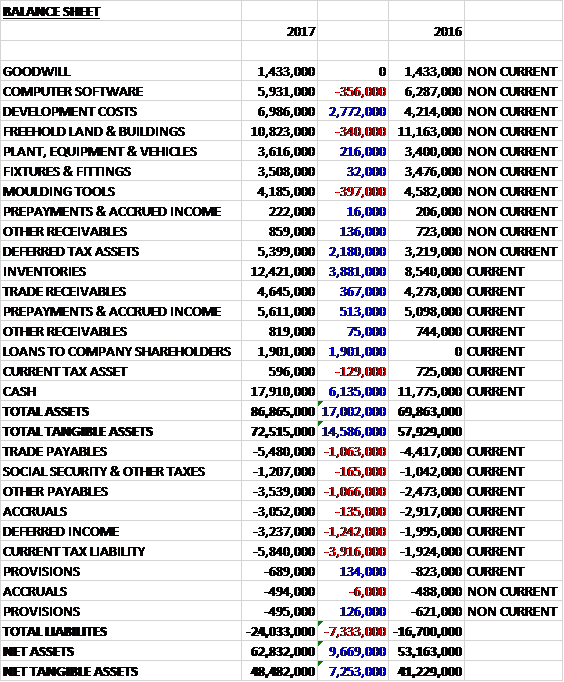

Before movements in working capital, cash profits increased by £21.3M to £49.2M. There was a broadly neutral working capital position compared to an outflow last year buy tax payments increased by £2.9M to give a net cash from operations of £43.9M, a growth of £20M year on year. The group spent £5.4M on tangible assets, £5.7M on development costs and £1.7M on software which meant that the free cash flow was £31.1M. Of this, £25.7M was spent on dividends to leave a cash flow of £5.5M and a cash level of £17.9M at the year-end.

As a business with 75% of sales made overseas, the results have benefited from favourable forex movements. Overall, sales growth in each division at constant currency was around 20%. The step increase in volume across all channels was a significant challenge for the factory and warehousing but have managed with only the necessary increases in resources. They have a flexible structured resource plan to meet any future volu8me changes.

During the year they released over 400 new models across their core systems and added 17 new paint colours to their range. They also launched new editions of their White Dwarf magazine and Blood Bowl game which have both sold well. In March they refocused the Black Library team to ensure they continue to produce bestselling novels and their design to manufacture teams have been working collaboratively on the new edition of Warhammer 40,000: Dark Imperium, released in June.

The operating profit in the Trade division was £18M, a growth of £7.3M year on year. Revenue from the UK and Central Europe increased by £6.5M and revenue from North America grew by £7.7M. All other territories were relatively minor but all saw growth. In addition, the new country managers in China, Singapore, Hong Kong, Japan and Malaysia have all reported double digit growth. The group will continue to invest in Asia with more localised content in the coming year.

The operating profit in the Retail division was £461K, a positive movement of £4.4M when compared to last year. Overall retail sales grew by 21% at constant currency with like for like sales up 16%. Revenues from the UK increased by £3.1M, revenues from the rest of Europe grew by £3.9M, revenues from North America were up £6.2M and revenues from Australia and New Zealand increased by £2.3M. Theo opened a net 11 new stores during the year and the main focus for store openings in the year ahead will be North America and Germany.

The operating profit in the Mail Order division was£18.8M, a growth of £5M when compared to 2016. Sales grew by 27% with sales of Forge World up 23% and the Citadel range up 31%. In the second half of the year they refreshed their home page.

The operating profit in the product and supply division was £16.3M, an increase of £8.3M year on year. They launched a dispenser of eight products called Battle for Vedros in toy shops in North America in June 2016 and a small range called Build and Paint globally in September. Although not delivering huge value to the group, they have proven that they should continue to support a range of products aimed at new customers.

The group received royalty income of £6.9M, an increase of £1.6M when compared to last year. They have had a solid year thanks to the ongoing success of Total War: Warhammer: End Times and Warhammer 40,000: Fireblade. The income is split 80% PC and console, 13% mobile and 7% other.

The replacement of the European ERP system is ongoing. From April 2017, the moved to a more agile methodology for implementing it. The revised plan will ensure they introduce business benefits as they go along rather than just at the end of the project. The estimated cost is now £9M as opposed to £6M. There is also a mail order warehouse system replacement ongoing with an estimated cost of £1.2M that is scheduled to go live in Autumn 2017.

As a result of a procedural oversight, 6p per share of the dividend paid in June is being treated as an unlawful dividend and is shown as a loan to company shareholders on the balance sheet. Although they always had sufficient reserves to pay it, at the time it was made this needed to be demonstrated by reference to interim accounts prior to payments. Those accounts were not filed with Companies House until after the dividend was paid. No fines or other penalties have been incurred but this seems a bit sloppy.

The group announced that Chairman Tom Kirby was retiring after the AGM and will not seek re-election as a non-exec but will become a consultant to the company for a year. Nick Donaldson will become Chairman having been a non-executive director since April 2002. I do hope his pre-able will be as entertaining as Tom’s.

Going forward, following the group’s good performance this year trading has continued strongly into 2018 such that sales and profits to date are well above the same period of the prior year and are likely to be above market expectations. There continues to be some uncertainty for the rest of the year, however.

At the current share price the shares are trading on a PE ratio of 17 which falls to 16.2 on next year’s consensus forecast. After an increase in the total dividend the shares are yielding 4.6%, increasing to 5.6% on next year’s forecast. At the year-end the group had net cash of £17.9M compared to £17.8M at the end of last year.

Overall then this has been a very strong year for the group. Profits are up, net assets increased and the operating cash flow grew with a decent amount of free cash being generated. All divisions saw growth and even the retail business is making a modest profit. It is quite hard to pin down exactly why the company has outperformed.

There is now doubt that forex movements have helped but the underlying performance is still very strong. There have been some refreshes in ranges but it’s hard to see how that has had such in effect. In any case, the shares are no longer the bargain they once were but are not excessively expensive either, with a forward PE of 16.2 and dividend yield of 5.6%. I continue to hold.

On the 5th September the group announced that trading in Q1 has continued strongly. Sales and profits for the year to date are therefore well above the same period last year. Great stuff.

On the 19th October the group released an update where they stated that sales have continued strongly and given the high operational gearing of the business, profits to date continue to be well above the same period last year.