Havelock Europa have now released their final results for the year ended 2016.

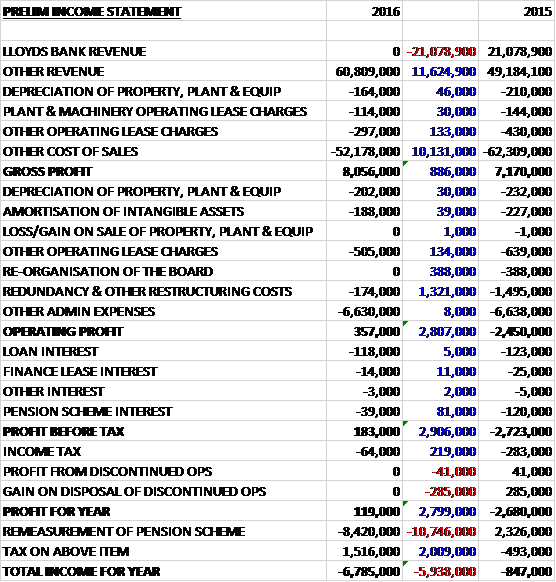

Revenues declined when compared to last year as the loss of the Lloyds Bank revenue, accounting for £21.1M last year, was partially offset by an £11.6M increase in other revenue. Cost of sales declined, however, so the gross profit grew by £8.1M. There was a £134K reduction in operating lease charges, the group didn’t spend £388K on finding a new CEO and restructuring costs reduced by £1.3M which meant that there was a £2.8M positive swing to an operating profit. The pension scheme interest fell by £81K and fax charges were down £219K which gave a continuing profit for the year of £119K, an improvement of £2.4M year on year.

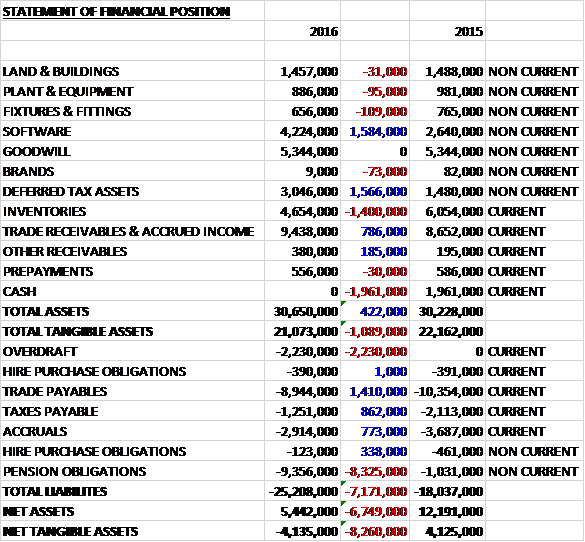

When compared to the end point of last year, total assets increased by £422K to £30.7M, driven by a £1.6M growth in deferred tax assets, a £1.6M increase in software and a £786K growth in trade receivables, partially offset by a £2M decline in cash and a £1.4M fall in inventories. Total liabilities also grew during the year as a £1.4M decline in trade payables, an £862K fall in taxes payable and a £773K decrease in accruals was more than offset by an £8.3M increase in pension obligations and a £2.2M rise in the overdraft. The end result was a net tangible asset level of -£4.1M, a deterioration of £6.7M year on year and a bit of a precarious situation in my view.

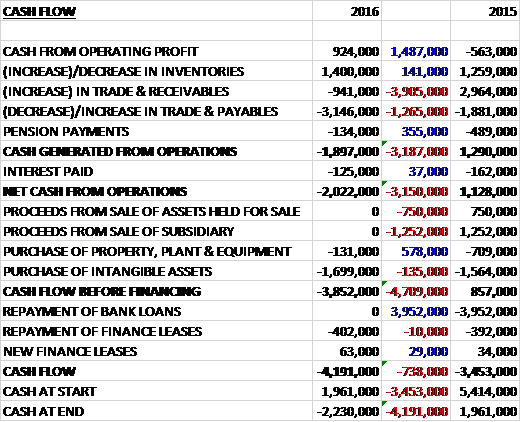

Before movements in working capital, cash profits increased by £1.5M to £924K. There was a cash outflow from working capital, however, with a decrease in payables, so there was a net cash outflow of £2M from operations, a deterioration of £3.2M year on year. The group spent £131K on property, plant and equipment along with £1.7M on intangible assets so there was an outflow of £3.9M before financing. The group also had to repay a net £339K of finance leases which meant that there was a cash outflow of £4.2M for the year and a cash level of £2.2M at the year-end.

There was a major increase in public sector sales in the year, especially in the education sector, but financial sector sales were much lower following the decision by Lloyds Bank to reduce their refurbishment and development spend. Due to the improved margins on major public sector contracts and the impact of operational efficiencies following the restructuring in the prior year, the group did manage to turn a profit, however.

Retail and Lifestyle sales fell slightly in the year. Whilst one of the group’s clothing retail customers continued to open new stores in the UK and Europe, some of their major UK customers reduced their activity. They continue to broaden the customer base in this division and initial orders were received from a health food retailer and an electrical goods retailer during the year.

With the reduced level of business from Lloyds, corporate services had a disappointing year with sales excluding Lloyds broadly flat. They continue to target opportunities for both furniture and fit out contracting in this sector and they have recently secured work from a major new financial services customer.

The group is still somewhat dependent on a small number of large clients. Last year, 30% of revenues came from Lloyds Bank so the dangers of this are clear. This year is somewhat better with the largest customer, Primark, accounting for 14% of revenues.

The group continued to develop their new ERP system and costs in the year totalled £1.7M. A phased implementation of the system started in June 2016 and it became fully operational in February 2017. As well as offering cost and efficiency benefits, it should provide a platform for better implementation of the new operational plan and enable the business to become more agile and responsive.

The group are scraping around to save cash. They have made an agreement with the trustees of the pension fund to defer deficit funding payments of £700K scheduled in 2017 into 2018.

There has been a lot of change in the boardroom over the past year. Hew Balfour, who was CEO between 1989 and 2010 was appointed as a non-executive director in April, replacing Alastair Kerr who resigned. David MacLellan resigned as a non-executive director in January 2017 having been chairman for the last four years. He was replaced by Ian Godden. Finance Director Ciaran Kennedy resigned in April to take up a position at Clancy Docwra and he will be replaced by Donald Borland.

After the period-end, in January the group issued 3,000,000 new shares to the Chairman in consideration for cash. In April 2017 he agreed to provide an unsecured loan of £300k to the group which carries interest of 6%, to be converted into shares in the event of a future placing.

Going forward the first half of the year will be challenging. There is a strong pipeline of opportunities in Retail & Lifestyle and Corporate Services but project delays in the Public Sector will result in the 2017 result being heavily weighed to the second half of the year. The current order book for 2017 delivery of £32M is slightly lower than the £35M last year and a major review of longer term vision, mission and strategy is underway.

At the current share price the shares are trading on a PE ratio of 32.8 which apparently falls to 9.9 on next year’s consensus forecast. At the year-end the group had a net debt position of £2.7M compared to net cash of £1.1M at the end of last year, not helped by the investment in the new ERP system. Obviously no dividend is proposed for the year.

On the 13th June the group released a trading statement at their AGM. They continue to make progress despite operating in a very competitive market. As previously indicated they expect 2017 to be significantly weighed to the second half and for the full year whilst activity in the public sector is expected to be below last year, this will be balanced by a better than expected demand from retail and corporate services clients.

Forecasting for the second half remains difficult but given the current order book of £38M and existing and new framework agreements, the board believes that the performance in the full year will remain in line with their expectations. The recent launch of their new Early Years’ Education and Healthcare furniture ranges have been well received by the market and they are now in the process of updating their secondary school range.

The pipeline in the retail and corporate services sectors is encouraging. They have been appointed exclusively by a major UK Building Society to design and deliver new style furniture for their branch refurbishment programme, have secured new retail customers both in the UK and internationally, and have undertaken their first projects in the car showroom sector.

Overall then this has been another difficult year for the group. They did manage to make a profit but the net tangible asset base is now negative, which is a big warning sign for this type of company scraping around for cash like they are. The operating cash outflow worsened due to working capital movements but there was a modest cash profit made here. The public sector has been good this year and that, combined with earlier cost-cutting was what gave rise to the profit. Unfortunately, public sector is not expected to be as strong this year.

The group seem to be trying to conserve cash and they are in a very precarious position. The fact that they are expecting to be so heavily weighted to the second half of the year is another big concern. The forward PE of 9.9 looks decent at first glance but when the negative tangible asset base is taken into account and the fact that I view the forecasts as a bit weighty, I would not be touching this with a barge pole for now. I do expect them to survive but it will be a bumpy ride. Indeed, I will probably not revisit this share until it sorts it balance sheet out.

On the 29th June the group announced that they were to appoint administrators and the shares have now ceased trading. Can’t say this was unexpected.