Spectris has now released their interim results for the year ending 2017.

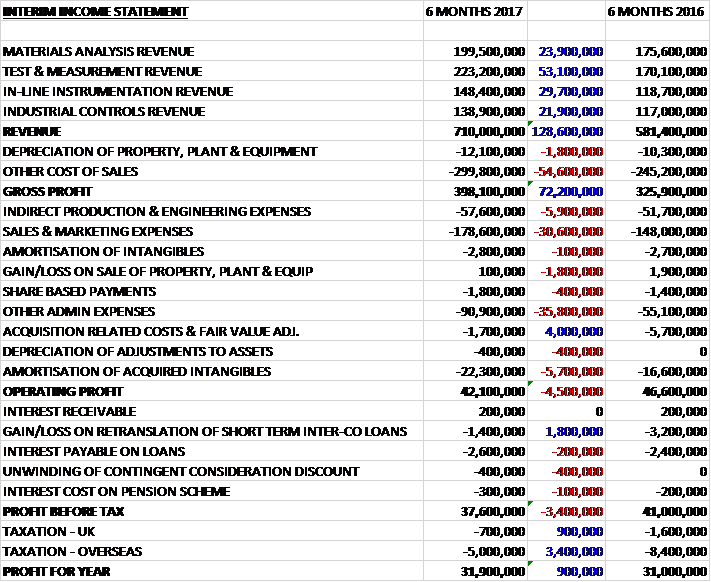

Revenues increased when compared to the first half of last year with a £53.1M growth in test & measurement revenue, a £29.7M increase in in-line instrumentation revenue, a £23.9M growth in materials analysis revenue and a £21.9M increase in industrial controls revenue. Depreciation was up £1.8M and other cost of sales increased by £54.6M to give a gross profit £72.2M higher. Indirect production and engineering expenses grew by £5.9M, sales and marketing expenses increased by £30.6M and other admin expenses rose by £35.8M. Offsetting this, there was a £4M fall in acquisition costs but the amortisation of acquired intangibles increased by £5.7M to give an operating profit down by £4.5M. We then see a £1.8M reduction in the loss on the retranslation of short term inter-company loans and a £4.3M decline in tax charges which meant that the profit for the year came in at £31.9M, a growth of £900K year on year.

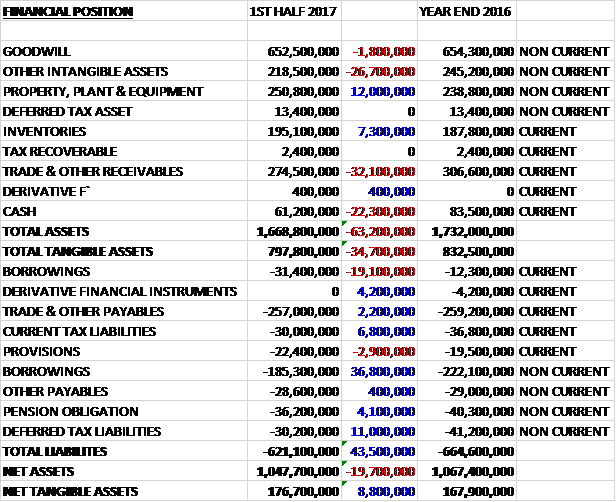

When compared to the end point of last year, total assets declined by £63.2M, driven by a £32.1M fall in receivables, a £22.3M decrease in cash and a £26.7M decline in other intangible assets, partially offset by a £12M growth in property, plant and equipment and a £7.3M increase in inventories. Total liabilities also declined during the period as a £2.9M increase in provisions was more than offset by a £17.7M fall in borrowings, an £11M decrease in deferred tax liabilities, a £6.8M reduction in current tax liabilities, a £4.2M fall in derivative financial liabilities and a £4.1M decrease in the pension deficit. The end result was a net tangible asset level of £176.7M, a growth of £8.8M over the past six months.

Before movements in working capital, cash profits increased by £8.3M to £82.7M. There was a cash inflow from working capital, but this was slightly lower than last year and after tax payments increased by £7.3M the net cash from operations was £79M, a decline of £1.1M year on year. The group spent £24.4M on capex and £12.6M on acquisitions to give a free cash flow of £42.4M. They spent £2.2M on interest payments (this should be included in operational cash flow in my opinion) and £40.5M on dividends. They also repaid £41M of borrowings to give a cash outflow of £41.2M and a cash level of £29.8M at the period-end.

On a like for like basis, excluding project Uplift costs, adjusted operating profit decreased by 3%. This reflected the impact of the higher sales volumes, offset by overhead cost increases and the performance of in-line instrumentation which posted a decline in profits.

The like for like adjusted operating profit in the Materials Analysis business was £21.4M, a growth of £1.3M year on year. LFL sales were up 3% and LFL sales to the pharmaceutical sector grew strongly in the period with a particularly good performance in Asia. This has been driven by higher investment within the generics sector and the current regulatory focus on data integrity is leading to new equipment purchases as manufacturers upgrade their capabilities.

Since the start of the year the merger of Malvern Instruments and PANalytical has been in effect and work is underway to cross train and merge the sales and marketing teams. The initial focus has been on cross-selling opportunities and a number of these have already been realised with new sales of both products into existing counterpart company customers. During the period the combined business launched two new products: one aimed at helping customers meet regulations in the biopharmaceutical industry and the other for the analysis of the elemental composition of liquids.

At PMS the acquisition of CAS Clean Air Service has allowed the business to be able to offer its Good Manufacturing Practice service knowledge and expertise for regulatory compliance in the pharmaceutical industry. During the period this has now been extended into other markets in Europe and the US. Demand for consulting services in areas such as sterility assurance continues to be robust and the business has been able to provide this additional service to existing customers.

In the metals, minerals and mining sectors, LFL sales returned to growth following the sizeable declines in 2016. Europe delivered a strong performance, although North America continued to see a decline. Commodity prices for base metals have shown a slow recovery. Investments in new production and analytical capabilities are still at a low level, however, but the number of opportunities has started to increase. Sentiment in the mining sector has been improving and the group has seen an uptick in Australia in particular. Aftermarket sales remained robust as customers continued to repair and support their existing equipment.

LFL sales to academic research institutes were down in the period with all regions showing a decline, although there was good growth in orders. In North America, the government has been operating under a continuing resolution that froze 2017 spending at most agencies and generally prevented them from starting new programmes. Similarly political uncertainty in parts of Europe has meant that academic research expenditure has remained subdued in this region. In Asia the key positive market was Japan which did see sales growth.

In the electronics, semiconductor and telecoms sector, LFL sales rose year on year with the main demand centre of Asia showing strong growth. Europe also saw LFL sales increase while LFL sales in North America were lower. There has been strong growth in semiconductor demand, particularly in China and South Korea with a continuation of the favourable market conditions seen in the second half of last year. Electronics sales in the period have been lower, but the order growth was up year on year.

Going forward the board expect sales growth to continue in the second half in the pharmaceuticals sector, given the order growth seen to date and the expansion of the advisory service into new markets such as China. Given the improving backdrop in the metals, minerals and mining sectors, they are encouraged that the increased market activity will start to feed through to a sustained improvement in sales for Malvern and aftermarket sales are expected to remain robust. Sales to the academic research sector remain unpredictable as public sector budgets are likely to remain under pressure in many countries. In the electronics sectors, they expect to see continued strong growth in Asian markets.

The like for like adjusted operating profit in the Test and Measurement business was £19.2M, a growth of £2.1M when compared to the first half of last year. Like for like sales grew by 5%. Sales to automotive customers grew strongly with all key regions delivering growth. At Millbrook the group have been expanding the capacity of their automotive testing services. In May a new large climatic chamber was opened to be used for conducting environmental tests on vehicles. In July they added further capacity as well as complementary customers and services with the acquisition of a commercial vehicle test facility in the UK. The CSA Leyland Technical Centre provides test services to the commercial vehicle, automotive and off-highway sectors and expands Millbrook’s capacity in powertrain, safety and vehicle testing.

There was good LFL sales growth to machine manufacturers in the period. Although the growth in sales in this sector was primarily driven by non-automotive related demand, a significant proportion represents sales into the automotive supply chain. Machine manufacturing sales were strong in Asia, particularly China and in Europe Germany saw good growth with an increase in German exports and an increasing desire for automation and robotics products driving demand for industrial measurement solutions.

In aerospace and defence, LFL sales were flat overall with North America and Europe seeing sales increases, offset by a reduction in Asia. Sales to electronics and telecoms customers were down slightly. Sales to telecoms customers were down as sales to this sector are lumpy, reflecting the scheduling of projects by customers. They have continued to see good traction with Chinese mobile phone operators and have been working closely with Huawei. Sales to electronics customers increased in both Asia and Europe, driven by trends in consumer demand for devices such as audio and communication systems with improved sound quality. They are also seeing continued growth in the supply of high quality components for acoustic testing of smartphones.

In the unconventional oil and mining markets, commodity prices have settled and there has been an increase in US production. As a result the group’s fracking monitoring business has been more buoyant and sales in North America have increases markedly on last year. Mining activity has been more subdued, however, and has been impacted in Asia by the Indonesian government’s restrictions in exports.

Going forward, the board expect the automotive sector to remain robust though the remainder of the year with automotive customers expanding their development programmes and the group’s capex programme coming through to generate revenue. In the aerospace and defence sector, they expect to see a similar trend to the first half, although the pipeline of opportunities has improved in recent months. The consumer electronics market is expected to remain attractive. If commodity prices remain settled, they expect the improvement of their microseismic monitoring to be sustained through the remainder of the year.

The like for like adjusted operating profit in the In-line Instrumentation business was £8.7M, a decline of £1.5M when compared to the first half of 2016 due to adverse mix, restructuring and additional costs following the closure of a business centre in Europe. LFL sales were actually very strong, increasing by 11% year on year. Restructuring activities continued, in particular at NDC Technologies which is consolidating its California production and admin functions into its Ohio facility with the California facility becoming the new Web Process Solutions Technical Centre of Excellence.

Sales to the pulp, paper and tissue markets grew in the first half with all regions in positive territory. Pulp and paper sales were up slightly whilst the tissue business had a good start to the year with particularly strong growth in Asia where they have secured new business with producers of premium grade tissue products. They have also continued to expand their offering by providing solutions for process control and optimisation, particularly in the chemical pulp segment, with the capstone Software tools.

They received new orders for their dataPARC analytics in the pulp and paper, chemicals and other industries. In June they delivered their first digital solution for tissue production management with a vibration monitoring systems installed at a Spanish paper and tissue company, whereby vibration data is captured and displayed using their new analytics software, allowing monitoring of the machine’s Yankee dryer performance.

LFL sales to the energy and utilities sector increased. The backdrop for refinery markets has improved compared to last year as energy prices have stabilised and the group have seen a more solid performance in the hydrocarbon processing sector in the US with activity in Asia also picking up. The wind power business delivered a strong growth in sales from both the turbine OEM companies and their targeted approach to wind farm owners and operators. Bruel & Kjaer Vibro was selected by EDP Renewables to supply and retrofit the installation of condition monitoring systems for more than 15,000 wind turbines globally.

At Servomex, their customer offering has been broadened by the launch of the Laser 3 analyser for combustion applications. This compact product measures ammonia, oxygen and carbon monoxide from combustion processes. They are also aiming to streamline their industrial gases customer offering to a single platform with two variants, a simplified user interface and digital communications which can be more easily deployed by customers according to their needs. This platform will have the ability to integrate their new AquaExact Moisture Sensor which measures moisture in a range of process applications such as air separation, natural gas processing and transportation.

After a surge in growth last year, sales to the web and converting industries increased only slightly this time. Growth in sales in Europe and Asia was offset by an overall decline in North America. The performance in packaging and the cable and tube business has been robust as a result of improving market conditions. During the period NDC Technologies entered into a cooperation with RAM, a web inspection company in similar industries, to sell their web inspection systems in territories RAM don’t cover with a reciprocal arrangement whereby RAM will sell NDC’s gauging systems to their customers.

Going forward, in the pulp, paper and tissue market, the board expect to continue to see good demand in tissue and packaging, particularly in Asia. Sales of Capstone software are also expected to drive growth in both this sector and in other process industries. In energy and utilities, the current environment is encouraging with a more stable oil price underpinning cautious investment in areas such as hydrocarbon processing. Demand from the wind energy sector is expected to remain healthy as they continue to focus on wind farm operators and owners.

The North American market has shown signs of improvement in the first half of 2017, as they see a freeing up of capex and industrial spend in the process industries they serve. They would expect to see the segment’s overall growth in LFL sales to moderate as they go through the second half of the year, however. Based on the current order book and the non-recurrence of adverse costs seen in the first half, they expect to see a strong recovery in margins though.

The like for like adjusted operating profit in the Industrial Controls business was £17.8M, an increase of £1.9M year on year. There was a 5% increase in LFL sales, including in N. America for the first time since 2014.

At Omega, the restructuring continues. Electronics manufacturing, currently performed in California, is to be outsourced and distribution operations for certain markets will be consolidated. The business has developed a number of products to capture the opportunity presented by the increasing “Internet of Things”. Their long range wireless monitoring systems provide web-based monitoring of temperature, humidity and barometric temperature. This system can provide data assurance and security, and they have worked with a major satellite company to provide such a solution.

The industrial networking business also saw a return to sales growth in the core North American market, particularly with the Ethernet and Interface product families. During the period they had notable sales at two major automotive manufacturers, delivering networking solutions for their robotics OEMs and own manufacturing lines. In May Red Lion announced an enhancement to its products which enables more secure communications to cloud platforms and remote access applications. This enhancement utilises Distrix Networks’ software defined networking technology with Red Lion’s RAM range of industrial remote terminal units.

At the automatic ID and machine visions solutions business, sales of their Micro Hawk products have continued to grow rapidly and during the period a new high density version was launched that can read very small barcodes, for example on a silicon chip.

Going forward, progress for this segment in the second half will be largely determined by the industrial demand environment in the US which has experienced an improving backdrop during the first half. They expect to see continued good growth in Asia. As they see customers continue to focus on increasing productivity and efficiency, they expect to see continued growth in demand for their solutions for factory automation and industrial networking, sensing and controls. At Omega, they continue to expect the organisational changes and restructuring measures to deliver an improvement in performance and to exit the year with margins at historic levels.

Project Uplift is well underway with initiatives progressing as planned. The net spend of £8.8M includes Phase 1 activities for IT, procurement and footprint. They have also completed a shared feasibility study and are moving into the detailed design and implementation planning phase.

In February the group acquired Pixirad Imaging Counters, a supplier based in Italy, for a total consideration of £2.8M. The business develops and distributes x-ray detectors and the acquisition generated goodwill of £1.7M. In May they acquired Setpoint, a US business, for a total consideration of £8M. This extends their capabilities in the condition monitoring market and generated goodwill of £4.6M. These acquisitions contributed £1.6M to group operating profit during the period. After the period-end the group acquired CSA Leyland Technical Centre, a company based in the UK, which extends the group’s automotive testing facilities.

Going forward, overall the board expectations for the full year remain unchanged.

At the current share price the shares are trading on a PE ratio of 24.5 which falls to 18.3 on the full year consensus forecast. At the period-end the group had a net debt position of £155.5M compared to £150.9M at the end of last year. After a 6% increase in the interim dividend the shares are yielding 2.1% which increases to 2.4% on the full year forecast.

Overall then this has been a bit of a mixed period for the group. Profits increased but this was due to lower tax charges and pre-tax profits declined. Net tangible assets grew but the operating cash flow declined but interestingly this was due to higher tax payments, in contrast to the profit figures, and cash profits increased with a decent amount of free cash being generated. The overall decline in profit has been due to increased overheads and higher costs in the in-line instrumentation division. The performance in the other division seems pretty good with LFL sales increases across the board.

A lot of the group’s markets do seem to be picking up a bit and I am more positive here than I have been for some time. The shares remain expensive in my view, however, with a forward PE of 18.3 and yield of 2.4%. I therefore find it hard to justify a purchase at the moment.

On the 30th August the group announced that it had signed an agreement to sell Microscan Systems to Omron Corp for a total cash consideration of £123M. The net proceeds from the sale will be used to reduce net debt. The sale will generate a profit of £101M and the business made a profit of £7M last year which means it is expected to have an impact of 2p on EPS in 2017.

Microscan is a provider of machine vision technology and solutions for critical identification, inspection and verification applications. The group’s strategy is transitioning to provide customer solutions incorporating hardware, software and services in selected markets so they believe the business is better off elsewhere. This seems to be a bit of a backwards step as the business is a profitable one, but on the other hand it is being sold for way over the net asset value and it will help to reduce debt so in two minds over this.

On the 21st November the group released a trading update for the first four months of H2. Reported sales increased by 9% and group like for like sales were up 7% with like for like sale in the first ten months of the year increasing by 6%.

Like for like sales grew in all key regions with particularly good growth in Asia, led by strong demand from China. The performance in North America improved markedly since the first half of the year while Europe continued to perform in line with the first half. Like for like sales declined marginally in the rest of the world.

LFL sales increased across all four business segments. There was a notable sales growth in automotive, electronics, semiconductors and telecoms and metals, minerals and mining while academic research continued to see a sales decline in the period.

During the period the group completed the acquisition of Omicon for an initial consideration of $29M plus a deferred consideration of up to $7M. The business provides a range of services to help its customers analyse and improve product reliability and safety and is being integrated alongside the Prenscia Software business within Test and Measurement.

In October the divestment of Microscan was completed with net cash proceeds received of £93M. The disposal will lower adjusted EPS by around 2p. Following the sale, net debt was £26.6M before the outflow of the dividend payment of £23M in November.

Project Uplift initiatives continued and the group still expects a net cost of £14m in 2017 for Phase 1 but both gross benefits and costs will be lower than previously expected. Overall though, the outlook for the full year remains unchanged.

On the 14th December the group announced that they had reached an agreement with Macquarie Capital for them to acquire 50% of the group’s environmental monitoring business EMS Bruel & Kjaer for a cash consideration of £43.4M. The net proceeds will be used to reduce net debt. The business is a provider of environmental monitoring services to airports, cities, mines and construction companies. It will now benefit from accelerated investment which will help create additional services that enable asset owners to monitor and manage their resources more effectively.

On the 26th January the group announced the acquisition of Concept Life Sciences from Equistone Partners. The purchase consideration of £163M will be met from existing cash and bank facilities. The business is a UK-based group providing integrated drug discovery, development, analytical testing and environmental consultancy services to an international customer base, mainly in the pharmaceutical, biotechnology, agrochemical and environmental sectors. Additionally it carries out development and analytical services for the food, consumer and environmental industries.

The gross assets of the business are £73.4M and last year EBITDA was £9.3M and it has a history of double digit growth which is expected to continue. The acquisition adds test service capabilities to the Materials Analysis segment, where it has strong synergies with Malvern Panalytical. This actually looks like a nice acquisition at a decent price to me.