Finsbury Food has now released their final results for the year ended 2017.

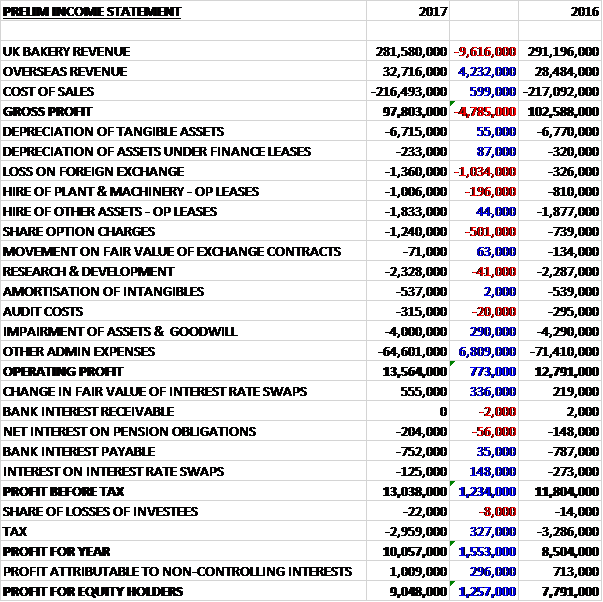

Revenues declined when compared to last year as a £4.2M growth in overseas revenue was more than offset by a £9.6M decrease in UK revenue. Cost of sales reduced marginally to give a gross profit £4.8M lower. There was a £1M increase in the loss on forex movements and share option charges grew by £501K but this was offset by a £6.8M fall in other admin expenses and the operating profit grew by £773K. There was a £336K positive movement in the hedging instruments and a modest reduction in interest with a £327K decline in tax charges, all of which meant that the profit for the year was £9M, a growth of £1.3M year on year.

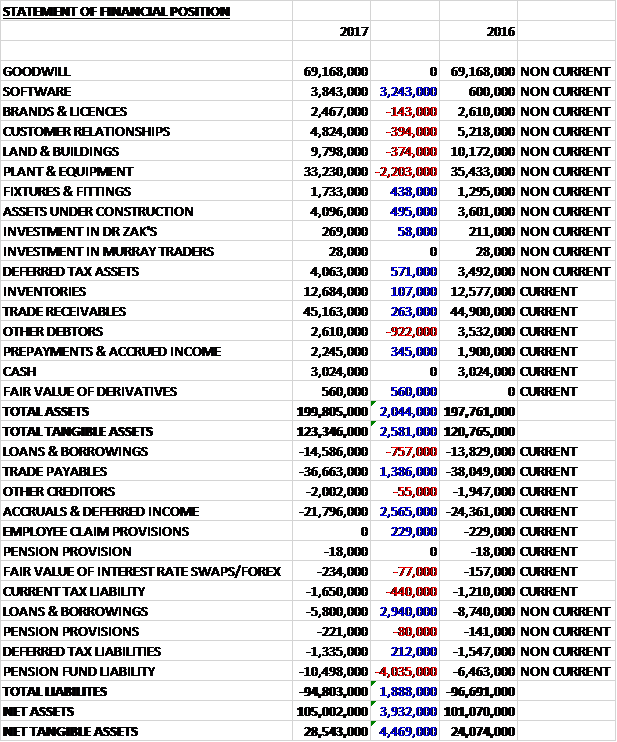

When compared to the end point of last year, total assets increased by £2M, driven by a £3.2M growth in the value of software, a £571K increase in deferred tax assets and a £560K increase in the fair value of derivatives, partially offset by a £2.2M decline in plant and equipment and a £922K decrease in other debtors. Total liabilities declined during the year as a £4M growth in the pension liability was more than offset by a £2.2M decrease in borrowings, a £2.6M fall in accruals and deferred income, and a £1.4M decline in trade payables. The end result was a net tangible asset level of £28.5M, a growth of £4.5M year on year.

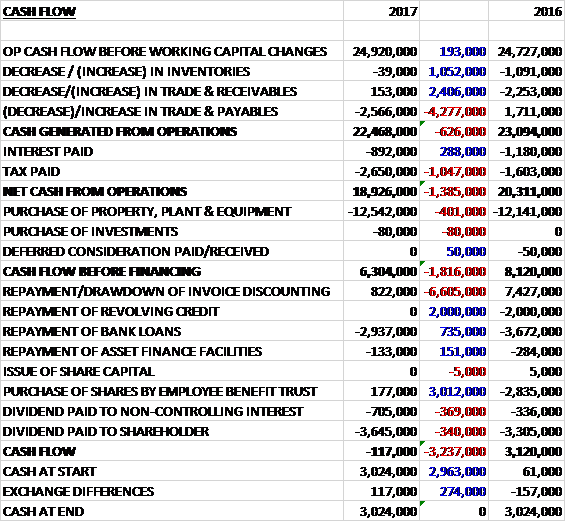

Before movements in working capital, cash profits increased by £193K to £24.9M. There was a cash outflow from working capital due to a fall in payables and after tax payments grew by £1M the net cash from operations was £18.9M, a decline of £1.4M year on year. The group spent £12.5M on capex to give a free cash flow of £6.3M. Of this, a net £2.1M was used to pay back loans and £4.4M went on dividends to give a cash out flow of £117K. Interestingly this is the exactly same amount as the benefit from forex movements so the group ended the year with the same amount of cash as it started it – £3M.

The Grain D’Or business has been historically loss making and despite the implementation of a range of initiatives to improve the business including cost control and new working practices, the site remained loss making. The group now proposes to close the site and a decision has been made to impair the assets by £4M. The business has lost two large contracts since the year-end which has affected its financial performance further. It is believed that the exceptional cash costs associated with the closure could reach up to £10M, spread over seven years, but more likely to be in the region of £6M.

The operating profit at the UK business was £15.4M, a decline of £518K year on year, not helped by reduced promotional spend which was enacted to preserve margins. In Foodservice, the year was one of consolidation with revenues marginally ahead of the prior year. New business was secured on the new cake ranges with the two major UK Foodservice wholesalers, as well as major cafes and pub groups. Kara Brioche buns continue to grow in line with demand, traditional doughnuts continued their renaissance and artisan bread products continued to grow in both sales and outlet penetration. There was strong growth in the top four customers, somewhat offset by reduced trading in export markets, particularly France, and in some smaller customer business closures.

The group has recently completed the renewal of its long standing partnership with Thorntons which will see the group continue to produce and market cakes. They have also announced the launch of a new Mary Berry range in Spring which extends to loaf, sharing and celebration cakes. Successful character licenses in the year have included Batman vs Superman, Minions, Star Wars and Emoji along with Me to You, Peppa Pig and Paw Patrol.

The operating profit at the Overseas business was £2.2M, a growth of £708K when compared to last year, benefiting from improved celebration cake and free from product ranges along with favourable forex movements.

This has not been an easy market. There has been a deflationary UK retail food market which has led to an upswing in discounter’s market share but this has changed in the second half of the year. There have also been some specific cost issued that relate to the current weakness of Sterling and increased costs of the national living wage. These trends looks set to continue for some time with high profile butter price hikes, driven by increased demand and a supply shortfall. These have been somewhat overcome through efficiency gains and price hikes.

During the year the group made capital investments of £12.5M. A new cake line is coming on stream in Cardiff, being commissioned for full production in 2018 and a new artisan bread bakery has been opened in Salisbury. There is a new IT system being rolled out which will give a common platform for the whole business. Going forward, they plan to invest in new plant and equipment to further improve efficiency, product quality and their capability in sustainable and environmentally responsible manufacturing.

At the current share price the underlying PE ratio is 11.4 which falls to 10.8 on next year’s consensus forecast. At the year-end the group had a net debt position of £17.4M compared to £19.7M at the end of last year. After a 7% increase in the total dividend, the shares are yielding 2.8% which increases to 3.1% on next year’s forecast.

Overall then this has been a bit of a mixed year for the group. Profits rose due to a reduction in admin expenses, net assets increased and although the operating cash flow declined, this was due to working capital movements and higher tax payments with the cash profits showing a modest increase. The group still made a decent amount of free cash. The UK business is struggling due to a sluggish market, the living wage increases and raw material price rises. The overseas business is growing, however, no doubt aided by the weak pound.

Going forward, the PE of 10.8 and yield of 3.1% is not too bad but much rests on the raw material issues given the slow growth in the market.

On the 22nd November the group released a trading update covering the first four months of the year which was in line with expectations. Total group sales grew by 4% reflecting the newly inflationary environment. The UK bakery division’s sales increased by 5% while the overseas division declined by 3.8%.

On the 18th January the group released a trading update for the first half of the year where they stated that they had performed in line with management expectations. Total group sales were £157.8M, representing a 0.7% increase. Sales for the continuing business (excluding Grain D’Or) grew by 2.5% to £144.8M with the UK bakery division growing by 3.2% and the overseas division declining by 2.1%. The board believe that its activities during the period position the group well for a solid performance for the rest of the year.

On the 1st March the group announced the purchase of the freehold property at its Lightbody factory in Hamilton which has been occupied by the group for fifteen years. The total purchase price is expected to be £2.6M and financed from existing resources. This is a good development in my view.