Central Asia Metals have now released their interim results for the year ending 2017.

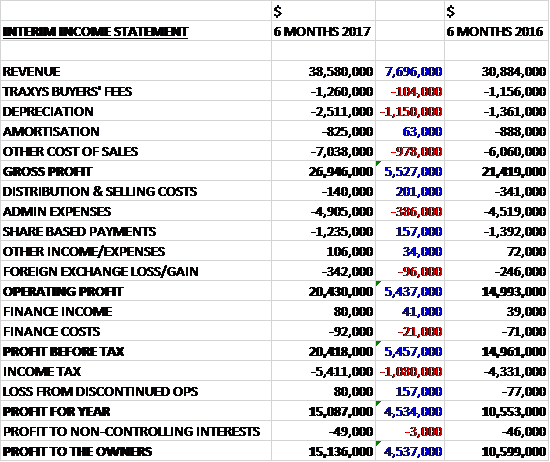

Revenues increased by $7.7M when compared to the first half of last year. Depreciation was up $1.2M and other cost of sales increased by $978K to give a gross profit $5.5M higher. Distribution and selling costs fell by $201K but admin expenses increased by $386K, Share based payments fell by $157K but forex losses increased by $96K to give an operating profit $5.4M higher. Finance costs were broadly similar but tax charges grew by $1.1M which meant that the profit for the period was $15.1M, a growth of $4.5M year on year.

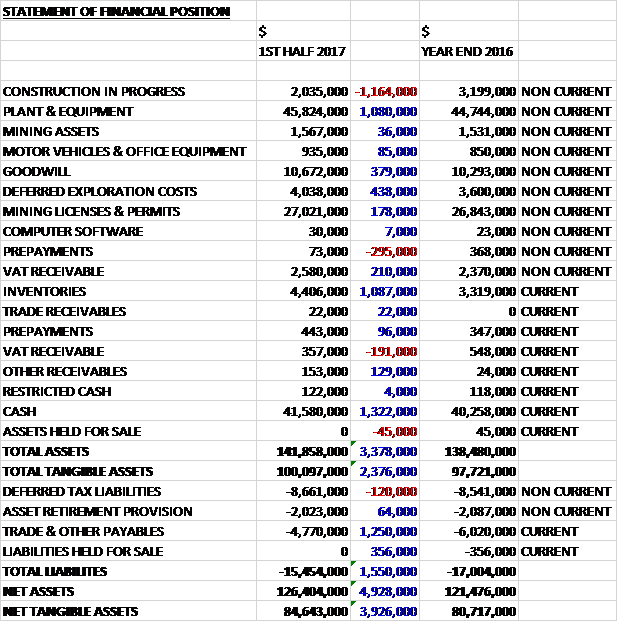

When compared to the end point of last year, total assets increased by $3.4M driven by a $1.3M growth in cash, a $1.1M increase in plant and equipment and a $1.1M growth in inventories, partially offset by a $1.2M fall in the value of construction in progress. Total liabilities declined during the period, mainly due to a $1.3M decrease in payables. The end result was a net tangible asset level of $84.6M, a growth of $3.9M over the past six months.

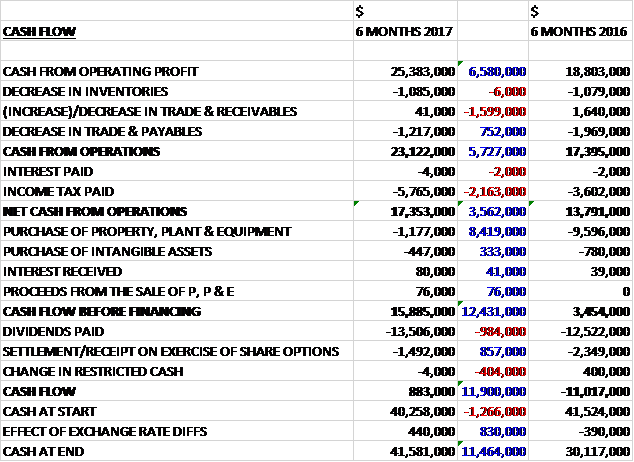

Before movements in working capital, cash profits increased by $6.6M to $25.4M. There was a modest cash outflow from working capital but the tax payments increased by $2.2M to give a net cash from operations of $17.4M, a growth of $3.6M year on year. The group spent $1.2M on property, plant and equipment along with $447K on intangible assets, relating to Copper Bay expenditure, and the free cash flow was $15.9M. Of this, $13.5M went on dividends and $1.5M on share options to give a cash flow of 883K for the half year and a cash level of $41.6M at the period-end.

During the period, the group produced 7,027 tonnes of copper, an increase of 2% and they are on course to achieve the 2017 guidance of 13,000 to 14,000 tonnes.. They sold 6,870 tonnes, which represents an increase of 8%. The average copper price achieved was $5,659 per tonne compared to $4,903 in the first half of last year and was the driver of the improved performance.

Kounrad’s cash cost of production was 45c per pound, compared to 40c per pound in the first half of last year. Production from the Western Dumps started in April and this resulted in slightly higher electricity consumption and additional labour costs to manage the operations. Over the coming years, the proportion of copper produced from the Eastern Dumps will fall as production from the Western Dumps gradually increases. This will result in slightly higher electricity consumption and additional labour to manage the Western Dumps operations. The group’s fully inclusive unit cost was $1.08 per pound, up from 97c per pound. The increase is due to the increased cash cost, higher depreciation and larger MET obligations.

The Kazakh Tenge, which weakened in August 2015, has remained broadly stable since, and there has been little in-country inflation which has meant that the group’s profitability has increased considerably given the increase in the copper price. As of the period-end, there is estimated to be a further 19,500 tonnes of copper to be recovered from the Eastern Dumps during the next three years. The new sprinkling irrigation system, which has been designed to enable the group to recover copper resources from within the slope areas of the dumps became operational in July.

Q2 was an important period of transition as Kounrad began irrigating the Western Dumps. By the end of the quarter, around 1,300 tonnes of copper had been recovered from this material. This leaching process has been in line with expectations and test work, and in June, copper production from the Western Dumps represented around 40% of total metal recovered.

After completing the stage 2 expansion at Kounrad, there are no additional major capex programmes at the mine, with only annual sustaining capex of around $2M expected going forward.

During the winter period, the Shuak exploration team undertook studies reviewing all historic data and they have now started field based work. A drilling programme of approximately 4,700 metres has recently started together with an initial 7,000m CHT drilling campaign and in total, 22,000 metres of drilling are planned for 2017 at a cost of $1.8M. The group remains focused on the near surface copper oxide resource potential of the license area and believes that in the future it could be possible to develop another SX-EW style of processing operation, similar to that at Kounrad. In addition, they also intend to explore the primary copper porphyry target at depth.

During the period the group undertook some additional engineering studies at Copper Bay with the intention of improving the economics of the project. While some capex savings were identified and there is the potential to optimise the project further in the future, the board decided that these findings were not sufficiently material to warrant developing Copper Bay in the near term. In August the board made the decision to sell the project with a sales process due to start in Q4.

After the period-end, in August, the group became the registered owner of the Shauk sub soil user contract. In the same month, given that they do not intend to develop the Copper Bay project in current market conditions, the board made the decision to dispose of their holding in the business and will start the sales process in Q4.

At the current share price the shares are trading on a PE ratio of 14.1 which falls to 11.2 on the full year consensus forecast. After an increase in the interim dividend the shares are yielding 6.4% which falls to 4.8% on the full year consensus forecast. At the period-end the group had a net cash position of $41.7M compared to $40.4M at the year-end.

On the 22nd September the group announced that it had acquired Lynx Resources, the owner of the SASA Zinc-lead mine in Macedonia for $402.5M. The mine has a reserve base supporting production until at least 2032. Last year it produced 783,000 tonnes of ore which generated 22,515 tonnes of zinc in concentrate and 28,955 tonnes of lead in concentrate and in the first six months of the year it achieved an EBITDA margin of 61%. The transaction is expected to be both earnings and cash flow per share accretive in the first full year.

The total consideration of $402.5M is being funded with $120M of debt funding with Traxys at 4.75%+LIBOR with a roll-over of $67M of existing Lynx debt; $153.5M in CAML shares via an accelerate book build; $50M in CAML shares to Orion via an equity subscription; and $12M of deferred consideration.

As can be seen above, the group is looking to raise $153.3M through a placing with both existing investors and new institutional investors. At the same time, non-executive director Kenges Rakishev intends to sell around 10.6M shares, which represents 9.5% of the company’s existing share capital Following the sale he is still expected to hold approximately 10.6M shares in the company.

On the 3rd October the group released a Q3 operations update. Copper production in the quarter was 3,842 tonnes compared to 4,102 tonnes in Q3 last year. Copper cathode sales were 3,795 tonnes compared to 4,291 tonnes last time but they are still on course to achieve the upper end of production guidance of between 13,000 tonnes and 14,000 tonnes. During the quarter, 2,179 tonnes of copper has been recovered from the Western Dumps.

The group are nearing the completion of their 2017 Shauk drilling programme. The CHT drilling programme has finished with 17,500 metres having been drilled and the 5,200 metre diamond drilling programme is 90% complete.

Overall then this has been a strong period for the group with profits up, net assets increasing and the operating cash flow growing with plenty of free cash being generated. Production was broadly flat but the growth in profits has been due to the increase in the copper price. Costs did not grow anywhere near as much as the sales price but it should be noted that now the Western Dumps are being utilised, costs will be slightly higher going forward.

Obviously this is overshadowed by the acquisition of the SASA Zinc mine. The rationale seems sound, particularly in order to diversify away from Kazakhstan. The mine did not come cheap, however, and with quite a bit of debt to pay off, this is not without its risks. Overall though with a forward PE of 11.2 and yield of 4.8% I am happy to continue holding.

On the 15th January the group released an update covering Q4 and the year as a whole. At Kounrad, Q4 copper production of 3,234 tonnes brings the total output for 2017 to 14,103 tonnes and Q4 copper cathode sales of 3,516 tonnes brings the annual total to 14.181 tonnes.

The group assumed economic ownership if Sasa at the start of October. In 2017, mined and processed ore was 792,068 tonnes and 793,332 tonnes respectively and the average head grades were 3.18% zinc and 3.98% lead. The mine typically received from smelters around 85% of the value of its zinc in concentrate and around 95% of the value of its lead in concentrate. Accordingly, 2017 payable production of zinc was 18,091 tonnes and lead was 28,387 tonnes.

During the year Sasa sold 375,544 ounces of silver. Due to an existing streaming agreement with Osisko Gold Royalties, the group will receive a base of $5 per ounce for its silver production for the life of the mine. 2017 payable silver sales since the start of November was 67,485 ounces. In Q2 the Sasa team started construction of a tailings storage facility with completion expected in the second half of 2018.

The Shuak exploration programme was completed in October. 75% of diamond drilling lab results have been returned with some CHT samples still to be processed. New areas of oxide mineralisation have been identified at the Kyzyl-Sor prospect and diamond drilling also returned encouraging intercepts of copper sulphide mineralisation at the Mogol V and Mongol I-II prospects with gold and molybdenum also identified in some cases.

While the preliminary work is encouraging, the team will undertake additional drilling and exploration in order to better understand likely continuity or resource potential of the license. Much of the winter period has been spent compiling assay data and designing the 2018 exploration programme which is expected to start in June. A key area of focus will be delineating the extent of the oxide mineralisation identified at Kyzyl-Sor.

Going forward the group targets 2018 Kounrad copper production of between 13,000 and 14,000 tonnes of cathode, slightly less than this year, with around 65% expected to be leached from the Western Dumps. At Sasa, they expect underground ore production of between 780,000 and 800,000 tonnes. This should result in zinc production of between 21,000 and 23,000 tonnes and lead production of between 28,000 and 30,000 tonnes.

On the 9th February the group announced that non-executive director Kenges Rakishev sold his entire holding of 10,605,876 shares at a value of £29.2M. This is not ideal.