Origin Enterprises has now released their final results for the year ended 2017.

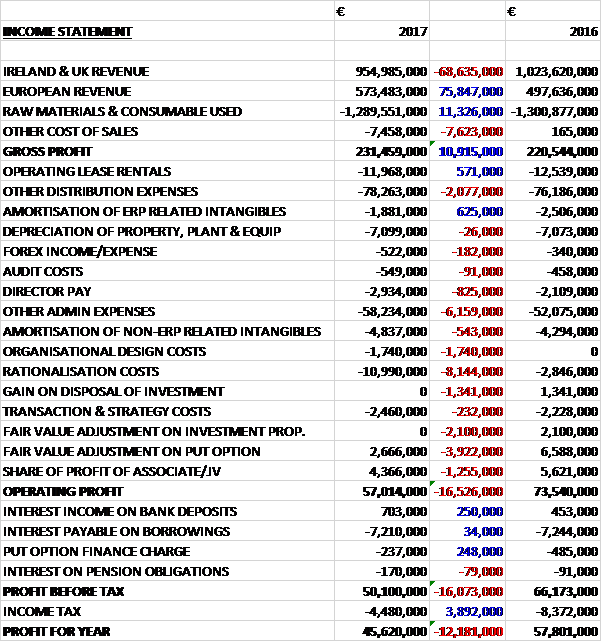

Revenues increased when compared to last year as a €68.6M decline in UK and Irish revenue was more than offset by a €75.8M growth in European revenue. Raw material costs declined by €11.3M but other cost of sales increased by €7.6M to give a gross profit €10.9M higher. Distribution expenses increased by €1.5M, director pay was up €825K and other admin expenses grew by €6.2M. We also see rationalisation costs up €8.1M, organisational design costs of €1.7M, no gain on investment disposals, which was €1.4M last year, a detrimental movement of €6M on fair value adjustments and a €1.3M reduction in the share of profit from associates, all of which meant that the operating profit decreased by €16.5M. The group did make a small improvement in finance costs/income and tax charges fell by €3.9M, however, to give a profit for the year of €45.6M, a decline of €12.2M year on year.

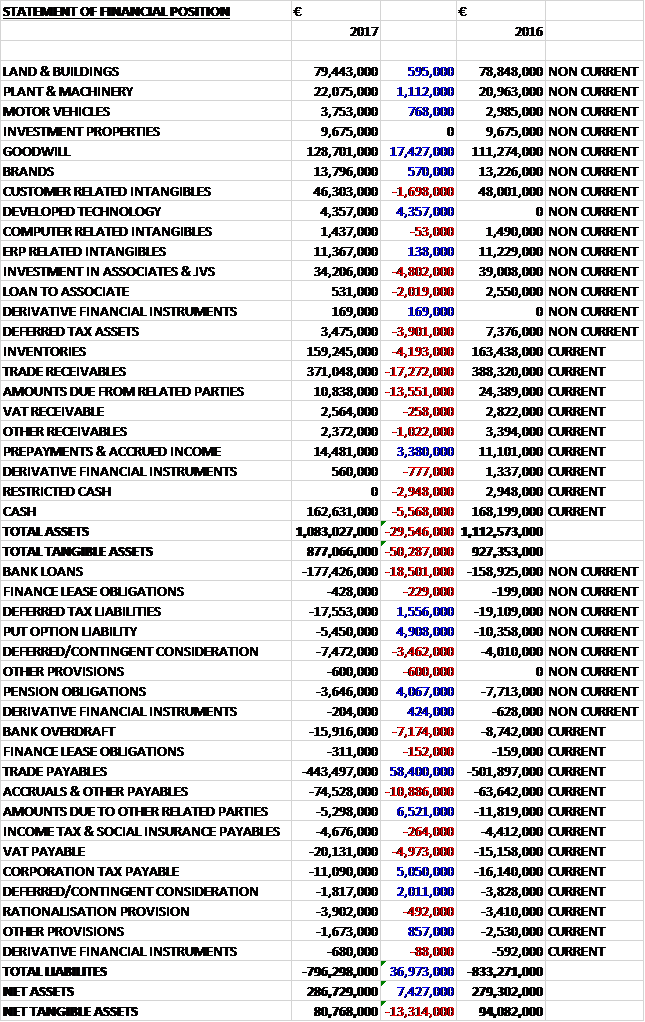

When compared to the end point of last year, total assets declined by €29.5M, driven by a €17.3M reduction in trade receivables, a €13.6M fall in amounts due from related parties, a €4.8M decline in investments in joint ventures, a €5.6M decrease in cash and a €4.2M fall in inventories, partially offset by a €17.4M growth in goodwill and a €4.4M increase in the value of developed technology. Total liabilities also declined during the year as an €18.5M increase in bank loans, a €10.9M growth in accruals and other payables and a €7.2M increase in the overdraft was more than offset by a €58.4M reduction in trade payables and a €6.5M fall in amounts due to related parties. The end results was a net tangible asset level of €80.8M, a decline of €13.3M year on year.

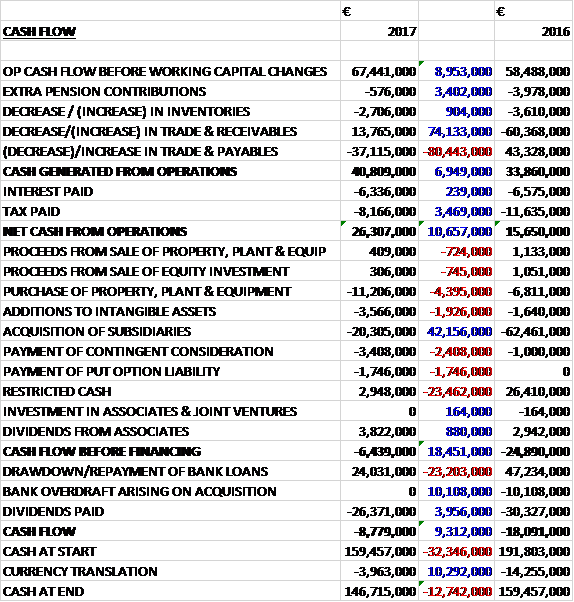

Before movements in working capital, cash profits increased by €9M to €67.4M. There was a cash outflow from working capital but this was similar to last year and after tax payments fell by €3.5M, the net cash from operations was €26.3M, a growth of €10.7M year on year. The group spent €11.2M on property, plant and equipment, €3.6M on intangible assets, €20.3M on acquisitions, €3.4M on deferred consideration and €1.7M on a put option, although they did receive €3.8M in dividends from associates. Despite this there was a cash outflow of €6.4M before financing. The group then drew down €24M of new loans to pay the €26.4M spent on dividends to give a cash outflow of €8.8M for the year and a cash level of €146.7M at the year-end.

Although headline revenue only increased by 0.5%, on a constant currency basis, this increase was 3.4% with this movement principally reflecting increased service revenue and input volumes. Underlying growth in agronomy services and inputs was 5%. With improved margins, the underlying operating profit at constant currency increased by 12% compared to the 4% actual increase.

The operating profit in the UK and Irish business was €54.7M, a decline of €778K year on year with a 1.3% growth in the core business being offset by a 21% decline in associate and joint venture profits. On a constant currency basis, the movement was a growth of 12% and a decline of 14% respectively. The positive impact of sterling depreciation on crop output values along with a favourable backdrop to global diary markets, and lower unit costs for key inputs, were all drivers of an improvement in farm incomes.

The group’s agronomy and on-farm services business delivered a satisfactory performance following particularly difficult trading conditions last year. Higher output prices in local currency together with lower than expected input cost inflation supported increased services and input demand. The business had a renewed focus on high service channels and value added technologies, resulting in higher volumes and improved margins across all portfolios. The business continues to extend the group’s position in the provision of systemised crop technology transfer direct to farm. This is supported by a comprehensive service offer, market leading agronomic research and technical support, and strong software based support capabilities.

There was strong progress on the integration of Resterra, which complemented a very satisfactory performance from Digital Agriculatural Services. Priority focus areas since the acquisition have included the development of new agronomy applications, organisational design and the launch of precision farming services across the European business.

Business to business Agri-inputs delivered good growth in profits in the period with performance principally supported by higher volumes and margins in fertilizer. Strong early season demand for fertilizer drove higher volumes for the year as a whole as primary producers benefitted from greater certainty in raw material pricing and more favourable farm economics. Speciality nutrition applications maintained solid development momentum and underpinned improved margins in the period.

The amenity business achieved a very satisfactory performance, reflecting good underlying volume growth across all business channels. The integration of Headland was completed in the period and in July the group acquired Linemark.

Feed ingredients achieved a satisfactory performance underpinned by good volume growth in competitive trading conditions. Volume improvement largely reflects a more favourable demand backdrop resulting from a combination of higher dairy cow numbers and improved returns for grassland farm enterprises that are seeking to maximise milk production following the abolition of production quotas in 2015. The group’s animal feed manufacturing associate delivered a satisfactory performance in the period.

The operating profit in the European business was €14.8M, a growth of €1.7M when compared to last year. Underlying agronomy services and input volumes increased by 6% reflecting the positive growth momentum in the sales of value added technologies. Market conditions were generally very competitive as farmers responded to volatile output markets and the impact of the challenging growing season in 2016. The operating margin reduced from 4.6% to 4.1%, however, reflecting the timing of acquisitions last year.

Poland delivered a solid performance. Higher margins were underpinned by an improved portfolio mix of value added technologies. On-farm activity showed positive momentum against a weak 2016 comparison, but service and input demand was largely subdued reflecting a delayed start to spring seasonal activity and the impact on primary producers of poor harvest yield and quality last year. Total winter and spring plantings were broadly in line with last year. The new €6M seed processing and input formulation facility is on target to be operational early in the 2018 financial year. This facility will enhance the product capabilities of the business and extend its market leadership in the provision of high performing certified seed varieties to Polish farmers.

Romania delivered a strong performance in the period with good growth achieved across the principal sales channels. Demand was resilient in the case of the main cropping enterprises underpinned by a 2% rise in the total cropping area. Crop development was satisfactory, notwithstanding the impact of intermittent unseasonal weather patterns in Q3. Nutrition portfolios performed strongly in 2017, reflecting the focus on meeting demand from primary producers for improved ranges and speciality applications. Good progress was achieved in business integration with the continued development of trial demonstration farms and knowledge transfer infrastructure supporting the delivery of enhanced technical support on-farm.

Ukraine delivered a good performance in the period, achieving higher revenues and margins underpinned by a favourable portfolio mix of services and input technologies. An improved macro-economic backdrop contributed to a more favourable financing environment for primary producers. Total winter and spring plantings were broadly in line with last year. Soil fertility and seed technology applications maintained good growth momentum with new customer gains supported through an expansion of the sales force together with an extension of the regional distribution footprint of the business. Solid progress has been made during the year leveraging the group’s supply chain partnerships to secure access to high spec technologies.

The group has announced the establishment of a dedicated digital, precision agriculture and crop science collaborative research partnership with University College Dublin, supported by Science Foundation Ireland. This five year development programme underpinning the research partnership is being financed by a €17.6M investment which is co-funded by Origin and SFI.

There were a number of acquisitions during the year. In November they purchased David Dumosch, an agricultural and horticultural merchant. In March they acquired Resterra, a digital agricultural services group that provides an enhancement to their digital technology capabilities with particular emphasis on expanding their data driven group management solutions framework. In July they acquired Linemark UK, a sports and amenity paint manufacturer supplying line marking paint, grass marking machines and accessories. The total consideration for these acquisitions was €25.4M, of which €5.1M was contingent. In all, €15.7M of goodwill was generated.

There were a number of exceptional items during the year. Rationalisation costs of €11M comprise the compensation and termination payments arising from the restructuring of the agronomy services business in the UK. Transaction costs of €2.5M principally comprise costs incurred in relation to the acquisitions. Organisational redesign costs of €1.7M relate to a project to enhance the group’s central capabilities, focusing on how the reporting and management structures need to evolve as the group continues to integrate businesses. The €2.7M gain is relating to the movement in fair value of the put option liability in respect of the Agroscope acquisition.

After the period-end, in August, the group completed the acquisition of Bunn Fertilizer. Based in the UK, the business is a producer of prescription fertilizer blends and nutrition management system servicing the arable grassland and horticulture sector. The consideration for the acquisition was €9M but there is no details on goodwill generation.

Going forward, the board anticipate a stable operating environment for primary producers in 2018, farm sentiment is expected to remain cautious reflecting general volatility in output markets. The group remains focused on capturing growth opportunity in systemised crop technology transfer and is well positioned to capitalise on its scalable business platforms, development opportunities and strong balance sheet.

At the current share price the shares are trading on a PE ratio of 19.8 which falls to 14.3 on next year’s consensus forecast. At the year-end the group had a net debt position of €31.5M compared to net cash of €174K at the start of the year. After the dividend was kept the same, the shares are yielding 3.1% which is forecast to remain steady next year too.

Overall then this was a solid year for the group. Profits declined but this was due to a slew of one-off costs, net tangible assets did decline but the operating cash flow grew, despite the group not producing any free cash. The UK and Ireland saw profits fall but this was due to currency movements and the underlying market seems pretty decent. Likewise things have improved in the group’s Eastern European markets. The forward PE of 14.3 and yield of 3.1% isn’t exactly cheap, however, and I am not sure this offers good value at the moment.

On the 24th November the group released a trading update covering the first quarter. Overall they had a satisfactory start to the year in the seasonally quiet quarter. Demand levels for agronomy services and crop inputs were favourable. This reflects a generally improved on-farm sentiment together with a positive planting profile to date in Autumn across the majority of markets.

Group revenue was €346.7M compared to €333.6M in the corresponding period last year. On an underlying basis, at constant currency, revenue increased by 5% reflecting increased volumes. Ireland and the UK delivered a satisfactory performance recording underlying volume growth in agronomy services and crop inputs of nearly 6%. On a like for like basis, there was an increase of nearly 10%.

Integrated Agronomy and On-Farm Services delivered a satisfactory performance in Q1 with all service and input portfolios maintaining solid momentum in competitive trading conditions. Autumn and Winter crop planting activity has advanced well following a delayed start in September and improved in-field conditions during October enabled significant catch up crop drilling activity.

Business to business Agri-inputs achieved a satisfactory results in the period with performance underpinned by higher fertilizer and feed volumes. Fertilizer recorded higher underlying volumes in highly competitive conditions. The emergence of raw material price inflation has slowed early new season sales order activity as primary producers adopt a cautious approach and defer procurement decisions until closer to the main application period in H2. Speciality nutrition applications maintained good growth momentum and positively supported margins in the period. The Bunn Fertilizer acquisition was fully integrated in the period and is performing to expectations.

The Amenity business maintained a good performance in the period with solid momentum achieved within the professional sports turf and fine turf channels. Linemark performed satisfactorily in the period and integration is progressing to plan.

Higher volumes underpinned a satisfactory performance from Feed Ingredients in the period. Favourable volume development is reflecting a combination of good spot demand in the quarter due to poor animal grazing conditions and improved forward buying interest from customers due to the generally positive backdrop for primary dairy production.

Continental Europe delivered a satisfactory performance recording underlying volume growth in agronomy services and crop inputs of nearly 14%. On a like for like basis there was an underling increase in revenue of 13.5% offset by a 2.5% reduction due to currency movements.

Poland performed well in the period with an increased contribution achieved across the principal service and input portfolios. Despite the favourable performance, many farmers continue to experience challenging operating conditions. A delayed harvest and poor ground conditions due to unsettled weather resulted in curtailed crop cultivation and maintenance activity in many regions of northern Poland. Autumn and winter planting are estimated to be around 3% lower than last year but the shortfall is expected to be recovered through an increase in spring plantings leaving the total cropping area broadly flat. Value added agronomy applications continue to maintain good growth momentum reflecting a favourable business mix and improved commercial effectiveness.

Romania achieved a satisfactory result in the period with all customer channels performing well. The nutrition portfolios continued to maintain good momentum, recording higher volumes in the period as primary producers seek improved ranges and speciality applications. Farm sentiment is positive reflecting a generally good harvest outcome with above average crop yields and quality for the main crop species. The total sown area for autumn and winter cropping is estimated to be in line with last year.

Ukraine delivered a solid performance in the period, in line with expectation and supported by an improved macro-economic backdrop. The business continues to benefit from an expanding distribution footprint and a continued focus on an enhanced crop technology portfolio to address the requirements of the high service segments of the market. Total autumn plantings for cereals and oil seed rape are estimated to be in line with last year.

Overall sector sentiment currently remains cautious against and improved planning backdrop for primary food producers. The autumn and winter cropping profile provides a strong foundation for the seasonally more important second half. Overall, this sounds OK.

On the 23rd January the group announced the acquisition of Pillaert-Mekoson. The business is based in Ghent, Belgium, and is a provider of standard and prescription fertilizer in Belgium and surrounding regions. The turnover for the business last year was €35M and EBITDA was around €1.8M. There is no indication of how much the acquisition costs but is being funded from existing bank facilities and is expected to be earnings enhancing in the first full year of ownership.