Photo-Me has now released their interim results for the year ending 2018.

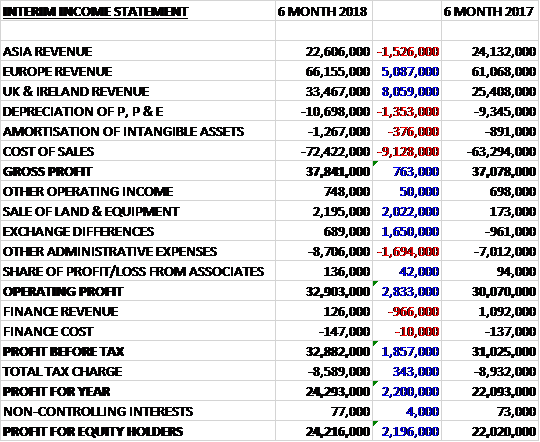

Revenues increased when compared to the first half of last year as a £1.5M decline in Asia revenue was more than offset by an £8.1M increase in UK and Ireland revenue and a £5.1M growth in European revenue. Depreciation was up £1.4M, amortisation increased by £376K and other cost of sales rose by £9.1M to give a gross profit £763K higher. The group made £2M more from the sale of land and equipment, and benefited from a £1.7M positive swing in exchange differences, but other admin expenses grew by £1.7M to give an operating profit £2.8M higher. Finance revenue was down £966K but tax charges fell by £343K to give a profit for the period of £24.2M, a growth of £2.2M year on year, half of which is related to favourable forex movements.

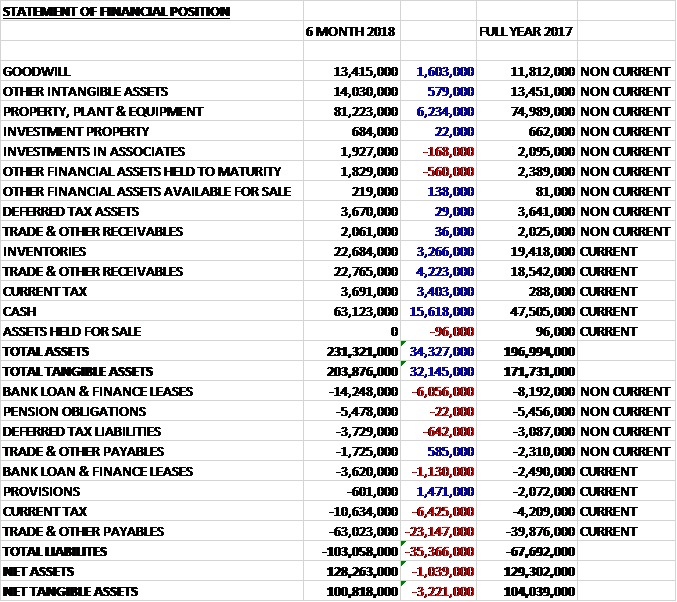

When compared to the end point lf last year, total assets increased by £34.3M, driven by a £15.6M growth in cash, a £6.2M increase in property, plant and equipment, a £4.2M increase in receivables, a £3.4M increase in current tax assets, a £3.3M growth in inventories and a £1.6M increase in goodwill. Total liabilities also increased during the period was a £1.5M decline in provisions was more than offset by a £23.1M increase in payables, a £7.2M growth in borrowings and a £6.4M increase in current tax liabilities. The end result was a net tangible asset level of £100.8M, a decline of £3.2M over the past six months.

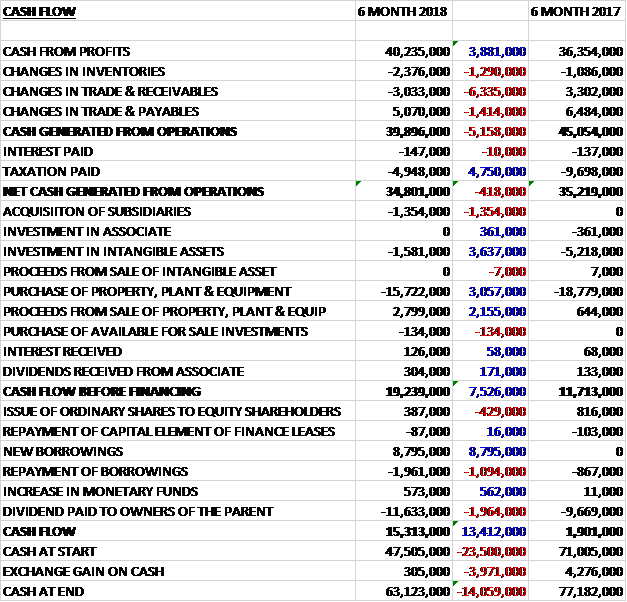

Before movements in working capital, cash profits increased by £3.9M to £40.2M. There was a broadly neutral working capital position compared to a cash inflow last year and after tax payments reduced by £4.8M the net cash from operations was £34.8M, a decline of £418K year on year. The group spent £1.4M on acquisitions, £1.6M on intangible assets, and £15.7M on fixed assets to give a free cash flow of £19.2M. Of this, £11.6M went on dividends and for some reason the group took out a net £6.8M of new borrowings, which makes me a bit nervous, to give a cash flow for the half year of £15.3M and a cash level of £63.1M at the period-end. Why are they taking out new loans to hoard so much cash? It doesn’t really make sense to me.

The operating profit in the Asian business was £2.4M, a decline of £1.3M year on year on revenues that fell by 6.2%, partially reflecting the impact of forex movements. At constant currency, the year on year decrease of 3% reflected more challenging market conditions in Japan and the lower contribution from the My Number ID programme. The board see future growth from the investment in launderette shops, with six now open in Japan.

Photo ID competition has remained high with new entrants looking to capitalise on the long term opportunity presented by the Japanese government’s My Number initiative which is expected to be made compulsory in the medium term (this no longer seems to be being flagged up as an opportunity for the group).

The operating profit in the European business was £22.5M, a growth of £485K when compared to the first half of last year on revenues that increased by 2.3%, primarily driven by a 39% increase in takings from the automated laundry machines and the recent upgrades to the photo booth estate with digital security features and roll out of further kiosks. France, the largest contributor in this sector, performed strongly with revenue up 3.2% and gross takings from the estate of automated Revolution laundries and the laundrette outlets increased by 40%. In Portugal, revenue from laundry operations increased to €700K with profits in the country more than doubling over the past two years.

The operating profit in the UK and Irish business was £7.3M, an increase of £2.6M when compared to the first half of last year reflecting continued expansion in laundry and the roll out of the secure digital upload technology for the Irish Online Passport Service. This includes a £2.3M profit from the sale of the head office building and £700K from acquisitions, offset by £900K in restructuring charges, meaning the underlying profit growth was just £500K. Ireland has been a focus for the laundry roll out programme and the country has seen revenues from laundry operations increase from €100K in 2015 to €2.1M in the same period this year.

The estate increased by 2.8% to 12,951 machines, reflecting the expansion in the laundry business as well as the roll out of the new Speed Lab digital printing kiosks. There has been softening in the UK market due to consumer disposable income constraints. This resulted in lower revenues from the UK photo ID operations in the first half, with slightly reduced demand for photo ID. This backdrop will be mitigated by actions to improve operational efficiencies in the business. Price rises from £5 to £6 have been implemented across the UK photo booth estate.

The group has taken some actions to boost the profitability of the UK digital printing business (the acquisition from Asda). The retail operations are being refocused to provide unattended digital printing kiosk activities, with the phased closure of manned retail outlets. This will result in a total one-off restructuring cost of £2M in the current year, of which £900K has been accounted for in the first half. The restructuring will improve the profitability of the business in the second half but there will be a negative impact on revenue.

The group has continued to invest in the further deployment of digital kiosks, mainly in the UK leveraging their presence across the Asda network. The board are pleased with the performance of the new equipment, achieving average monthly gross takings per unit of £800 across the estate and reaching £1,500 in the UK. They will further expand the roll out of the Speed Lab Cube and Speed Lab Bio released last year, offering the latest digital printing technology and an enhanced consumer experience, creating potential for further growth.

The group have continued to expand their services in Ireland through the deployment of their encrypted photo ID upload technology in their photo booths for online passport applications. Since the Irish government launched the new system in April 2017, around 200 photo booths have been enabled with the technology. They are on track to upgrade a total of 300 units by the end of the year. In the UK, discussions with HM passport office regarding the new online passport service hand testing have concluded positively. The service is now being rolled out to photo booths across the UK from mid-December 2017. The progressive rollout of secure and direct data transfer technologies in photo boots in Germany has continued with around 20 being upgraded.

Within laundry, the group’s manufacturing partner transferred production from Hungary to a new facility in Poland. This resulted in a short term slowdown in production but the new facility has the capacity to support production of 150 Revolution units per month in the second half of the year. This increase in production will enable to the group to accelerate deployment in the longer term.

In July 2017 the group completed the sale of their head office buildings in Bookham, Surrey. The freehold was sold to Shanly Homes for a consideration of £2.5M. The book value of the assets was only £100K so there was a profit on the sale of the building of £2.3M, taking into account sales costs of around £100K. The group has consolidated its head office and UK operations into one location in Epsom so the building was surplus to requirements.

In July 2017 the group acquired Inox Equip ltd and Tersus Equip ltd for a total consideration of £2M. The businesses are both UK based, business to business laundry companies which provide design, procurement and installation of laundry and catering equipment facilities for companies and institutions such as care homes and hospitals. The acquisition includes £450K of contingent consideration and generated goodwill of £1.5M. In the period after acquisition, the businesses generated pre-tax profits of £442K.

Going forward, in the medium term it is anticipated that laundry revenue will grow significantly as a proportion of the total group revenues and satisfactory progress is being made towards the target of 6,000 total laundry units deployed by the end of 2020. In the second half the group will benefit from the enhanced profitability of the retail operations once the refocus of activities is complete. Whilst remaining mindful of the macroeconomic environment, forex movements and consumer sentiment, the board remains confident about the group’s prospects.

After a 20% increase in the interim dividend the shares are yielding 4.2% which increases to 4.6% on the full year consensus forecast. At the current share price the shares are trading on a PE ratio of 19.7 which falls to 18.6 on the full year forecast. At the period-end the group had a net cash position of £47.1M compared to £39.2M at the end of last year.

Overall then this has been a bit of a mixed period for the group. Profits were up, but this was due to the sale of the HQ building and lower tax charges, otherwise profit would have declined somewhat. Net assets declined as did the operating cash flow but this was due to working capital movements and cash profits increased with a decent amount of free cash being generate, albeit with the group also taking out more loans.

The sluggish performance has come from Japan which has struggled with the delays to the My Number ID cards. Both Europe and the UK/Ireland saw a decent performance, buoyed by higher laundry takings and in the case of the latter, the new secure passport service. With a forward PE of 18.6 and yield of 4.6% the shares are not too bad value-wise actually and I continue to hold. Though the cash position seems a bit odd to me.

On the 19th February the group announced that the board of Max Sight, of which the group is an 18% shareholder, has made an application to list on the HK stock exchange. The business intends for the majority of the proceeds from the share offer to be used to fund the long term development of the business in the Guangdong province, expanding the network of photo booths. Following the listing, the group will hold nearly 14% of the share capital. The revaluation of the carrying value of the investment would lead to a revaluation gain of £3.3M.

On the 30th May the group released a trading update covering 2018. The board expects the group will achieve turnover growth of around 6% with the group’s pre-tax profit to be broadly in line with market expectations. As of the end of April, net cash was around £26M reflecting capex slightly ahead of last year, investment in laundry acquisitions and the restructuring of Photo-Me Retail.

The photo ID business continued to perform well except in Japan which has remained a very difficult market due to an oversupply which has put pressure on commissions across the industry. In the UK, rollout of the group’s encrypted passport photo ID upload technology commenced in mid-December. At the year-end, 2,200 photobooths had been upgraded with this technology. This technology is also installed in 200 photo booths in Ireland and 5,700 in France. The group is also in prelim discussions with the Dutch government regarding deployment of this technology in the Netherlands.

The laundry business continued to perform well. Revenue increased by 49% to £32.3M. Production capacity of the Revolution machine increased following the transfer from Hungary to Poland. The increase in volume will support an acceleration in laundry expansion, the early benefits of which started to come through towards the end of the financial year.

In May 2018, after the year-end, the group acquired LeWash, a Spanish business to business laundry services business based in Barcelona, for a consideration of €4.75M. The business, which is a franchise model, consists of two companies with a combined pre-tax profit of €796K.

The operations of Photo-Me Retail have been refocused to provide unattended digital printing kiosk services. This action will boost the profitability of the UK digital printing business but will result in a one-off restructuring cost of £2.6M in 2018.

Going forward, the Japanese photo ID market continues to be highly competitive. The number of photo booths increased significantly during the launch of the ID card but this programme was not compulsory and did not gain the momentum initially anticipated. During the current year, the group will invest in a restructuring of the Japanese business which should boost profitability from 2019.

Taking this into account, the board now believe that pre-tax profit in 2019 will be around £44M, below current market expectations and at a similar level to 2018. The board currently expect to maintain the existing dividend policy.

This does not look good, I am considering selling out here to wait for some signs of improvement.