Avingtrans has now released their final results for the year ended 2017.

Revenues increased when compared to last year as a £161K fall in medical revenue was more than offset by a £1.7M growth in energy revenue. Cost of inventories grew by £1.6M but other cost of sales were down £1M to give a gross profit £906K higher. There was an 89K fall in the profit on asset disposals but amortisation was down by £109K. Operating lease rentals increased by £80K, there was £101K of acquisition costs, no proceeds from the sale of property (£446K last time), there was £226K of tender share buyback costs and other admin expenses were up £397K to give an operating loss £239K higher. There was a £333K fall in interest receipts but tax payments were up £186K to give a loss for the year of £296K, a detrimental movement of £716K on a continuing basis.

When compared to the end point of last year, total assets declined by £22.9M, driven by a £28.8M fall in cash, partially offset by a £2.6M growth in inventories, a £1.5M increase in other receivables and a £1M growth in prepayments and accrued income. Total liabilities also declined during the year as a £1.2M increase in trade payables was more than offset by a £3.9M fall in borrowings. The end result was a net tangible asset level of £38.3M, a growth of £21M year on year.

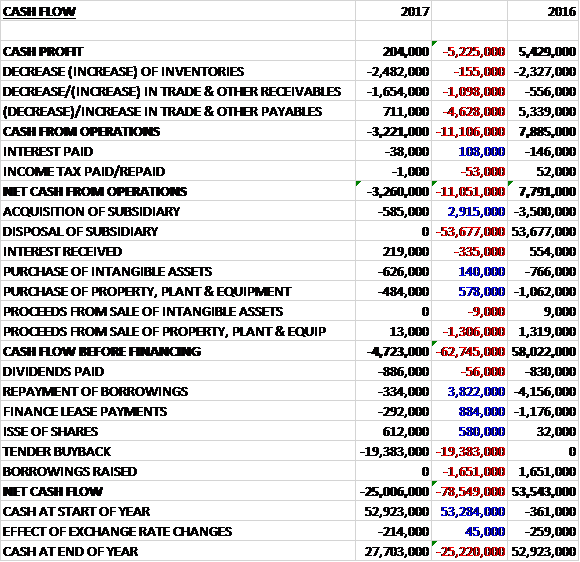

Before movements in working capital, cash profits declined by £5.2M to £204K. There was a cash outflow from working capital and despite interest payments falling by £108K, there was a net cash outflow of £3.3M from operations, a detrimental movement of £11.1M year on year. The group spent £626K on intangible assets, £484K on property, plant and equipment and £585K on acquisitions to give a cash outflow of £4.7M before financing. They also spent £886K on dividends, £292K on finance lease payments, and £334K on loan repayments before a £19.4M return of capital from tender buybacks meant that the cash outflow for the year was £25M and the cash level at the year-end was £27.7M.

The operating profit in the Energy business was £456K, a growth of £209K year on year reflecting the positive effects of restructuring at Maloney and the improving margin mix of new contracts at Metalcraft and Crown. The residual phase of restructuring at Maloney is now complete and the group continued to mitigate the negative effects of the oil price by focusing on the growth areas in the energy market such as energy storage, carbon capture and nuclear power life extension and decommissioning. Haywood Tyler had already been following a risk mitigation path for its oil and gas business plans and the board will continue to follow through with that restructuring.

At Metalcraft business with existing key accounts such as Cummins was steady. The ten year Sellafield contract to produce 3M3 boxes for the storage of nuclear waste progressed to plan and they also won an £11M three year contract extension, extending the scope of the box programme. They made good progress with facilities refurbishment and pre-production tests. The production set up and prototyping phase will continue in the current year, with series production expected to start in 2018.

At Maloney Metalcraft, the oil price continued to affect the business. They completed a limited restructuring process to stabilise their position. The gas project contract with Samsung was completed in the period and the JGC Gulf International project is nearing completion, following a number of customer induced design changes. Work also commenced on the EDF life extension contract and is proceeding to plan.

Crown had a stronger second half to the year, driven by the win of an important new £1.7M contract for flame detection masts, whose end customer is Fluor Corp. Work on this contract continues into the current year. The FET carbon abatement trial in Wales concluded and they are working to turn this application into a product of the future with FET. This technology promises to make small to medium fossil fuel generators “clean”.

The addition of Haywood Taylor brings with it several additional sites to the Energy division. The centre of excellence in Luton, the associated business in Vermont and Peter Brotherhood’s production facility in Peterborough, as well as sales, support and repair facilities in India and China. The facility in Luton includes an advanced facility for specialist motor manufacture.

The operating profit in the Medical business was £428K, an improvement of £616K when compared to last year and included a £115K loss from the acquired Space Cryomagnetics. This is despite a modest revenue decline mainly due to ramp up delays at Composite Products. The board anticipate growth coming through this year from recently won contracts such as Rapiscan and CAS Oxford as well as a full year of revenue from Scientific Magnetics. The division was awarded a £9M ten year contract for NMR cryostats during the year for a customer called CAS Oxford in China.

There have been some notable changes of ownership in some of the key players in the MRI sector recently and the board continue to see new entrants penetrating the Chinese medical imaging market, which, in general, they view positively in terms of business opportunity. These developments indicate that the sector will continue to spend money on developing new products and imaging techniques.

At Metalcraft, business with Siemens was steady in the UK and they continued to develop their relationships with other customers such as for Proton Therapy. In China, results for the unit continued to improve and they made good progress with existing customers such as Siemens and Alltech as well as preparing for the new contracts with Bruker and CAS Oxford for NMR vessels. Composite Products saw its performance in the second half suffer from ramp-up delays with key customer Rapiscan. They believe that the issues causing the delays are now resolved and expect to continue the ramp-up in the current financial year.

In February the group acquired 82% of Space Cryomagnetics to enhance their positon in the energy and medical division. The total consideration was £588K and the acquisition generated goodwill of £648K as it had net liabilities. There are call and put options enabling the group to purchase the remaining 18% of the issued capital of the business with an excise date of 2019 and 2022. The yexpect to acquire the remaining 18% with a contingent consideration of £256K being recognised. The acquisition enables the group to build their capability into superconducting magnets and cryogenics

After the year-end, in August, the group acquired Hayward Taylor for £29.4M through a share placing. At the same time, £11.5M of its facilities were repaid, a further £10M of debt assumed and £5M of transaction costs incurred (this seems a bit steep!) Last year the business had a turnover of £62.7M and a pre-tax loss of £3.7M.

At the current share price the shares are trading on an underlying PE ratio of 208.4 which falls to 66.8 on next year’s consensus forecast. At the year-end the group had net cash of £26.4M compared to £51M at the end of last year. After an increase in the dividend the shares are yielding 1.6% which is forecast to remain flat next year.

On the 2nd October the group announced that CEO Steve McQuillan purchased 18,500 shares at a value of just under £40K. He now holds a total of 243,500 shares.

On the 8th January the group released an update covering the first half of the year with performance in line with market expectations. The group has secured new business in generally improving market conditions. A number of notable contracts were secured in the period, worth almost £7M in total including nuclear life extension contracts worth £2.2M in Sweden and £2.5M in South Korea; a £1M steam turbine refurbishment contract; an initial £500K UK gas distribution network upgrade contract; and a £500K M6 smart motorway contract.

The immediate focus for the group has been the integration of Hayward Tyler and the re-establishment of profitable growth for the business. The initial integration and the necessary restructuring has been completed, in particular at Luton and Peterborough where the group has realised anticipated cost savings. Overall the opportunities for the long term profitable growth of the business as presented by the acquisition are as expected.

Overall then, on the surface this looks like a bit of a disappointing year for the group, with a swing to losses, a fall in net assets and an operating cash outflow. This is very much a business in transition, however, and operationally both divisions saw an improvement with restructuring and improved margin contracts helping the energy division. Going forward, the integration of Hayward Tylor and the Sellafield contract are two important factors and with the oil price improving things should be better this year.

This does seem to be factored into the share price, however, as unless I’m missing something the forward PE of 66.8 and yield of 1.6% looks quite expensive. One to keep an eye on I think.

On the 21st February the group announced that Haywood Taylor has won a $6.7M contract from Korea Hydro and Nuclear. The business has been a supplier of pumps and spare parts to them for over forty years. The latest order, for spare parts to upgrade and refurb existing nuclear power plants, they largest they have received from the group, takes the total value of orders received from this customer since completion of the acquisition to over $10M.