Telford Homes have now released their interim results for the year ending 2018.

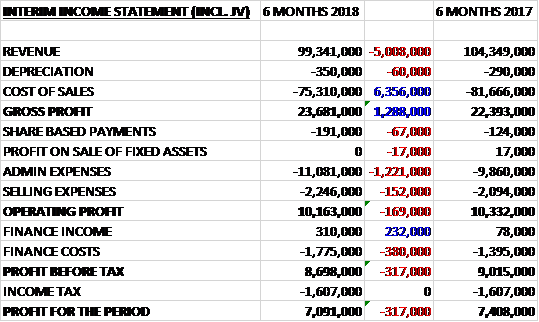

Revenues have declined by £5M when compared to the first half of last year. Depreciation was up £60K but other costs of sales declined by £6.4M to give a gross profit £1.3M higher. Share based payments grew by £67K, admin expenses were up £1.2M and selling expenses grew by £152K which meant that the operating profit was £169K lower. There was a £380K increase in finance costs but income tax remained flat to give a profit for the period of £7.1M, a decline of £317K year on year.

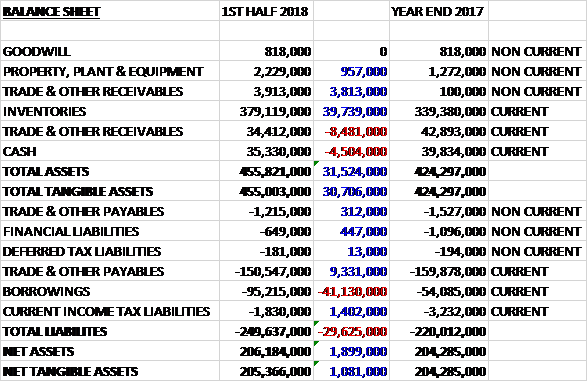

When compared to the end point of last year, total assets increased by £31.5M driven by a £39.7M growth in inventories and a £957K increase in property, plant and equipment, partially offset by a £4.5M decrease in cash and a £4.7M. Total liabilities also increased during the period as a £9.6M decrease in payables and a £1.4M fall in current tax liabilities was more than offset by a £41.1M growth in borrowings. The end result was a net tangible asset level of £205.4M, a growth of £1.1M over the past six months.

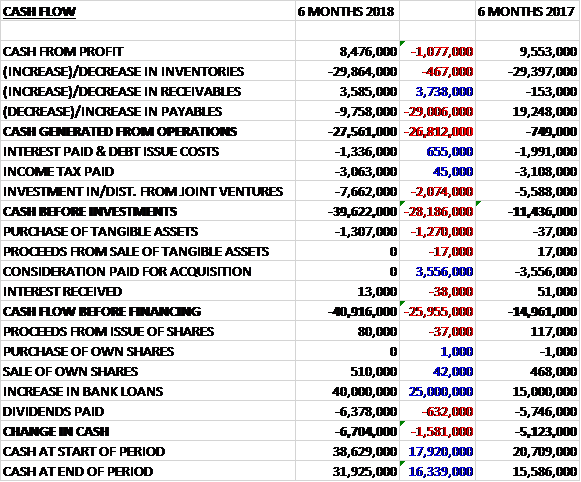

Before movements in working capital, cash profits declined by £1.1M to £8.5M. There was a bug cash outflow from working capital and after interest payments reduced by £655K and investments into joint ventures increased by £2.1M there was a net cash outflow of £39.6M, an increase of £28.2M year on year. The group spent £1.3M on intangible assets to give a cash outflow of £40.9M before financing. They then paid out £6.4M in dividends and took out a new loan of £40M to give a cash outflow for the half year of £6.7M and a cash level of £31.9M at the period-end.

The group’s financial results are influenced by the number of open market completions achieved and there were fewer of these in the period than expected in the second half. As experienced last year this is purely down to development timings which are all on track and in accordance with the original programmes but do not fall evenly across the year. Completions of individual properties are proceeding as planned with no delays.

In joint ventures, whilst there were more open market completions at 116 (85) there has been less revenue from construction contracts, particularly affordable housing, due solely to the timing of developments. In the future construction contracts will be a greater proportion of revenue due to the increased involvement in build to rent where profit is recognised as they build rather than at the end of the development.

The gross margin was 25.1%, up from 22% in the first half of last year. This increase is primarily due to some higher margin developments completing in the period. The margin on build to rent revenue was 17.5%, exceeding the target of 13% mainly due to cost efficiencies.

The group’s recent success in securing build to rent sales means they have not launched any new developments to individual customers in the period. They do have residual availability at a few predominantly forward sold schemes, however, where they have continued to make regular sales at prices in line with expectations.

They have two new development launches scheduled for Q1 2018. The second phase of New Garden Quarter in Stratford will be marketed and at Bow Garden Square they will be opening an on-site sales centre expecting to sell to owner-occupiers utilising Help to Buy. The expected average price at New Garden Quarter is around £550K and at Bow Garden Square it is less than £500K. At the latter 52 of the 83 homes for sale ae expected to be priced below £500K so that first time buyers can benefit from the reduction in stamp duty.

Despite some of the commentary around higher priced homes in London, the group have secured the sale of all four penthouse apartment at their Stratford Central development in the last few weeks for a combined sum of over £5M.

In June they signed a pre-construction agreement with global rental housing operator Greystar to develop just under 900 rental homes in Nine Elms, Battersea. Together they are making progress towards securing a detailed planning consent at which point the group will enter a full design and build contract and the site will then become a significant addition to their existing development pipeline. Their existing build to rent developments are progressing well with the Pavillions due for handover to L&Q by mid-2018. They are now actively looking for new opportunities with L&Q going forward.

Ongoing uncertainty around Brexit and a lack of political stability has deterred some potential buyers from making a purchase, particularly at higher

price levels. Changes to the tax system, especially the phased removal of tax relief on mortgage interest, have also dampened demand from UK based investors despite an active rental market. Despite this, the board expect the structural shortage of homes in London to continue to attract individual investors including those based overseas who typically invest from a larger asset base. The group are working harder to sell individual homes with prospective owner-occupiers needing more visits to a property before agreeing a purchase but this represents a more normal market environment rather than one where the homes sell immediately.

The development pipeline at the period-end represented £1.4BN of future revenues and comprised just under 4,200 homes, over 3,000 of which are in design or under construction with the remainder going through the planning process. The average expected price for open market homes in the pipeline is just under £540K. The group are in promising discussions on a number of attractive opportunities to add to the pipeline both for build to rent and individual sale.

Going forward the board believe the group is well positioned to meet market expectations for the full year with over 95% of gross profit secured. They are on track to deliver over £40M pre-tax profit in 2018 and secured over 65% of the gross profit required to exceed £50M in 2019.

At the current share price the shares are trading on a PE ratio of 11.4 which falls to 8.9 on the full year consensus forecast. After an 11% increase in the interim dividend the shares are yielding 3.9%, increasing to 4.1% on the full year forecast. The net debt at the period-end stood at £59.9M compared to £14.3M at the year-end. This was as expected and is driven by construction on larger sites as they deliver on their pipeline.

On the 20th December the group announced that it had exchanged and completed contracts with U+I and Parkdale Investments for the purchase of a significant residential-led development site in Walthamstow for a total consideration of £33.9M. The site benefits from detailed planning consent for 257 open market homes, 80 affordable homes and 18,830 square feet of flexible commercial space. Whilst this development can be marketed for individual sales the group expects to explore entering into a build to rent transaction for the delivery of the open market homes in the New Year and will undertake the detailed design accordingly. Vacant possession is expected by April 2018 and the group intends to start work in Autumn 2018 with completion expected in late 2021.

Also on the 20th December the group announced that they had exchanged contracts with the London borough of Brent for the redevelopment of Gloucester House and Durham Court, a significant residential development site in South Kilburn. The development will deliver 124 new open market homes, 102 affordable social rent homes and ten shared equity homes in buildings ranging from four to eight stories high. The gross development value of the scheme is expected to be around £95M and work is already underway on site with completion expected in 2021.

Overall then, this appears to be a bit of a mixed period but it was as expected. Profits were down and the operating cash flow deteriorated with a large cash outflow. Net assets did increase modestly, however. All this was flagged up well in advance, though, and the board are very confident of a strong second half. The market seems to be fairly robust in the price-points that the group operates in. With a forward PE of 8.9 and yield of 4.1% these shares look decent value and I continue to hold.

On the 2nd Febuary the group announced that Chairman Andrew Wiseman sold 125,000 shares at a value of £512K. He still owns 2,203,927 shares.

On the 15th February it was announced that non-executive director Jane Earl purchased 6,342 shares at a value of £25K. She now owns 7,432 shares.

On the 18th April the group released a trading update covering the year ended 2018. They expect to report record levels of revenue and profit with pre-tax profit expected to be up by more than 30% and slightly ahead of current market expectations. This increase has been assisted by an improvement in the group’s operating margins by around 3 percentage points.

The housing market in London has remained robust at the group’s typical price point. In January they launched the second phase of New Garden Quarter in Stratford, marketing first in the UK and then internationally. They secured over 100 reservations across three weeks which exceeded initial expectations. Dampened UK based investor demand due to recent tax changes restricted domestic sales to a quarter of these reservations, however, with the remainder sold in China which represents a growing market for the group. The demand is driven by good rental yields with the homes expected to complete in mid-2019.

All of the remaining available homes at Bermondsey Works have been sold in recent weeks, alongside a continuing rate of sale of the remaining higher priced homes at Manhattan Plaza. In late March the group launched Bow Garden Square, focused on owner-occupiers with prices starting from £390K. Initial interest has been encouraging and a number of reservations have been secured.

There is no sign of the weight of investor demand diminishing and the group continues to be approached by new rental operators looking for opportunities. The development pipeline now includes over 4,000 homes compared to 3,972 last year and the average price of the open market homes within that is around £539K compared to £527K.

In December the group exchanged and completed contracts with U+I and Parkdale Investments for the purchase of a significant development site in Walthamstow for a total consideration of £33.8M and the group is about to start a formal marketing process to find a build to rent investor for all of the open market homes having concluded a period of initial design work.

The planning environment in London continues to be challenging and the group has experienced some delays in recent months. They are well place to acquire more sites to add to the pipeline, however.

This all sounds fine, I continue to hold.