James Latham has now released their interim results for the year ending 2018.

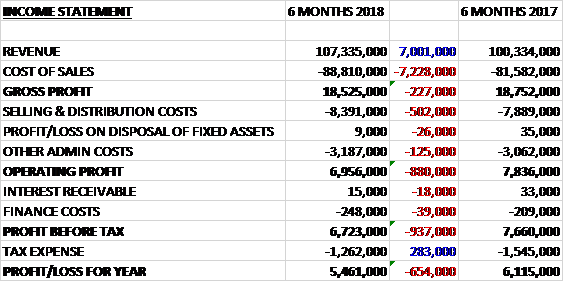

Revenues increased by £7M when compared to the first half of last year but cost of sales grew by £7.2M to give a gross profit £227K lower. Selling and distribution costs were up and admin costs increased by £151K which meant the operating profit fell by £880K. There was also an £18K decline in interest receivable and a £39K growth in finance costs but this was offset by a £283K reduction in tax charges to give a profit for the period of £5.5M, a decline of £654K year on year.

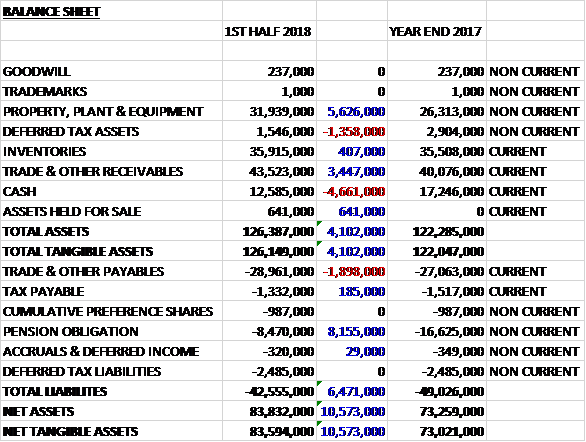

When compared to the end point of last year, total assets increased by £4.1M, driven by a £5.6M growth in property, plant and equipment reflecting the new warehouse at Yate and start of the investment in the new warehouse in Leicester, and a £3.4M increase in receivables, partially offset by a £4.7M fall in cash and a £1.4M decline in deferred tax assets. Total liabilities declined during the period as a £1.9M increase in payables was more than offset by an £8.2M decrease in pension obligations. The end result was a net tangible asset level of £83.6M, a growth of £10.6M over the past six months.

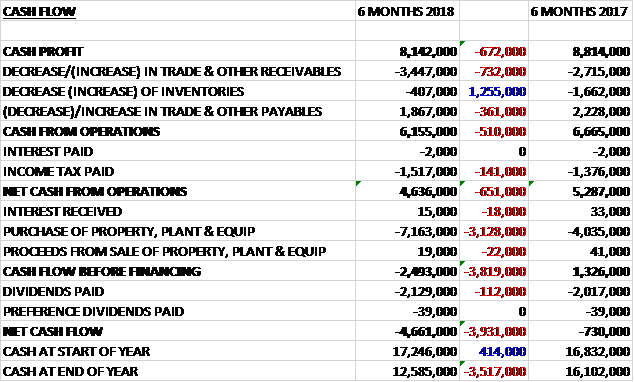

Before movements in working capital, cash profits declined by £672K to £8.1M. There was a cash outflow from working capital, although this was slightly less than last time and after tax payments increased by £141K, the net cash from operations declined by £651K to £4.6M. The group spent £7.2M on property, plant and equipment to leave a cash outflow of £2.5M before financing. They then spent £2.1M on dividends to give a cash outflow of £4.7M in the half year and a cash level of £12.6M at the period-end.

The group have seen volumes continue to grow especially through their own warehouses where they are up nearly 8%. The cost price of their products overall continues to increase, in part due to the weakening of sterling following the Brexit vote and in part due to manufacturers increasing prices, some of which the group have not been able to pass on to customers. Gross margins therefore declined from 18.7% to 17.3% but the board believe they are starting to stabilise. They were also affected by some disruption to supplies from some of their key suppliers’ manufacturing facilities which are now getting back to normal.

In July the group completed the move of their Yate depot to a new facility. It is already performing ahead of expectations but the group incurred £100K of costs relating to the move. The group are now looking forward to the relocation of their Wigston depot to a site closer to the motorway network in Leicester ahead of schedule in January 2018.

Going forward the second half of the year has started well with growing revenues at slightly higher margins. Trading conditions continue to be mixed, but despite the uncertainties in the economy, the group remains busy.

At the current share price the shares are trading on a PE ratio of 14.2 and after the interim dividend remained unchanged, they are yielding 1.9%. I can find no forecasts.

Overall then this has been a bit of a mixed period for the group. Profits declined as did the operating cash flow with no free cash being generated. Net assets did improve and revenues were up but the group has suffered from increasing costs. They have started the second half with somewhat improved margins but a PE ratio of 14.2 and yield of 1.9% looks on the high side to me.

On the 22nd March the group released a trading update covering the year ended 2018. Revenue and pre-tax profit are expected to be in line with market expectations. The relocation of the Wigston depot to the new site in Leicester has been completed with minimal disruption to the ongoing business and the old site has now been sold.