Naibu has now released their half year results for the year ending 2013.

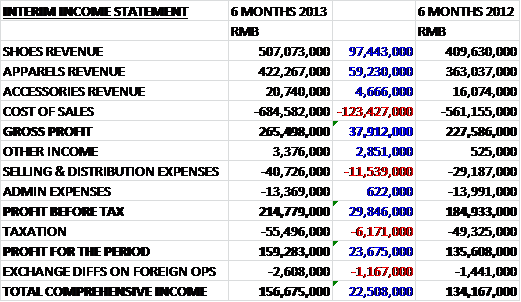

Once again, revenues were up across all product types with shoes increasing by £9.7M, mainly due to higher sales volumes and apparel up by £5.9M, which was a slightly slower rate than the other categories due to a timing difference in the delivery of sales orders which resulted in a strong showing in the first half of last year. Cost of sales also increased partly due to the increased proportion of lower margin shoe sales and the increase of costs due to some of the shoes being manufactured by OEM suppliers due to the lack of the group’s own manufacturing capacity. Selling and distribution expenses also increased, mainly due to an increase in amortisation expenses related to the store decoration subsidy for distributors’ shops, but admin expenses fell slightly due to the IPO costs incurred in 2012, to give a profit before tax £3M higher at £21.5M. An increased tax bill then gave the overall profit for the period of £15.9M.

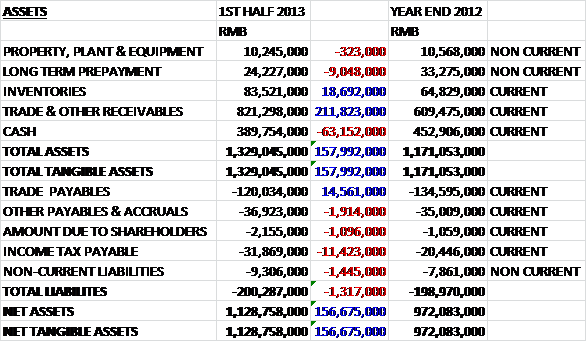

When compared to the end point of last year, total assets at the end of the first half were up by £15.8M which was due to a £21.2M hike in trade and receivables and a £1.9M increase in inventories, somewhat mitigated by a £6.3M fall in the cash levels. Liabilities did not change a great deal with a £1.5M fall in trade payables counteracted by small increases elsewhere, the largest of which was a £1.1M increase in tax payables. This meant that net assets for the year were up an impressive £15.7M to £112.9M.

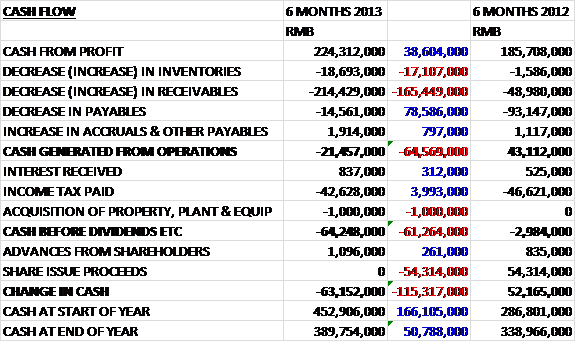

Cash profits for the first six months were up by £3.9M but this was almost entirely swallowed up by a massive increase of £16.5M in trade receivables which, along with a £1.9M increase in inventories and a £1.5M decrease in payables meant that the cash flow after working capital considerations was a negative £2.2M, a fall of £6.5M on the same period of last year. On top of this there were £4.3M of taxes paid out which meant that the overall cash outflow was £6.3M, £11.5M worse than last time, albeit last year did benefit from the £5.4M of share issue proceeds. This is undeniably a bit disappointing but I hope it is due to a ramp up of orders.

It is claimed that trade receivable turnover days actually fell in the period so the huge increase is likely due to more orders (it remained high at 116 days). The trade payable cycle did decrease, however, from 47 to 33 days. The disparity from the 33 days the group takes to pay its payables and the 116 days that their customers take to pay Naibu is very clear and not a great state of affairs.

Although revenues for shoes are higher than apparel, the group actually made more profit on the clothing ranges (£8.1M compared to £7.8M, however both products are increasing profits).About 54% of the shoes sold by the group are manufactured internally with the rest of the shoes and all of the apparel being made externally.

Growth is continuing on the retail side of things and 104 new stores were opened since the end of last year. The group are also releasing a new brand called “Nibo” based on a European fashion concept which will be launched in 2015. One thing that Naibu does that in their opinion gives a competitive advantage is to provide a renovation subsidy so that their distributors can upgrade their retail stores to keep them looking new.

In the last report it was mentioned that the group was building new shoe production facilities in Western China but this has taken longer than was anticipated due to the changes in the political leadership in China. The group has now signed an agreement with the government of Dazhu County in Sichuan province to purchase land use rights for 13.3 hectares to develop a Naibu industrial zone. This will include R&D, manufacturing and logistics facilities. As part of the investment, by mid-2015 there should be 12 new production lines in operation at this site. The group will pay RMB60M for the rights but the total cost of the project is likely to rise to about RMB300M, which is quite a substantial investment. The group have now completed their purchase of its new plant in Quangang for RMB 157M and the new production lines are expected to be operational by the end of this February which is a delay of two months. This delay meant that the shoes will have to be sourced from OEM manufacturers at a lower margin to prevent any interruption to the supply chain. Until the new production lines are up and running, the four existing lines will continue to produce shoes but the plant in Shishi was vacated because the lease expired (as was previously announced).

Going forward, the board expects to be challenged by continued inflation and increased competition but government urbanisation plans continue to provide more opportunities for sales. It is clear that this half of the year was one of expansion for the group and although the delay in the construction of the new factory is a blow and is hurting margins, the investment is definitely needed. The new industrial zone in the West of the country is an interesting development and should be good for the long term future of the group although it is likely to swallow up a lot of cash in the short to medium term. The disparity between the average trade payable days and trade receivable days is a worry and the huge increase in trade payables is harming the cash flow but hopefully this is a signal that the business is growing rather than anything else. The group has declared an interim dividend of 2p per share, which, when compared to the 4p at the end of last year equates to a yield of 7.7% which is a very good return. Given the cash levels after the unfavourable movements in working capital, along with the capital commitments in the new industrial zone, however, it remains to be seen as to how sustainable this is. Overall though, I think that there is a case for investment here and due to the fact that Naibu seems to be a bit further down the journey than Camkids, I have dipped my toe in here.

On 29th January, the group released a trading update covering the year to December 2013. It was stated that results wold be in line with expectations and that during the year, revenues increased by 15%. The move to the new production facility at Quangang is on track to be completed by the end of February. Nothing really to say here.